Investors punish funds for bad behavior

(MoneyWatch) It's a fact of investing life that investors tend to chase performance by moving into what has recently been hot. That's why for every single fund family, the returns investors have actually received over the past 10 years have lagged the performance of the funds themselves. (Investors don't actually put their money into the fund until after it has performed well, so they miss some, if not all, of the upside.) And according to a Morningstar analysis titled "It pays to mind the gap," the larger the lag, the more trouble the fund family has had gathering assets.

A little background

To see how investor return can lag the fund return, consider this fictional example. Let's say that in 2010, the Allan Roth Global Performance Chasing Fund (ARGPCF) had $100 million in assets and earned 20 percent. Because I was so good at marketing my fictional brilliance, I attracted another $900 million at the start of 2010. Unfortunately, my luck ran out on my billion dollar fund and I lost 15 percent in 2011 for my investors. The math reveals that the fund earned an annual 1.0 percent positive return while investors (as a whole) lost 6.9 percent annually over the two year period. So I attracted $1 billion in capital and lost $133 million, making the gap between my investor return and the fund return 7.9 percent.

Morningstar's forward ratings

Morningstar grades 10 largest fund families

Have DFA advisors helped clients avoid mistakes?

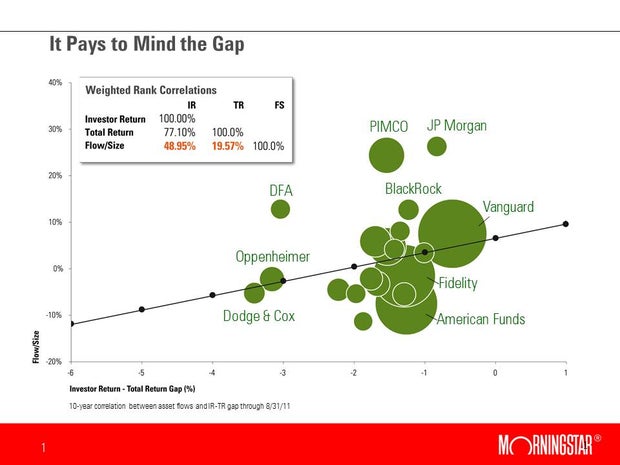

In the graph below, Morningstar has plotted the 10 year gaps between fund family return and investor return against each family's ability to attract more investor capital. It turns out that fund families that minimized the gap in bad behavior (performance chasing) generally attracted more investor capital. Fund families that attracted bad behavior (larger gaps) declined.

The four families with the least bad behavior, Vanguard, JP Morgan, PIMCO and Blackrock all attracted new investor money at a pretty healthy clip. Three fund families had a behavior gap of roughly 3 percentage points or more -- DFA, Oppenheimer, and Dodge and Cox. All but DFA saw investors taking funds from those families.

Don Phillips, president of Morningstar's Investment Research division, notes in past studies that DFA has had very small gaps. The more recent numbers reflect the huge gaps in the company's emerging market funds as institutions and advisors poured money into these funds, which subsequently had weak performance. Phillips says the gap will narrow if emerging market stocks turn around.

The bottom line

Performance chasing has been known to be hazardous to your wealth. I've heard a fund manager or two say it isn't their fault if investors flock to their funds after great performance. It turns out, however, that the fund family may benefit by discouraging the performance chasing. Thus, closing a hot fund to new investors for a period of time is not only in the best interests of the investor, it is probably in the best interests of the fund family itself.