Diversify the sources of your retirement income

(MoneyWatch) If you know anything at all about investing, you're most likely familiar with investment diversification -- the "don't put all your eggs in one basket" theory of investing. An important refinement of this theory is retirement income diversification.

- Retirement income scorecard: immediate annuities

- Boost your Social Security payout by $100,000

- How Warren Buffett would handle today's market

- Wells Fargo on what to do with rising interest rates

Because it's next to impossible for most of us to accurately predict when high inflation or a recession will occur, when interest rates will rise or fall and how the stock market will perform, this strategy can help you protect your retirement paycheck whatever direction the economy takes. Different sources of retirement income will enable you to withstand different economic challenges, so you'll be prepared no matter what happens.

As you may have read in my recent retirement income scorecard series, there are three types of retirement income generators (RIGs):

- RIG No. 1:Investment income, where you use just the interest and income from invested assets and don't touch the principal

- RIG No. 2: Systematic withdrawals, where you invest your retirement savings in a portfolio of stocks and bonds and then withdraw interest, dividends and principal systematically to avoid outliving your savings (though there are no guarantees)

- RIG No. 3: Immediate annuity, where you invest your savings with an insurance company and they guarantee to pay you a retirement income for as long as you live

Each RIG has its pros and cons, and each produces a retirement paycheck in different amounts, as you can see if you review my scorecard series.

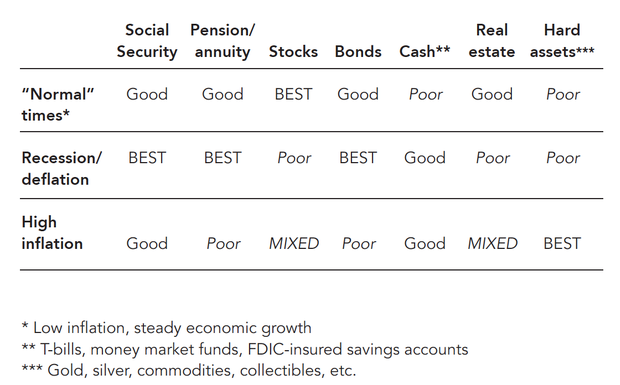

The table below -- an excerpt from my latest book, "Money for Life" -- explains in summaries why diversifying your sources of retirement income is an important goal. The table rates how different sources of retirement income fare in various economic climates: normal times, recession/deflation or high inflation.

Note that in this table that RIGs No. 1 and No. 2 -- investment income and systematic withdrawals -- are represented by investments in stocks, bonds, cash, real estate and hard assets.

Note first that Social Security benefits alone provide a good retirement paycheck in all three economic scenarios. This is one reason why maximizing your Social Security income is a good strategy. The other sources of income perform well in some climates but poorly in others.

Forecasts of future economic conditions are notoriously inaccurate. In fact, fellow CBS MoneyWatch bloggers Allan Roth and Larry Swedroe contend it's a fool's game. And given the likely length of your retirement, there's a good chance you'll experience all three economic environments. Which is why it pays to diversify your sources of retirement income.

The good news is that you can modify some RIGs -- investment income and systematic withdrawals -- to reflect changing economic winds, such as your investment strategy, asset allocation and the amount withdrawn from your savings. Other decisions cannot be revisited so easily, such as how to draw your pension, when to start Social Security benefits and whether and when you should purchase an immediate annuity. For that reason, it's also a good idea to have some sources of income that can be modified along the way.

Since many people may have to work during their retirement years, it might make sense to include wages as a source of retirement income in the above chart. In this case, I'd rate wages as "good" in both normal times and in times of high inflation, since they can be a reliable source of income. In a recession, however, wages qualify as good only if you can get and keep a job. If you can, wage income ranks up there with Social Security as a source of income that does well in all economic climates. Thus it's wise to keep your feet in the job market. But relying heavily on wage income if your job or industry is vulnerable to layoffs is a risky business. And understand that most likely you'll reach a point in your life when you won't be able to work.

If you're interested in learning more about the topic of generating reliable retirement income, my latest book, "Money for Life: Turn Your IRA and 401(k) Into a Lifetime Retirement Paycheck," explores in detail the diversification of your retirement income so you can survive inevitable economic downturns in your golden years.