Jamie Dimon says rejecting capitalism is "dead wrong" in CBS News interview

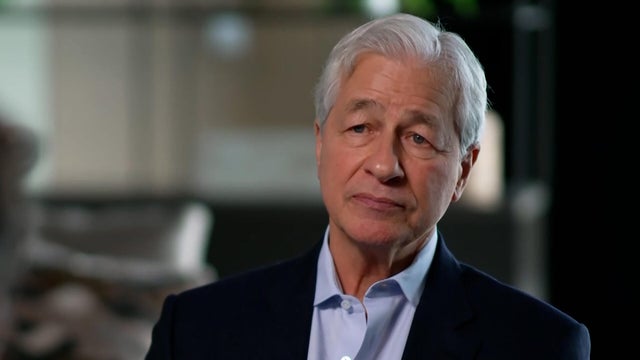

JPMorgan Chase CEO Jamie Dimon shares his thinking on capitalism, AI, prediction markets and more in an interview with "CBS Evening News" anchor Tony Dokoupil.

Watch CBS News

JPMorgan Chase CEO Jamie Dimon shares his thinking on capitalism, AI, prediction markets and more in an interview with "CBS Evening News" anchor Tony Dokoupil.

The average price of gas across the U.S. last reached $4 after Russia's invasion of Ukraine sent crude oil prices surging.

Jamie Dimon told "CBS Evening News" anchor Tony Dokoupil that "what's more important for the future of the world is that this war successfully conclude."

Full-time employees cut their 401(k) participation and contribution rates last year amid an affordability crunch, new research shows.

JPMorgan CEO Jamie Dimon thinks AI will shorten the work week and lead to medical breakthroughs, while acknowledging the technology's potential impact on the nation's workforce.

The JPMorgan Chase CEO said the bank may one day introduce prediction market features, but said "there's a bunch of stuff we won't do" in that space.

Shortages of helium, a byproduct of natural gas processing, could create problems for semiconductor and medical equipment manufacturers.

As the war with Iran continues, CBS News is tracking gas and oil prices. Find out how much more it costs to fill up your tank or heat your house.

The Department of Homeland Security said TSA agents should begin receiving pay as early as Monday, March 30.

Following major gold price changes in March, investors should consider these questions before starting this April.

Tax debt and tax liens aren't the same and misunderstanding the difference can cost you a lot over time.

Ignoring a wage garnishment notice can make a bad debt situation much worse. Here's what's actually at stake.

CBS News is tracking the rising cost of products most impacted by tariffs imposed and soon-to-be-imposed by President Trump, from grocery items to cars and trucks.

These charts track prices consumers pay for groceries and other goods now compared to five years ago.

Full-time employees cut their 401(k) participation and contribution rates last year amid an affordability crunch, new research shows.

With Social Security's trust fund sliding toward insolvency, one group wants to cap benefits for the wealthiest U.S. couples.

More Americans are digging into their retirement savings for emergency expenses, research from Vanguard shows.

More employees are clinging to their positions in a trend known as "job-hugging." That's making it harder for job-seekers to find work.

A college degree still provides an edge when it comes to finding a good job, but a person's major may be just as important to career stability, research suggests.

"Reverse recruitment" firms promise to cut the length of job searches in half and help connect candidates with employers.

Just hours earlier, an Army spokesperson said the crew had been suspended from flying while the Army conducts a formal investigation into why the Apache helicopters flew near Kid Rock's Nashville house.

Tiger Woods announced Tuesday that he's "stepping away for a period of time to seek treatment" after pleading not guilty to charges including driving under the influence.

JPMorgan Chase CEO Jamie Dimon shares his thinking on capitalism, AI, prediction markets and more in an interview with "CBS Evening News" anchor Tony Dokoupil.

The JPMorgan Chase CEO said the bank may one day introduce prediction market features, but said "there's a bunch of stuff we won't do" in that space.

President Trump has long wanted to place additional restrictions on mail-in voting, which he has called "mail-in cheating."

