Why oil prices matter now -- more than usual

Heading into the end of the year, energy prices look ready to jump back on the front pages. And that may not be a good thing.

Of all the economic indicators, little matters more to the average red-blooded American than the price of a gallon of unleaded gasoline. It’s universal. It’s fast changing. And unless you’re really into battery-powered electrics or Uber, it’s just something you can’t get away from.

Lately, though, the vagaries of gasoline -- driven by the ups and down of crude oil -- have been even more important than usual. Ever since energy prices peaked in the summer of 2014 before collapsing nearly 80 percent into last February’s lows, the health of the stock market, the economy, the U.S. dollar, corporate earnings and the prospect of Federal Reserve rate hikes have all depended on where oil is headed.

And although oil and gasoline prices haven’t really changed since March, another bout of volatility looks likely as the U.S. summer driving season comes to an end.

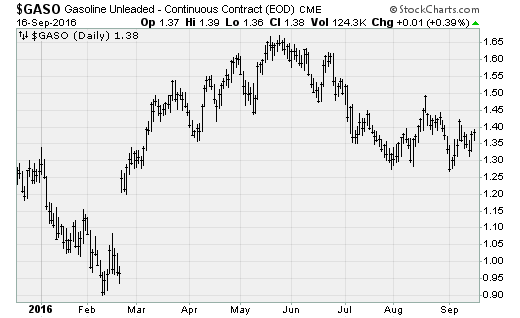

The wholesale price of a gallon of gasoline continues to trade in a tight three-month range between $1.27 and $1.49 (chart above), a range that was in play in late 2015 as well.

The fundamentals suggest another bout of weakness is coming. Ed Yardeni of Yardeni Research highlights that the combination of weak demand (both from refineries and end consumers) and increased OPEC output (as Iran ramps up production as economic sanctions are lifted under the nuclear deal) swelled inventories in the developed economies to a record 3.1 billion barrels in July.

Last week, the International Energy Agency (IEA) predicted that the oversupply in the global oil markets will last for longer than previously expected. As a result, it estimated oil stockpiles will keep climbing through 2017, marking the fourth consecutive year of surplus. This was a major change from estimates the agency made as recently as August that showed the market returning to equilibrium later this year.

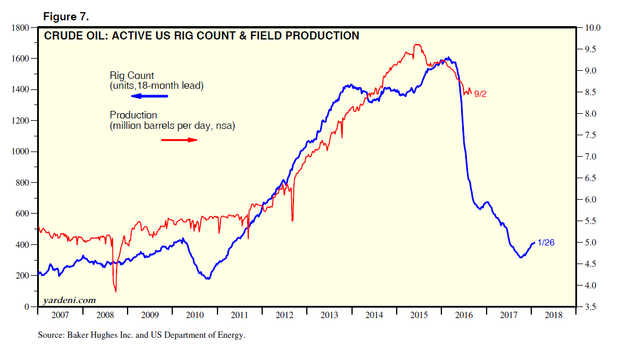

And while U.S. drilling rig counts have dropped precipitously from their 2014 highs, steady prices have encouraged a rebound in recent weeks (chart below). What’s more, exploration activity is ongoing, and Apache (APA) announced earlier this month that it has discovered at least 2 billion barrels of oil and gas equivalents in a new field in West Texas that geologists and engineers had previously written off.

If this weren’t enough, the U.S. Department of Energy released its “Long-Term Strategic Review of the U.S. Strategic Petroleum Reserve” and found that the SPR’s current level of nearly 700 million barrels should be reduced to a more appropriate level of 530 million-600 million barrels. With the U.S. growing in its role as one of the world’s largest energy producers, the threat of a supply disruption is fading.

Should the SPR be culled, that would throw millions of additional barrels of supply onto an already swamped market.

With the energy outlook tepid, and thus inflation measures relatively calm, the Fed is under little pressure to hike interest rates this year amid a batch of underwhelming economic data (including factory orders, manufacturing activity, construction spending and more). And unless oil prices bounce back, corporate earnings are likely to continue to fall. FactSet already anticipates S&P 500 profitability will fall for the sixth consecutive quarter in the third quarter -- mainly due to the estimated 66 percent year-over-year drop in energy sector earnings.

The wildcard is an upcoming OPEC meeting in Algiers later this month. But Capital Economics doesn’t believe a teased output freeze will actually come to fruition based on the cartel’s history of overpromising and underdelivering, as it did earlier this year.

Iran remains recalcitrant as it seeks to crank up its production to pre-sanctions output levels. And amid production disruptions in Nigeria and Libya, these countries won’t be interested in freezing output at current levels.

Overall, another bout of weakness in oil prices -- while undoubtedly great news for American drivers -- would probably be a net negative for the economy and the stock market -- and it could lead to a repeat of the last January’s and February’s unpleasantness.

At this point, aside from a surprise interest rate hike from the Fed, this is the largest single potential worry for stocks heading into the presidential election in November.