Who the housing recovery is leaving behind

The economic recovery since the Great Recession has been hailed as unusually long, with over eight years of sustained job growth and GDP increases, and -- for the last few of those years -- income increases.

But when it comes to housing, the recovery has created a stark divide.

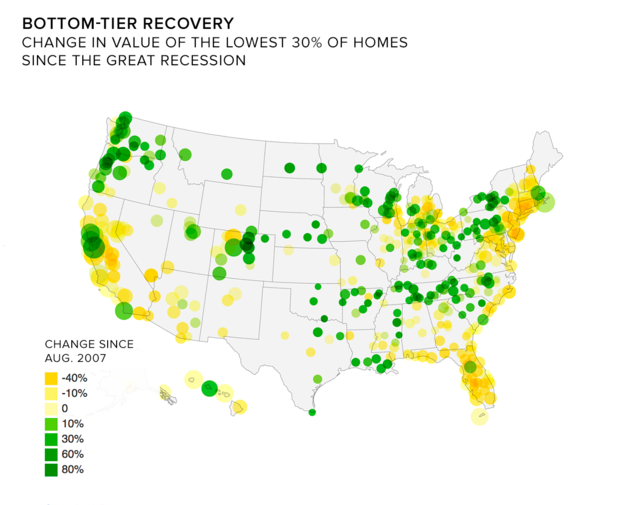

New data released by Zillow, the real estate listings company, shows that lower-priced homes are recovering value more slowly than those with higher prices. Even while many coastal cities are making headlines for increasingly unaffordable housing, more than half of the homes in the country -- 53 percent -- haven't regained what they were worth at the peak of the housing bubble in 2007.

Across the nation, 1 in 20 mortgaged homes is still worth less than the mortgage owed on it, according to CoreLogic.

This is evident in California, the poster child for the current housing affordability crisis. In the Bay Area, even the cheapest 30 percent of homes are up by as much as 20 percent over their 2007 value. But it's a different story inland. In Stockton, the cheapest third of homes are worth 17 percent less today than 10 years ago. In Modesto, they're down 14 percent and in Vallejo, they're 7 percent lower.

The Villages, Florida, is the only locality in the entire Sunshine State where the cheapest homes are now worth more than they were at the peak of the bubble. Homes in Western New York and Western Pennsylvania have recovered fully, while across all of New Jersey and the New York metro area, the lowest third of homes still aren't worth what they were 10 years ago.

Detroit's recovery has been the most uneven. The median home in the top tier is now worth $284,800 -- more than it was at the peak of the housing bubble. The median lowest-tier home is worth just $53,000, and only one in 10 of those homes has regained the value it lost in the crash.

"It's a signal, or a symptom, of how deep this recession went," said Svenja Gudell, Zillow's chief economist.

"The last time we saw a collapse on this scale was during the Great Depression, and it wasn't the same back then, because you didn't have as many homeowners," she said.

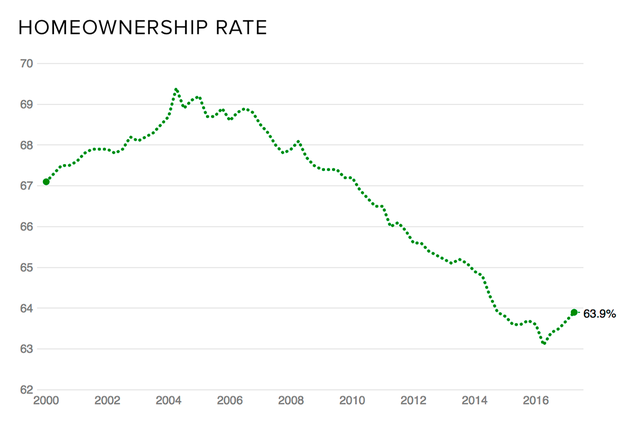

The implications of this unequal recovery are troubling, especially considering wages have been flat for nearly a decade. Stocks have been rising, but most Americans don't invest in the markets. For some 90 percent of them, "housing equity is the main store of wealth," the Federal Reserve Bank of New York found.

The recession wiped out this wealth for a good chunk of people, and many of them are finding it hard to get back to being homeowners. That's one reason the homeownership rate has kept falling even as the economy has expanded.

This is particularly evident for the lowest-income earners, who were more likely to buy homes with small down payments and thus see their equity wiped out in the crash. More and more people falling into this bracket now find themselves locked out of the market, Gudell explained.

People who lost a home to foreclosure after the bubble burst would have to wait seven years for the chance to buy again. In the meantime, much of their income would go to rent, constraining their ability to save for a down payment. By the time they could consider buying again -- 2015 or 2016 at the earliest -- many properties had become too expensive, thanks to rising values overall and builders focusing on the high end of the market.

Reversing this trend will take a good amount of effort: wage increases, particularly for the lowest earners; building a lot of new housing, also for the lowest earners; or a combination of the two. In the meantime, there's no easy fix.

"We will see more and more disparity between the people who are homeowners and the people who aren't homeowners," Gudell said, "or the people who bought during a lucky time and those who bought during a not-so-lucky-time."