JPMorgan Chase CEO Jamie Dimon shares his thinking on capitalism, AI, prediction markets and more in an interview with "CBS Evening News" anchor Tony Dokoupil.

The JPMorgan Chase CEO said the bank may one day introduce prediction market features, but said "there's a bunch of stuff we won't do" in that space.

JPMorgan CEO Jamie Dimon thinks AI will shorten the work week and lead to medical breakthroughs, while acknowledging the technology's potential impact on the nation's workforce.

Full-time employees cut their 401(k) participation and contribution rates last year amid an affordability crunch, new research shows.

Jamie Dimon told "CBS Evening News" anchor Tony Dokoupil that "what's more important for the future of the world is that this war successfully conclude."

President Trump is planning to go to the Supreme Court on Wednesday as the justices take up his executive order seeking to end birthright citizenship, a major test of his immigration agenda.

A federal judge directed the Trump administration to restore the legal status of migrants allowed into the U.S. under a now-defunct Biden administration program for asylum-seekers who arrived at the southern border.

President Trump is planning to deliver a prime-time address Wednesday night to "provide an important update on Iran," the White House said, as the president faces critical decisions in the monthlong war.

Just hours earlier, an Army spokesperson said the crew had been suspended from flying while the Army conducts a formal investigation into why the Apache helicopters flew near Kid Rock's Nashville house.

President Trump has long wanted to place additional restrictions on mail-in voting, which he has called "mail-in cheating."

The One Big Beautiful Bill Act will add red tape and restrictions for those seeking Medicaid and SNAP benefits. And the costs to update computer systems that determine eligibility for those programs will be steep.

David Lyon is one of the rising number of young adults to be diagnosed with colorectal cancer.

Here's what to know about peptides, what they can and can't do, and what's driving viral claims about possible health benefits online.

Dr. Jay Bhattacharya, head of the National Institutes of Health and interim leader of the Centers for Disease Control and Prevention, told staff a permanent CDC director could be nominated soon. "I know that it has been such a difficult year," he said.

Federal health officials posted a warning about misleading statements by biotech billionaire Dr. Patrick Soon-Shiong about his company's bladder cancer drug Anktiva.

American journalist Shelly Kittleson was kidnapped in Baghdad on Tuesday, according to two sources familiar with the matter as well as an Iraqi official.

Shortages of helium, a byproduct of natural gas processing, could create problems for semiconductor and medical equipment manufacturers.

Defense Secretary Pete Hegseth is tentatively expected to testify publicly before the House Armed Services Committee on April 29, according to two sources familiar with the plans.

Police said two people headed the network, including one person considered to be the "narco-architect" and "mastermind of the tunnels."

Palestinian parents separated from their premature newborns by the war in Gaza finally get to meet their children for the first time.

Kid Rock posted videos of the helicopters hovering by his Nashville home on social media over the weekend. The Army later confirmed the helicopters were on a training mission.

Taylor Swift is being sued by Las Vegas performer Maren Wade who has accused the superstar of trademark infringement over her latest album, "The Life of a Showgirl." Wade is the creator of the "Confessions of a Showgirl" podcast, which started as a column in 2014.

Sharon Stone reflected on her legendary career as she discussed joining the cast of "Euphoria," working with the show's creator, Sam Levinson, and how she has advocated for women in the entertainment industry.

A Las Vegas performer has sued Taylor Swift over the title of her hit album "The Life of a Showgirl," alleging it violates the performer's trademark.

A Barbie Dream Fest event in Fort Lauderdale, Florida, generated backlash from attendees over its allegedly underwhelming experience. Jessica Nova, who drove in from Atlanta for the occasion, joins CBS News to recount her experience.

CBS News contributor Patrick McGee joins "The Daily Report" to discuss the codependent relationship between Apple and China, a country that manufactures hundreds of millions of iPhones every year.

The JPMorgan Chase CEO said the bank may one day introduce prediction market features, but said "there's a bunch of stuff we won't do" in that space.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

Many have dreamed of a future with flying cars, eliminating traffic on the morning commute. One company is trying to make that dream a reality. Itay Hod reports.

