Have DFA advisors helped clients avoid mistakes?

Earlier this week, I examined DFA risk adjusted performance and presented the argument that DFA funds, despite their lofty reputation, have only clocked in average risk-adjusted returns. And these returns are average even before advisors charge for their services. Now I'm going to examine whether those advisor services added value.

DFA funds can only be purchased through advisors, therefore those advisors should be providing focus and discipline rather than chasing performance. As I have noted in the past, advisors in general did their clients no favors. Using TD Ameritrade's data, I found that financial advisors weighted clients' portfolios heavily toward stocks at the height of the market in 2007, only to turn to cash in early 2009, missing the rebound.

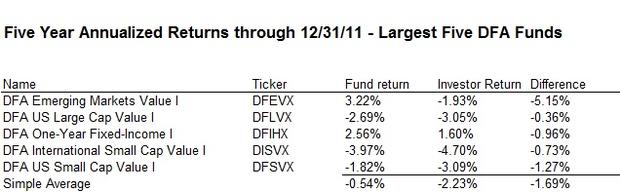

To examine the question as to whether DFA advisors were able to resist these all-too-human instincts of fear and greed, I researched five year returns of the five largest DFA funds. I compared the returns of each fund (geometric return) to the returns of the investors in each fund (dollar weighted). The results are shown below for the five year period ending December 31, 2011.

Each of the top five DFA funds showed lower investor returns than the funds themselves earned. This is evidence that the DFA advisors did show some performance chasing characteristics during the last five, very volatile, years. Though the simple average of the five funds lost 0.54 percent annually, the investor return was a negative 2.23 percent annually.

Investors lagged the fund return by 1.69 percent annually. Russel Kinnel, Director of Mutual Fund Research at Morningstar, was quick to point out that this was not a predictive indicator of how investors would fare in the future.

DFA vice president Weston Wellington responded by saying the measures in the Morningstar data included institutional assets. Thus, the lower investor return could be attributed to either institutional investors or advisor accounts, or both.

Performance Chasing at Vanguard?

For the most part, Vanguard funds are purchased directly, rather than through advisors. I wanted to do the same comparison between investor returns and fund returns for Vanguard, to see how performance chasing at Vanguard compared to DFA.

While it seemed like a very simple analysis, Kinnel cautioned me against this analysis. That's because Vanguard has several different share classes, and we can't conclude whether or not cash is merely being transferred to different share class. For example, when Vanguard lowered the minimum investment for lower cost Admiral Index funds to $10,000, large amounts of assets moved from the investor classes to admiral class funds.

While far from conclusive, I examined some share classes of Vanguard's total US stock funds, total international stock funds, and total bond funds. I actually found investors did better than the funds for the total US stock funds, and trailed a bit in international stocks and bond funds. Even where there was underperformance, it was less than the 1.69 percent shortfall averaged at the largest five DFA funds.

My take

It appears that there is strong evidence that DFA advisors have significantly underperformed in the largest five DFA funds over the past five years. It is possible that all of the underperformance came from institutional investors, but I see no data or logic to support this. Advisors in other funds also have a track record of chasing performance.

Should you invest in DFA funds?

DFA vs Vanguard -- which is better?

If everyone indexed -- a fantasy

Again, while not conclusive, there is some evidence that investors in the broad index funds showed more focus and less performance chasing, as investor returns were closer to the returns of the funds themselves for the share classes examined.

Thus, the conclusion from this piece, combined with the earlier piece on Morningstar ratings, shows:

-- DFA funds are average performers on a risk adjusted basis.

-- DFA advisors further reduced returns over the past five years by poor timing.

I personally own five DFA funds and won't be selling them based on my findings. I have far more invested in Vanguard funds, and this serves to confirm my belief that Vanguard outperforms on a risk adjusted basis. Vanguard's weighted average rating is a 3.6 star versus the 3.0 for DFA.

What this means for your portfolio is something you will have to decide. As an advisor, of course, I don't have to charge myself an advisory fee to hold DFA funds. The fact that, even without an additional advisory fee, I hold far more Vanguard funds than DFA tells you where I come out on the argument of DFA vs. Vanguard. That said, both Vanguard and DFA are outstanding fund families.