Why Trumpism is a threat to the U.S. dollar

As President Donald Trump heads to the World Economic Forum summit in Davos, Switzerland, to make a case for his America First economic philosophy to the (mostly skeptical) globalists in attendance, Wall Street is triumphant. That's something the president constantly raves about on Twitter. After all, the Dow Jones industrials index is easily bagging round-number victories at an accelerating pace. It took just two weeks to rise from 25,000 to 26,000.

Remember the last harrowing sell-off? Neither do I. Because Tuesday was the 445th day (a record) without a 3 percent pullback, according to Bespoke Investment Group. The last 20 percent pullback? That was 3,242 days ago -- #nomoredowndays.

The catalysts are familiar: Fueling economic and earnings growth expectations are the Trump administration's pro-business, anti-regulation, tax-cutting policies.

But there's a downside: President Trump's full-throated economic nationalism -- which sparked all those preelection fears among investors -- and with it, protectionist trade measures and the specter of deeper budget deficits.

Which is why the U.S. dollar has been gutted since Mr. Trump prepared to take office.

Of course, from a purely mercantilist perspective, this could secretly be a desired outcome. A frequent critic of China's outright manipulation of the yuan (to say nothing of Japan's long history of currency shenanigans), Mr. Trump no doubt understands that a cheaper currency directly translates into more competitive exports.

But some braggadocio is surely lost when the world believes your national currency -- and the world's reserve currency -- is suddenly not worth what it used to be. Moreover, the dollar's decline could eventually have some very serious knock-on effects on the president's precious stock market performance.

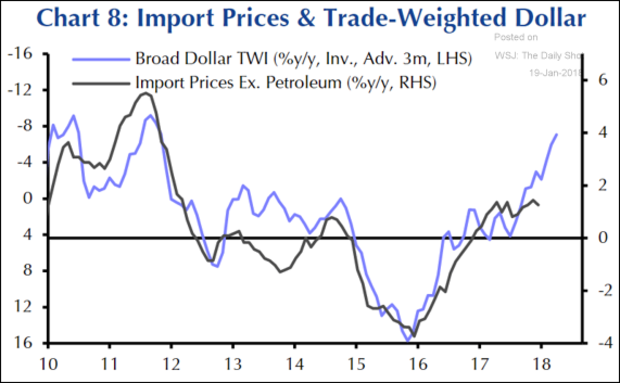

For one, a weaker dollar makes U.S. Treasury bonds less attractive to foreign buyers, providing an upward lift to yields and thus pushing borrowing costs higher for consumers. And two, a weaker dollar will boost inflation pressures by raising the cost of imports and commodities like crude oil, which is traded globally in U.S. dollars (chart above).

The latter, when mixed with the inflationary pressures of a rapidly tightening labor market, could push the Federal Reserve into a much more hawkish monetary policy stance in 2018. That would surely prick the sentiment bubble among the cheap-money junkies who call themselves investors these days.

Is Mr. Trump responsible? The market seems to have made that conclusion.

Consider: The U.S. dollar index peaked in the first week of January 2017 and has since lost 13.4 percent, returning to levels not seen since 2014. The sell-off has taken a new leg down since the end of December as Mr. Trump made clear that U.S. tariffs against imported solar panels and washing machines were likely (and since then enacted); amid rumors that the Chinese are threatening to slow their purchase of U.S. Treasury bonds; and worries that the president could unilaterally pull out of the North American Free Trade Agreement.

What about fears of America's creditworthiness?

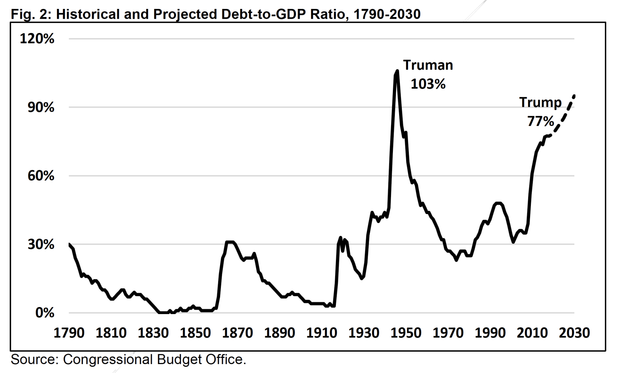

The Committee for a Responsible Federal Budget has warned that Mr. Trump's tax plan will cost more than $1 trillion over the next 10 years and cause the national debt as a share of the economy to swell further, returning to World War II highs (chart above).

Moreover, the temporary over-the-weekend government shutdown has given way to a short-term extension that pushes difficult issues like the federal budget, immigration and border wall funding into February -- butting up against the need to raise the debt ceiling, without which the risk of a national debt default becomes real.

Bank of America Merrill Lynch analysts noted some of these concerns -- rising trade protectionism and NAFTA negotiations -- in a recent note to clients. But they also raised their 2018 year-end S&P 500 price target to 3,000. Which means, for now, stock investors couldn't care less about the dollar's woes.

That'll change if the greenback's rout deepens and pushes crude oil past the $70-a-barrel threshold. This isn't the kind of round number Mr. Trump will want to brag about on Twitter.