What products generate the most retirement income?

Using your investments to generate a retirement paycheck is one of the most important -- and challenging -- retirement planning tasks. One very important factor to consider when choosing the best way to generate retirement income is the amount that a specific retirement income generator (RIG) will pay you at the start of retirement.

One way to systematically compare the different RIGs is to calculate the payout ratio for each RIG. The payout ratio is the amount of annual retirement income you'll receive upon retirement divided by the amount of savings used to generate that income.

To help you see how this works, this post calculates the payout ratios for a handful of RIGs. The RIG that generates the highest amount of income may surprise you.

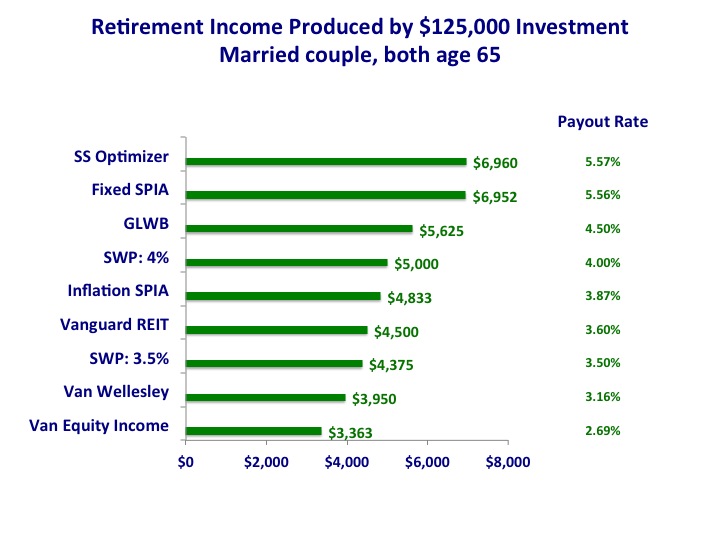

The chart below shows the payout ratios and annual amounts of retirement income a married couple, both retiring at age 65 in January 2015, could likely generate with a $125,000 investment in each of nine different RIGs (I'll explain later why I picked this number).

To understand the results, let's review some basic information about RIGs, which come in three types:

- The first involves investing your savings and using just interest and dividends for a retirement paycheck, while keeping your principal intact.

- The second requires you to invest your savings. To calculate your paycheck, use a method that systematically and cautiously withdraws principal, interest and dividends with the goal of not running out of money before you die (called a systematic withdrawal plan, or SWP).

- The last option involves buying an annuity from an insurance company.

Each type of RIG has many variations, features and pros and cons.

Here's an explanation of each RIG on the chart:

- SS Optimizer, or Social Security Optimizer, is the winner with a payout ratio of 5.57 percent. This RIG uses your savings to enable you to delay starting Social Security benefits until age 70 by using savings to pay the amounts you would have received from Social Security had the primary worker started benefits at age 65. For this purpose, the calculation assumed the worker had earned an average monthly Social Security income of $1,500 at age 66, which would be decreased to $1,400 if they started benefits at age 65 but increased to $1,980 if they started at age 70. Delaying the Social Security income from age 65 to 70 increases your lifetime monthly income by $580 per month, essentially earning you a lifetime annuity from Social Security. To make the payout rate calculation comparable to other RIGs, retirement savings were used to pay our hypothetical couple the extra $580 per month from age 65 to 70.

- Fixed SPIA is a single premium immediate annuity purchased from an insurance company using the Income Solutions annuity-bidding platform. This annuity is fixed in dollar amount and comes with a 100 percent joint and survivor benefit, making it payable as long as one member of the married couple is alive.

- GLWB is a guaranteed lifetime withdrawal benefit, an insurance company product that combines the features of annuities and systematic withdrawals. This example uses Prudential's IncomeFlex institutional GLWB.

- SWP: 4 percent is a systematic withdrawal plan that uses the common 4 percent rule to calculate the initial amount of retirement income.

- Inflation SPIA is the same as the fixed SPIA described above, except that the monthly income is adjusted for inflation each year.

- Vanguard REIT uses just the interest and dividends from Vanguard's REIT (Real Estate Investment Trust) index fund, calculated by adding up the interest and dividends received during 2014 by the 2014 year-end value of the fund. The principal is kept intact.

- SWP: 3.5 percent is a systematic withdrawal plan that reduces the payout from the 4 percent rule to reflect the current low interest rate environment and the possibility of paying significant fees for an advisor and/or investment manager.

- Van Wellesley uses just the interest and dividends from Vanguard's Wellesley fund, a fund that's balanced between stocks and bonds.

- Van Equity Income uses just the dividends from Vanguard's Equity Income fund, which is primarily invested in dividend-paying stocks.

The Social Security optimizer strategy is particularly attractive when you consider that the income is adjusted for inflation each year. The next highest-paying RIG -- a fixed annuity -- doesn't increase for inflation. In addition, the extra Social Security income is guaranteed by the U.S. government. With any other RIG, you need to consider the strength of the underlying insurance company, financial institution or the underlying stocks and bonds.

The amount of retirement savings you can use for the Social Security Optimizer strategy is limited by your specific Social Security benefit (the $125,000 amount worked for the example used here). You can't apply unlimited amounts of savings to buy a higher benefit from Social Security. With all of the other RIGs on the chart, however, nothing limits the amount of savings that can be applied to that RIG.

One conclusion from this analysis is that in most circumstances, it just doesn't make sense to start an income under any other RIG until you've implemented the Social Security Optimizer strategy.

When selecting a RIG or combination of RIGs, you'll want to consider other important factors as well, including these:

- Is your retirement paycheck guaranteed for the rest of your life, no matter how long you live?

- Do you have access to your savings in case you want to withdraw money after your retirement paycheck has started?

- Can your income increase in future years, either due to good investment performance or features of the RIG?

- Is your retirement paycheck protected from decreasing if you experience poor investment performance or you live a long time?

- When you die, are unused funds available for a legacy?

- How is your retirement paycheck taxed?

Each of these factors will influence the amount of your retirement paycheck. As you can see, there's no one-size-fits-all RIG. Depending on your needs and circumstances, you may want to use a combination of RIGs to diversify your retirement income and realize the advantages of each type of RIG.

Before making any decisions, it's important that you do your homework to select the retirement income strategy that best meets your situation. Then go enjoy your retirement.