A smart strategy for collecting Social Security

(MoneyWatch) Social Security benefits provide a significant proportion of retirement income for most Americans. Federal data shows that the government program provides 50 percent or more of all income for almost two-thirds of retirees, and 90 percent or more of all income for a little more than one-third of retirees.

One key takeaway in these stats: Low- and middle-income workers who optimize their Social Security benefits can significantly improve their financial security in retirement.

- Boost your Social Security payout by $100,000

- Boost your spouse's Social Security payout by $90,000

- U.S. government annuity for sale

- Retirement income scorecard: Immediate annuities

Yet roughly half of all Americans start Social Security benefits at age 62, the earliest possible age with the lowest amount of retirement income. Many analysts have demonstrated that this approach is less than ideal for people in average or above-average health, and that retirement security can be enhanced substantially by delaying the start of Social Security income. For instance, postponing the start of benefits from age 62 to age 66 can increase annual Social Security income by 33 percent, while delaying to age 70 can increase annual Social Security income by 76 percent.

John Shoven, director of the Stanford Institute for Economics Policy Research, recently co-authored with Sita Slavov a paper that explains how Americans can effectively delay the start of Social Security benefits. Most Americans use retirement savings to supplement Social Security income and start withdrawing from savings upon retirement, a method Shoven calls a "parallel" strategy. Instead, he advocates using a "series" strategy, in which retirees draw down retirement savings first to pay for living expenses and delay the start of Social Security benefits until age 70. In effect, retirement savings are used to "buy" a higher annuity from Social Security.

This effective "annuity purchase rate" is a much more favorable rate than the cost of annuities purchased from private insurance companies in today's market, as demonstrated in a recent post from fellow CBS MoneyWatch blogger Allan Roth. The reason is that Social Security's delayed retirement credits were developed when interest rates were much higher and life expectancies were lower compared to today, and before Social Security benefits were indexed for inflation. As a result, Social Security's delayed retirement credits are more than fair actuarially.

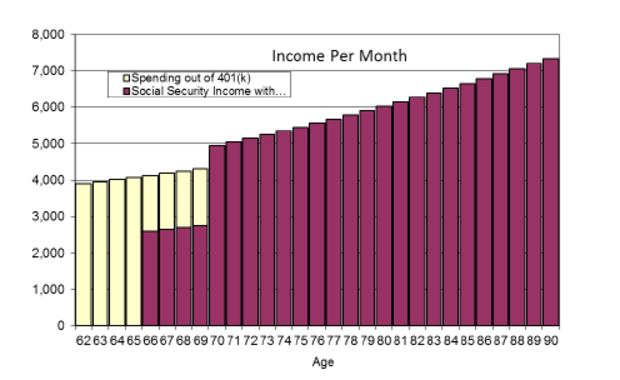

If you believe that "a picture is worth a thousand words," then here's a graph from the cover of Shoven's paper that illustrates his strategy.

Shoven's paper contains hypothetical examples of single retirees and couples who can increase their retirement incomes by several hundred dollars per month at age 70 if they delay Social Security benefits for the primary wage earner from age 62 to age 70. The increase in retirement income from deploying this strategy translates to $1,000 to $1,400 per month by the late 80s and 90s. In one example, the gain in the expected present value of retirement income was $200,000.

For many retirees, these increases may represent the difference between poverty and comfort. Boomers will need to squeeze as much retirement income out of their meager savings as possible, and the strategy advocated by Shoven is a good way to do that. The bonus is that the delayed retirement credit is reflected in survivors' benefits, so delaying the start of Social Security will also improve the financial security of widows and widowers.

Shoven's paper is written for the layperson, and contains details on Social Security benefits and the strategies he advocates. It also contains good background information for people who are serious about retirement planning.

I encourage you to take the time to determine the best strategy for starting your Social Security benefits. The time you spend thinking about this critical issue has the potential to boost your lifetime payout by $100,000 or more and your spouse's payout by $90,000 or more, so that's a very good use of your time.