Are GLWB products a good value?

(MoneyWatch) This post is the fifth and final post in a series examining guaranteed lifetime withdrawal benefit products (GLWB) offered by insurance companies and other financial institutions. These hybrid products (also known as "guaranteed minimum withdrawal benefit" products) combine the features of both managed payouts and immediate annuities in an attempt to offer the advantages of each method of generating retirement income.

Today we'll answer the question most readers are curious about regarding GLWB products: Do they offer the best of both worlds -- managed payouts and immediate annuities -- when it comes to generating retirement income? (You may want to review my previous four posts at the following links to get up to speed on the topic.)

Retirement income review: GLWB/GMWB

Focus on guaranteed lifetime withdrawal benefits

Retirement income review: GLWB in retirement

Can GLWB products protect retirement income?

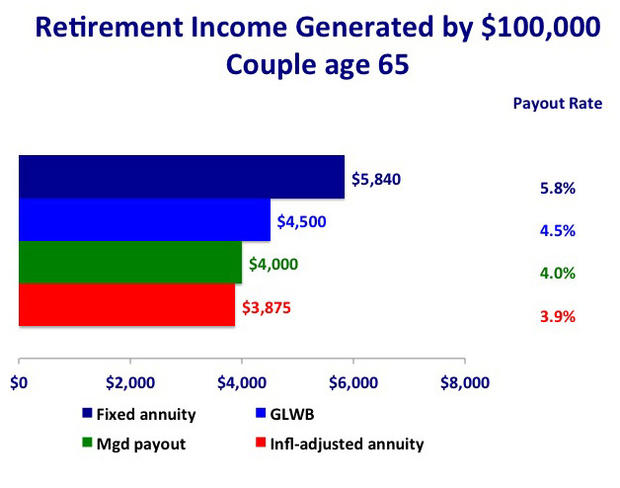

The fact of the matter is, the answer to the above question will depend on your goals and how much retirement income you need. GLWB products offer features of both immediate annuities and managed payouts and provide an initial amount of retirement income that falls somewhere between these methods. The following graph compares the initial retirement income you can generate with a GLWB product to what you'd earn from both managed payouts and fixed and inflation-adjusted immediate annuities, using income amounts for a married couple from my April 2012 retirement income scorecard.

This graph shows that the initial retirement income with a GLWB product is higher compared to inflation-adjusted annuities and managed payouts using the four percent rule, but lower than the amount of income from immediate fixed annuities. The comparisons are similar for single men and women.

My most recent postdescribed how GLWB products can boost your retirement income if your investments perform well, but that it would take consistently high rates of return to generate meaningful increases in your retirement income.

As a result, you'll most likely realize higher total retirement income over your lifetime with fixed or inflation-adjusted immediate annuities. Remember, however, that if you invest in these annuities, you have two disadvantages that don't apply to a GLWB product: You can't access your savings once you start the annuity, and you can't leave a monetary legacy, even if you die soon after your retirement income starts.

By comparison, managed payouts will likely offer more flexible access to your savings and a higher legacy value when you die. The downside with this investment vehicle is that it doesn't offer a guaranteed lifetime retirement income impervious to a downturn in the financial markets.

Wade Pfau, a chartered financial analyst and associate professor of economics at the National Graduate Institute for Policy Studies in Tokyo, writes an excellent blog on retirement income issues. In a recent post, he compared Vanguard's GLWB product with managed payouts. Pfau concluded that managed payouts are likely to produce a higher retirement paycheck and higher legacy values than a GLWB product would. Purchasing a fixed immediate annuity might enable you to buy a guaranteed income source more cheaply than a GLWB product, he said, which is confirmed by the above graph.

When you compare retirement income-generating methods feature by feature, GLWB products likely won't come out on top for any specific feature. But they might come in second place for most features, while other methods can rank first in some ways but last in others. For some people, GLWB's second-place rankings in many categories might be a desirable outcome.

One important advantage that GLWB products offer is that they address the significant behavioral challenges that people sometimes have to generating retirement income. For example, if you like the guarantee of a lifetime retirement income but don't like traditional immediate annuities because you have to give up access to your assets, a GLWB product is the next best thing. Similarly, if you want to use managed payouts so you have access to your savings and because you can invest in the stock market for the potential of growth in your retirement savings and retirement income, but you're scared by the possibility of market crashes, then a GLWB product might also be the next best thing.

Do GLWB products add value?

The guarantees offered by GLWB products can be of value to people who want to protect their savings when they're close to retirement and to generate lifetime income in retirement. But invest in them with the idea that you'll stay with them throughout retirement and that you'll apply your retirement savings to generate retirement income.

Remember that the guarantees of most GLWB products don't apply to any money withdrawn before retirement. So if you withdraw all your money from a GLWB product before you retire because you've changed your mind, you'll have wasted the insurance fees that you paid over the years.

Please take the time to learn about GLWB products' features and how they compare to other methods of generating retirement income. It could be that other forms of generating retirement income might also meet your needs, or that you could also get the best of both worlds by splitting your retirement savings between managed payouts and traditional fixed annuities.

GLWB shopping tips

If you think a GLWB product might fit your circumstances, here are some shopping tips to help you choose wisely.

First, make sure that the total charges for investment management fees, insurance guarantees, and any other charges don't exceed 200 basis points (2 percent) of your income base. When you can get products with lower fees from Prudential, Vanguard, and other insurance companies, why pay more? High expense charges only reduce your retirement income.

Second, don't buy a retail GLWB product that pays a commission to an insurance agent. If someone is pitching you a GLWB product, ask point-blank if there's a commission. These charges only reduce your retirement savings, and there are other GLWB products that don't charge a commission.

Third, investigate whether the insurance company can increase the charge for insurance. Prudential and Vanguard both offer GLWB products that allow the insurance company to increase this charge up to 1.5 percent and 2 percent, respectively. This makes me nervous, but it's a fact of life with most GLWB products. I wouldn't accept any policy that can increase the insurance charge to more than 2 percent.

If you're interested in a specific GLWB product, I strongly encourage you to take the time to understand how the various features work. Don't invest in anything you don't understand! Most GLWB products offered in 401(k) plans have non-commissioned representatives who can answer your questions.

One last word of advice: As with other annuities, I suggest not investing all of your retirement savings in a GLWB product. It's prudent to diversify your sources of retirement income.

And as with any retirement income-generator, there are competitive GLWB products and products with charges that are just too high. Take the time to learn the difference -- it's a good use of your time.