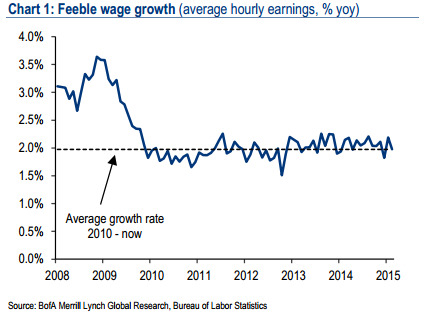

But where are the wage gains?

By one measure, the job market has fully healed. The unemployment rate fell to 5.5 percent in February, at the upper end of the Federal Reserve's estimate for a concept known as "full employment."

Put simply, this suggests that the job market has, for the first time since 2007, is back to normal. If the Fed's estimate is correct, any further declines in the unemployment rate will quickly result in higher wages and an upward push on measures on inflation.

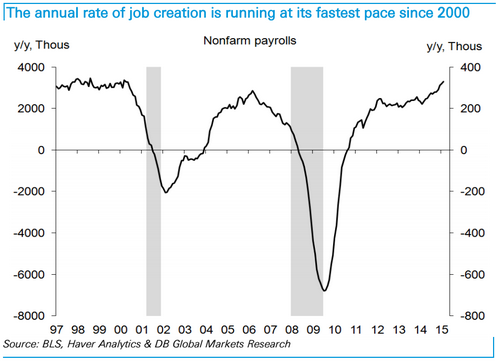

The February jobs report is impressive stuff. And it comes at the end of an impressive run of job gains rivaling the employment utopia enjoyed in the 1990s: Monthly payroll gains have totaled more than 200,000 per month since last March, a run of consistency that beats anything seen during the housing boom and matches a run of job gains between 1993 and 1995.

Altogether, we are now 11.5 million jobs above the February 2010 employment low.

But all's not perfect. We're still waiting for the appearance of meaningful wage gains -- something that has been sorely lacking in this economic recovery. Average hourly earnings are rising at a 2 percent annual rate, slightly below the 2.1 percent the economy averaged in 2013-2014.

Philippa Dunne of the Liscio Report notes that a lack of wage gains stands in stark contrast to the pace of job creation: Aggregate payrolls were up at a 5.4 percent annual rate in February, the fifth consecutive month above 5 percent.

The explanation is that, so far, much of the job gains have been in relatively low-quality jobs with an outsize contribution from bars and restaurants. Jobs here account for about 8 percent of total employment, but contributed 20 percent of February's job gains and 14 percent of the last year's.

And while total employment is now 2.8 million above the prerecession peak hit in December 2007, almost half of that gain was in bar and restaurant jobs. In Dunne's words, "this sector doesn't seem like the firmest ground for long-term prosperity."

Bank of America Merrill Lynch economist Michelle Meyer gives three theories for why wage gains remain tepid:

First is the belief that excess capacity still exists in the labor market. Although the unemployment rate has come down rapidly, "hidden slack" could be lurking as workers are underutilized.

Second is the risk of pent-up "wage deflation" from the recession. This is related to the phenomena of "sticky wages," where employers cannot easily cut wages during downturns. So, to compensate, they hold down wages in the recovery. If so, this would mean a larger lag between hitting full employment and the appearance of wage inflation.

And third, she also notes a shift in the quality of jobs, with a recent move to lower-paid jobs, which pushes down overall wage growth measures.

But the longer this torrid pace of job growth continues, the harder it will be for these three dynamics to keep holding down a jump in take-home pay.

Joseph LaVorgna at Deutsche Bank is looking to the latest Job Opening and Labor Turnover survey (JOLTs) for clues as to when wage inflation is set to lift. The pace of hiring has been a strong predictor of wage gains in the past and is currently projecting an increase in wage gains later this year.