Rival bills want to make homebuying more affordable. Here's how.

Two competing bills would restrict big investors from buying single-family homes, but they take different approaches.

Watch CBS News

Two competing bills would restrict big investors from buying single-family homes, but they take different approaches.

Mortgage rates have fallen to their lowest level since 2022, and now borrowers can find even lower-cost loans, experts said.

Refund amounts for State Farm customers will vary based on their place of residence and insurance premiums.

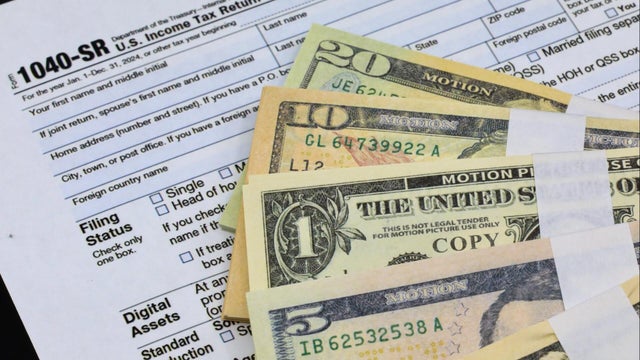

Early tax refund data shows the typical check is so far 14% higher than a year ago. Here's what Americans are planning to do with the money.

President Trump's media company, which is merging with a fusion energy player, is exploring whether to spin off Trump Social as a publicly traded concern.

FedEx said it will reimburse customers if the Trump administration provides refunds following a Supreme Court ruling that struck down emergency tariffs.

Streaming giant Netflix declines to match Paramount Skydance's $31 per share offer for Warner Bros. Discovery.

The decline in the average 30-year mortgage rate could be good news for home shoppers as the spring home-buying season gets rolling.

Novartis has settled a suit by Henrietta Lacks' estate alleging the pharmaceutical giant unjustly profited off cells were taken from her tumor without her knowledge in 1951.

Gold's price recently hit record highs, but that doesn't mean every form of gold investing is a guaranteed win.

Mortgage interest rates are dropping again, but could they fall back to 3%? Here's what to consider this March.

If a disability has made your credit card payments unmanageable, debt forgiveness may be closer than you think.

CBS News is tracking the rising cost of products most impacted by tariffs imposed and soon-to-be-imposed by President Trump, from grocery items to cars and trucks.

These charts track prices consumers pay for groceries and other goods now compared to five years ago.

Millions of Americans lack access to any type of retirement plan, hampering their ability to save for old age.

A new tax deduction for senior citizens is kicking in this tax season, potentially providing bigger refunds to millions, the AARP says.

As many Americans head into 2026 with mounting money worries, reviewing your finances now could help put you on firmer footing next year.

A college degree still provides an edge when it comes to finding a good job, but a person's major may be just as important to career stability, research suggests.

"Reverse recruitment" firms promise to cut the length of job searches in half and help connect candidates with employers.

Although economists have generally downplayed the impact of artificial intelligence on jobs, some employers are highlighting their adoption of AI.

Mortgage rates have fallen to their lowest level since 2022, and now borrowers can find even lower-cost loans, experts said.

President Trump said Friday that he is "not happy" with the pace of progress in negotiations with Iran.

The criminal civil rights case has also ensnared journalist Don Lemon.

Two competing bills would restrict big investors from buying single-family homes, but they take different approaches.

Refund amounts for State Farm customers will vary based on their place of residence and insurance premiums.

Mortgage rates have fallen to their lowest level since 2022, and now borrowers can find even lower-cost loans, experts said.

Two competing bills would restrict big investors from buying single-family homes, but they take different approaches.

Refund amounts for State Farm customers will vary based on their place of residence and insurance premiums.

President Trump's media company, which is merging with a fusion energy player, is exploring whether to spin off Trump Social as a publicly traded concern.

Early tax refund data shows the typical check is so far 14% higher than a year ago. Here's what Americans are planning to do with the money.

President Trump said Friday that he is "not happy" with the pace of progress in negotiations with Iran.

The criminal civil rights case has also ensnared journalist Don Lemon.

Two competing bills would restrict big investors from buying single-family homes, but they take different approaches.

Some of the changes mirror Scouting America's suggestions to the Department of Justice, including discontinuing its Citizenship in Society merit badge.