A judge has temporarily blocked the Pentagon's attempt to designate Anthropic as a supply chain risk. CBS News legal contributor Jessica Levinson joins with analysis.

According to a recent report, nearly one in four species catalogued by the CMS are threatened with extinction on a worldwide scale.

NASA is poised to launch four astronauts April 1 on a historic nine-day trip around the moon and back. Here's everything to know about the Artemis II mission.

Arctic sea ice levels are crucial to Earth's climate because, without the ice reflecting sunlight, more heat energy goes into the oceans.

Marine biologists found detectable levels of caffeine, cocaine and the over-the-counter painkillers in the blood of 28 sharks.

Here's what to know about peptides, what they can and can't do, and what's driving viral claims about possible health benefits online.

Lawyers for the man accused of killing Charlie Kirk are asking to delay a preliminary hearing set for May, arguing the defense team needs time to review ATF analysis they contend "could not" connect a bullet fragment recovered during Kirk's autopsy with the rifle found near the scene of the crime. CBS News legal contributor Jessica Levinson joins to unpack the development.

Tiger Woods had bloodshot eyes, was "sweating profusely" and had "extremely dilated" pupils after a rollover car crash last week, an arrest report shows. CBS News' Shanelle Kaul has the details.

Police said two people headed the network, including one person considered to be the "narco-architect" and "mastermind of the tunnels."

Lawyers for Tyler Robinson, the man charged with killing conservative activist Charlie Kirk, are looking to review an analysis that couldn't conclusively connect a bullet fragment recovered during an autopsy to the rifle found near the scene. CBS News' Carter Evans reports.

A new court filing reveals defense attorneys for Tyler Robinson, the man accused of killing Charlie Kirk, claim an ATF analysis could not conclusively connect the bullet that killed Kirk to the gun Robinson allegedly used. Now the lawyers are asking to delay Robinson's preliminary hearing to review the evidence. Carter Evans reports.

Forecasters continue to predict an 80% chance of favorable weather on Wednesday for the launch of four astronauts on a flight to the moon.

Countdown clocks began ticking Monday, setting the stage for launch of the Artemis II moon mission early Wednesday evening.

NASA's Artemis II astronauts — three space station veterans and a Canadian rookie — stand out even in an astronaut corps full of super achievers.

NASA is poised to launch four astronauts April 1 on a historic nine-day trip around the moon and back. Here's everything to know about the Artemis II mission.

The countdown to launch of the Artemis II crew's flight around the moon begins Monday at the Kennedy Space Center in Florida.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

Does the evidence show a cover-up, or was Todd Kendhammer wrongfully convicted for the murder of his wife?

Christy Salters-Martin dominated in the boxing ring but faced her toughest challenger at home.

Family seeks answers in death of newlywed who disappeared in 2005 while on Mediterranean honeymoon cruise.

Meet the tattooed beauty charged in the death of Google executive Forrest Hayes.

NASA is planning to launch its first crewed mission in over 50 years with its Artemis II flight on Wednesday from Florida's Kennedy Space Center.

JPMorgan Chase CEO Jamie Dimon speaks with "CBS Evening News" anchor Tony Dokoupil about the advancement of artificial intelligence, the war in Iran's effect on the U.S. economy, prediction markets and more.

Born with a rare heart defect, Wyatt Lopez was about a year old when he checked into the hospital. It took almost a whole year before he checked back out -- with a tuxedo, a little parade and a brand new heart. Tony Dokoupil has the story.

The head of JPMorgan Chase is acknowledging that the American dream is slipping out of reach for many. Jamie Dimon spoke to Tony Dokoupil, saying he's on a crusade to change that.

The countdown to launch of the Artemis II mission, NASA's first piloted moonshot in half a century, proceeded smoothly as engineers and technicians prepared the agency's giant Space Launch System rocket and Orion crew capsule for fueling and blastoff. Mark Strassmann has more.