Retirement income review: GLWB in retirement

(MoneyWatch) This post is the third in a series examining guaranteed lifetime withdrawal benefit products (GLWB) offered by insurance companies and other financial institutions. These hybrid products (also known as "guaranteed minimum withdrawal benefit" products) combine the features of both managed payouts and immediate annuities in an attempt to offer the advantages of each method of generating retirement income.

Today we'll look at how GLWB products work during your retirement (Please see my previous posts as background.)

Generating income in retirement

During retirement, you'll continue to invest your retirement savings in a portfolio allocated between stocks and bonds; this is often -- and conveniently -- done through a target date fund geared to retirees. Asset allocations to stocks typically range from 50-60 percent, with the remainder in bonds or cash investments.

Retirement income review: GLWB/GMWB

Focus on guaranteed lifetime withdrawal benefits

401(k) retirement income options coming your way

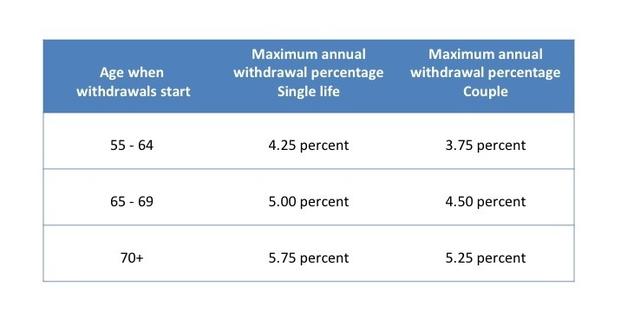

To generate retirement income, you'll apply the policy's maximum withdrawal percentage to the income base to determine the amount of your annual retirement income. The withdrawal percentage typically depends on your age and whether income is continued to your spouse or partner after you die. For example, with Prudential's IncomeFlex GLWB product, the maximum withdrawal rates are as follows:

Using the numbers above as an example, suppose you and your spouse are both age 65 and your income base is $100,000. Your policy's withdrawal percentage would be 4.5 percent, and your initial retirement income would be $4,500 per year, or $375 per month. (The maximum withdrawal percentages for other GLWB products are similar to the numbers shown above for Prudential's IncomeFlex.)

You typically lock in your withdrawal percentage when you start your benefits. So if the withdrawal percentages are similar to the above table, it would be a good idea to start your retirement income when you're at the bottom of an age bracket. For example, you wouldn't want to start benefits at age 64, when one year later the withdrawal percentage increases. Be sure to read the policy's fine print to understand if and how your withdrawal percentage would be adjusted once you start making withdrawals.

The income base continues to be increased for investment earnings and decreased by investment expenses and the insurance company's charges for the guarantees, just as they were in the accumulation phase. In addition, the income base is decreased by the amount of previous withdrawals for retirement income. Periodically -- typically annually -- the withdrawal percentage is reapplied to the income base, and if the income base at the time is higher than your previous income base, your retirement income will increase. This gives some potential for your retirement income to increase if your funds perform well.

Guarding against stock swings

If the stock or bond markets decline, however, your retirement income will never decrease below the amount of your initial retirement paycheck as long as you don't withdraw more than the maximum withdrawal amount (which is the maximum withdrawal percentage applied to the income base). This income amount is guaranteed for the rest of your life and that of your spouse or partner, if you elect to cover your beneficiary.

If there's still a positive value in your savings when you die (and after your spouse or partner dies), then this amount is paid to your designated beneficiary or charity. Often this amount is the market value of your savings without the guarantees on your account, not the income base that reflects the guarantees.

You're allowed to withdraw more than the amount dictated by the withdrawal percentage, but that will reduce the amount of your retirement income and may reduce or eliminate your lifetime guaranteed income. Again, the policy's fine print will spell out how the policy calculates the income base, "surrender value," and guaranteed retirement income once your retirement paycheck starts.

Understand how the fees work

The best GLWB products will charge from 150 to 200 basis points (1.5 to 2 percent) each year for both investment management expenses and the insurance guarantee. These charges would be applied to your income base during the year and used to carry forward your income base to the next year.

For example, Prudential's IncomeFlex product charges:

- 1 percent each year for the insurance guarantee, plus

- Investment management expenses ranging from 0.59 to 0.94 percent, depending on the fund an investor chooses

The result is total annual charges that range from 1.59 to 1.94 percent. Prudential reserves the right to increase the 1 percent insurance charge to as much as 1.5 percent for future contributions and for future step-ups in the income base.

Similarly, Vanguard's Variable Annuity with the GLWB rider charges:

- 0.95 percent each year for the insurance guarantee, plus

- Investment management and administrative expenses ranging from 0.17 to 0.51 percent, depending on the fund an investor chooses

This results in total annual charges that range from 1.12 to 1.46 percent. Vanguard reserves the right to increase the 0.95 percent insurance charge to as much as 2.0 percent.

Note, however, that some retail GLWB products can assess total charges well above 200 basis points (2 percent), with some reaching as high as 300 basis points (3 percent). Charges at this level create quite a drag on your investment performance, which means it can take an exceptionally great year in the stock market to increase your income base. My advice? Stick with GLWB products that have total charges below 200 basis points.

Are GLWB products a good way to generate a retirement income that's guaranteed for the rest of your life and gives you some upside potential if the stock market does well? Stay tuned for my next post, which offers an example to help you answer this question.