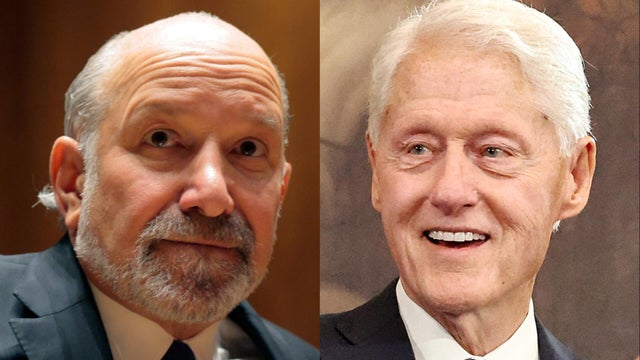

Former President Bill Clinton denied any knowledge of Jeffrey Epstein's crimes in an opening statement before the House Oversight Committee in New York.

More than three dozen states cover dental services for people on Medicaid, but with about $900 billion in cuts expected to hit states over the next decade, many programs could roll back dental coverage.

Chaz and Jean Franklin were facing a sevenfold increase in their health premium payments with the expiration of enhanced federal subsidies for Affordable Care Act plans. Then Jean received a crushing diagnosis.

A British gym chain is offering classes in "kidulting," luring adults into fitness with classes built around playground and PE class classics.

Starting in 2027, the Danish pharma firm will sell its weight-loss and diabetes drugs for $675 per month.

Robert F. Kennedy Jr. has criticized the broadening use of anxiety medications, but doctors and researchers say the MAHA movement is misrepresenting drugs that have been proven to help.

The find was made on a farmer's land in western Wales, museum Amgueddfa Cymru said.

President Trump said Friday that he is "not happy" with the pace of progress in negotiations with Iran.

One official calls a newborn boy "a symbol of the resistance of the Akuntsu people, but also a source of hope for Indigenous peoples."

As Trump leaves the threat of war on the table amid nuclear talks with Iran, the State Department urges Americans to "consider leaving Israel" while they can.

The U. S. is offering $5 million each for information on Rene Arzate Garcia and his brother Alfonso Arzate Garcia.

In his memoir, the Tony Award-winning composer of such hits as Broadway's "Hairspray" writes of his half-century in show business, which grew in part from his youthful worshipping of Bette Midler - an adoration that would grow into a collaboration.

For Oscar-winning composer Ludwig Goransson, creating the score for "Sinners" was a challenge, explaining he had to find his "voice within the blues." He describes his unlikely personal connection to the music and how he met the film's director.

"Scream" writer and creator Kevin Williamson describes his passion for horror films and being asked to direct a "Scream" movie for the first time, at the request of one of the returning stars. Natalie Morales reports.

Bobby J. Brown's breakout role was as a police officer on HBO's "The Wire." He appeared in 12 episodes across four seasons.

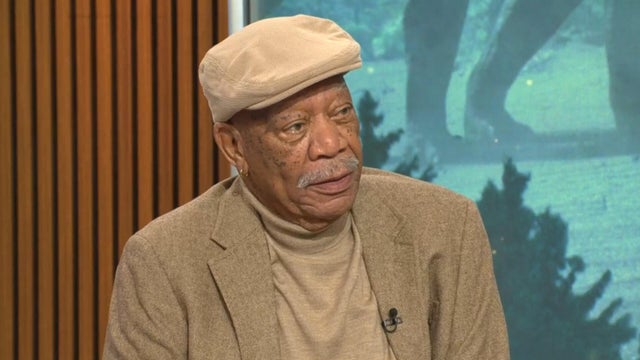

Legendary actor Morgan Freeman, who has starred in more than 100 movies in his six-decade career, joins "CBS Mornings" to talk about narrating the docuseries "The Dinosaurs" and how he's fighting the use of artificial intelligence to replicate his iconic voice.

The Pentagon's Friday afternoon deadline for Anthropic on granting use of its AI technology for certain military matters is rapidly approaching. Axios tech reporter Maria Curi joins CBS News with more.

Emil Michael, the U.S. under secretary of defense for research and engineering, speaks with CBS News' Jennifer Jacobs about how the military can benefit from artificial intelligence and defends the Pentagon's stance in its dispute with Anthropic over the use of the AI model Claude. Michael says the military has "made some very good concessions" and hopes Anthropic will do "the right thing" and reach a deal.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

The Pentagon's ultimatum for Anthropic on the use of its AI technology could impact U.S. military readiness. Tara Copp, a national reporter for The Washington Post, joins CBS News with more.

