Here's a Social Security strategy worth pondering

Is it a good idea to start your Social Security benefits as early as possible (at age 62), even if you don't need the income right away to meet your living expenses, and then invest this money for future use? A few readers asked this question in response to my recent post that analyzed the retirement income solutions that generated the highest retirement paycheck.

That's a good question, and there are a few different ways to look at it. The answer depends on four important factors:

- The rate of return you earn on the invested income

- The rate that Social Security benefits are increased for cost-of-living

- What you'll eventually do with the benefits you invest

- How long you'll live

To shed some light on this question and the possible answers, let's look at one simple example that compares two people who both retire at age 62. One starts Social Security right away and invests the money, while the other waits until age 70 to start receiving Social Security benefits. In both cases, these individuals have other sources of income from age 62 to 70, so neither of them will have to rely on Social Security to cover their living expenses until age 70.

The big picture

Does the "start early and invest" strategy result in more income at age 70 and beyond than what you'd get if you'd waited until age 70 to start your Social Security benefits? Here's the high-level answer to that question:

- Most likely, you'll be better off starting Social Security benefits early if you invest those funds in the stock market and achieve good rates of return, and/or if you die before your average life expectancy.

- You'll want to consider delaying benefits if you plan to invest in bonds or don't expect to earn good rates of return in the stock market, and/or if you live beyond your average life expectancy.

The details

Now let's dig into the analysis that supports these conclusions, using the two hypothetical retirees:

- Bob and Barbara were both born in 1953 and both intend to retire this year when they turn 62. Both had an identical earnings history, are currently earning $75,000 per year and earned similar amounts throughout their careers.

- Bob plans to start his Social Security benefits this year and will receive $1,500 per month, due to the reduction for starting benefits before age 66, his full retirement age. He'll invest this money until age 70, when he plans to start drawing from these accumulated savings to help meet his living expenses.

- Barbara plans to start her Social Security income at age 70, at which time her benefit will have grown to $2,640 per month due to the delayed retirement credit.

- Both Bob's and Barbara's Social Security benefits will increase because of cost-of-living adjustments (COLAs) after age 62. For the purpose of this analysis, I assumed COLAs of 2 percent per year (the 2015 increase was 1.7 percent).

To help determine if Bob made the best choice to begin taking his Social Security benefits as soon as possible, I added up his Social Security income of $1,500 per month from age 62 to 70, increased for the assumed COLA each year, then calculated the investment income he would earn at various rates of return until age 70. At that time, I assumed Bob would draw enough money from his accumulated savings so that when he adds these withdrawals to his Social Security income, he has as much income as Barbara, who waited until age 70 to start her Social Security income.

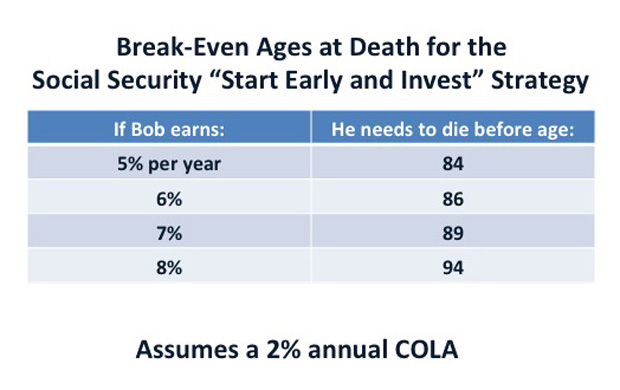

How long will Bob's invested Social Security assets last? After these assets are depleted, Bob's total income will come from just his Social Security income, so he needs to die before a "breakeven" age to make the "start early and invest" method a good move. How long his assets will last depends on the rate of return he earns, as summarized below:

Bob "wins" if his savings earn amounts higher than the rates shown in the above table or if he dies before the ages shown. He "loses" if he earns rates below the amounts shown or lives beyond the ages shown.

How should you interpret these results?

First, let's consider investment returns. In today's financial environment, you need to take risks in the stock market or assume bond yield or maturity risk if you hope to earn returns of 5 percent or more (though there's no guarantee that you will). If you're comfortable assuming stock market risk, however, it's easily possible that you could achieve annual returns that exceed the amounts shown on the table.

Now let's consider life expectancies. The average age at death for a man who is now 62 years old ranges from 81 to 82. For a 62-year-old woman, it's 83 to 84. But it's misleading to rely on life expectancies for the general population. You can easily add five to seven years to your life expectancy if you take care of your health, are more affluent than average and have an above-average education. So, there could be a good chance you'll live beyond the ages shown above.

How do the results change for COLAs other than the 2 percent I assumed? A 3 percent COLA hurts the "start early and invest" strategy by pushing back the breakeven ages at death by two to three years. A lower COLA helps the "start early and invest" strategy.

Your feelings about risk will also influence how you might act on these scenarios. Some people are comfortable with the uncertainty regarding stock market returns and are willing to assume the risk that their investments might decline as an acceptable trade-off for the potential that they might earn really good returns with stocks.

These people may also have other sources of retirement income or have a comfortable margin between their living expenses and their total retirement income, both of which may make them feel less anxious about a drop in their earnings. For these people, "start early and invest" might make sense.

Other people might consider Social Security to be the foundation of their retirement income, and they won't want to take any chances with it. Or they might be living on the edge when it comes to money, with little tolerance for declines in retirement income caused by stock market crashes. For these people, "start early and invest" wouldn't make sense.

You should consider other scenarios as well. For example, what if you never need the Social Security income to cover your living expenses and you simply want to invest your benefits to accumulate for a legacy? Or what if you retire at a different age than 62 or start Social Security at different ages?

The above simple analysis also didn't consider a number of important factors, such as how much you pay in income taxes, whether you or your partner are eligible for Social Security spousal benefits and the sequence of returns risk with stocks. It's likely these alternative scenarios and other factors won't change the basic conclusions, although they could affect the specific amounts of breakeven returns or life expectancies.

Finally, let me emphasize some behavioral aspects of this decision. You must be realistic with yourself if you're considering starting your Social Security benefits early and investing the money until age 70: Do you have the discipline to actually follow through? One of my friends started Social Security early, rationalizing that he'd invest the money. Then he ended up spending the extra income on a new car and expensive vacations.

In addition, consider if you still want to be paying attention to your investments when you reach your 80s and beyond, or do you want your retirement income to be on autopilot (which is the case for Social Security).

As you can see, this calculus has a lot of moving parts and a number of things to ponder before making a decision. The answers aren't certain or obvious. So, it's well worth your time to put together a thoughtful retirement income strategy that considers all your financial resources and your temperament for taking investment risk.

Your future self will thank you when you reach your 80s and 90s with an adequate retirement income.