Even the Fed is worried about the "Goldilocks" market

Smell that? It's euphoria in the air.

US equities surged higher on Tuesday, posting their best one-day gain since September despite a ballistic missile launch by North Korea and an apparent breakdown in bipartisan budget talks. Bank stocks rallied sharply, thanks to the GOP's tax overhaul getting through the Senate Budget Committee -- clearing the way for a vote by the whole chamber later this week.

Also adding to sentiment was a comfortable reception to Federal Reserve Governor Jerome Powell's confirmation hearing in his bid to become the next Fed chairman. As a result, the Dow Jones industrials index is closing in on the 24,000 level, just a month after crossing the 23,000 threshold, in what has been one of the most persistent, volatility-free uptrends in history.

But now, even the Fed is adding its voice to the chorus of Wall Street analysts worried the market has gone too far and is ripe of a nasty turnaround. In the minutes of its latest policy meeting, Fed officials expressed concerns about market "imbalances" and the possibility of a "sharp reversal" in prices.

In a recent note to clients, Morgan Stanley (MS) analysts warned that heading into the new year, "markets seem very late cycle, and valuations look extremely rich." They anticipate trouble will start to materialize in the credit markets, which typically sniff out a rise in default rates one year ahead of time.

Goldman Sachs (GS) warned that the "goldilocks" conditions that have fueled the market's rise -- complacency fueled by low volatility and central bank largesse -- are unlikely to continue into 2018.

Consider this: If stocks finish November near current levels, it will represent the 13th consecutive monthly gain on a total return basis. That hasn't happened in the 90 years of tracking this data.

Given this and the approach of another Fed rate hike in December, it's not surprising that the CBOE Volatility Index -- known as Wall Street's "fear gauge" -- has been creeping higher lately (shown in the upper pane of the chart above, vs. the S&P 500 in the lower pane). That's a sign hedgers are moving into downside protection in case Congress can't deliver major policy victories on taxes and the budget on such a tight timetable.

But the bears might have a wait until the calendar actually flips to 2018 for the carnage to start.

The folks at Almanac Trader noted that since 1987, the S&P 500 has logged post-Thanksgiving gains in 22 out of 30 years through New Year's Day.

Jason Goepfert at SentimenTrader pointed out conflicting signals between narrow market breadth and positive seasonality and momentum signals. The lack of volatility has been an anomaly as well, with stocks powering through the normally turbulent months of September and October like they weren't there.

There has also been a recent upward surge in Goepfert's "Smart Money Confidence" indicator, something that has presaged further gains during this bull market: The S&P 500 was higher a month later 70 percent of the time by an average of just under 1 percent.

But troublesome signs remain.

This is one of the longest and most expensive bull markets ever. A growing number of stocks are pushing to new lows -- setting off a cluster of ominous-sounding technical patterns including "Hindenburg Omens" and "Titanic Syndromes." Consumer confidence is off the charts high, and financial conditions are pushing to new levels of easiness (something the Fed isn't happy about). And cash levels are low.

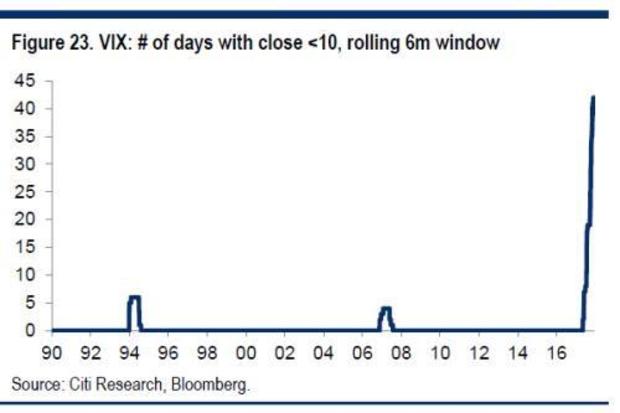

Just check out the chart from Citigroup (C) (above), which shows the level of complacency or persistent strength, depending on your bent, illustrating the number of consecutive days the VIX has been below 10.

There's no other way to say this: The Fed's easy money has created a monster. And now, the central bank is starting to fear it.