Defense Secretary Pete Hegseth set a deadline for Friday afternoon that involves Anthropic granting all lawful use for its AI technology. Amrith Ramkumar, a reporter for The Wall Street Journal, joins CBS News with more details.

NASA Administrator Jared Isaacman announced significant changes to the agency's Artemis program, which aims to land on the moon in 2028.

Documents might help scientists shed light on unexplained phenomena and government secrets, experts said.

A large shark was caught on camera for the first time in Antarctica's waters, surprising researchers. "There's a general rule of thumb that you don't get sharks in Antarctica," one said.

On the evening of Christmas 1776, Gen. George Washington surprised the King's forces by leading the Continental Army in a surprise crossing of a near-frozen Delaware River - a watershed military maneuver that dramatized a changing America, and a changing climate.

On the evening of Christmas 1776, Gen. George Washington surprised the King's forces by leading the Continental Army in an unanticipated crossing of a near-frozen Delaware River. Environmental correspondent David Schechter looks at how Washington's watershed military maneuver dramatized both a changing America, and a changing climate.

Former President Bill Clinton is being deposed by members of the House Oversight Committee over his alleged links to Jeffrey Epstein. CBS News' Nikole Killion reports.

Columbia University acting president Claire Shipman described the ICE detention of student Elmina "Ellie" Aghayeva, claiming agents gained entry to a residential building by stating they were police seeking a missing child. CBS News' Tom Hanson reports.

Former President Bill Clinton is up next for a deposition before members of the House Oversight Committee regarding his alleged links to convicted sex offender Jeffrey Epstein. CBS News' Nikole Killion reports.

Columbia University student Elmina Aghayeva has been released after ICE took her from one of the institution's residential buildings. CBS News' Tom Hanson reports.

Kentucky Republican Rep. James Comer, the chairman of the House Committee on Oversight and Accountability, said Commerce Secretary Howard Lutnick may be asked to testify on his knowledge of convicted sex offender Jeffrey Epstein's dealings. This comes as former President Bill Clinton prepares for his deposition. CBS News' Nikole Killion reports.

NASA announced an overhaul to its Artemis moon program as safety concerns persist. CBS News space contributor Christian Davenport breaks down the key takeaways.

NASA Administrator Jared Isaacman announced significant changes to the agency's Artemis program, which aims to land on the moon in 2028.

NASA's Artemis II mission continues to face concerns and delays. Scott E. Parazynski, a former astronaut, joins CBS News with more.

NASA is rolling back the Artemis II moon rocket from its launch pad at the Kennedy Space Center in Florida. It is expected to take up to 12 hours to move the 322-foot rocket, with the journey spanning four miles back to its hangar for repairs. CBS News space consultant Bill Harwood has more.

Fixing the Space Launch System rocket's helium pressurization problem has pushed the Artemis II launch to at least April 1.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

Does the evidence show a cover-up, or was Todd Kendhammer wrongfully convicted for the murder of his wife?

Christy Salters-Martin dominated in the boxing ring but faced her toughest challenger at home.

Family seeks answers in death of newlywed who disappeared in 2005 while on Mediterranean honeymoon cruise.

Meet the tattooed beauty charged in the death of Google executive Forrest Hayes.

The U.S. shot down a Border Patrol drone near the Texas border. CBS News' Kris Van Cleave reports.

Energy Secretary Chris Wright visited Texas and boasted about eased costs at the gas pump under the Trump administration, although he conceded prices are high amid uncertainty on Iran. CBS News' Ed O'Keefe spoke to Wright at a Corpus Christi gas station.

Hollywood is known for its iconic sign, Walk of Fame and studio lots bringing movies to life – but in 2026 the future of the entertainment industry is changing. Jo Ling Kent reports.

The Pentagon's Friday afternoon deadline for Anthropic on granting use of its AI technology for certain military matters is rapidly approaching. Axios tech reporter Maria Curi joins CBS News with more.

President Trump took questions before departing the White House on Friday and discussed the U.S. talks with Iran on its nuclear program and the future of Cuba. CBS News' Zak Hudak reports.