Trump says the dollar is "too strong" -- good luck weakening it

American presidents have historically eschewed talking about the value of the dollar, traditionally leaving that to Treasury Department and Federal Reserve officials. As with so much else in his administration, President Donald Trump seems to have little use for tradition.

In a move that raised eyebrows this week, Mr. Trump openly stated that he wants the greenback to fall, telling the Wall Street Journal that “I think our dollar is getting too strong, and partially that’s my fault because people have confidence in me.” He also backed away from his previous promise to label China a currency manipulator that seeks to harm U.S. manufacturing.

His reason for wanting a weaker dollar: That makes U.S. goods less costly to foreign buyers, thus buoying America’s exporters. The president campaigned as a champion of U.S. exports, part of his appeal that endeared him to his blue-collar base, which overseas competition has damaged economically.

Yet while the dollar is off some 2 percent this year, the likelihood of a prolonged swoon for the buck is small.

Wall Street surely would applaud any effort to help exports via a lower dollar -- which would aid U.S. corporations, especially those that earn a lot of money overseas, because it would be worth more when changed into dollars and deposited into company tills. The stock market has surged thanks to Mr. Trump’s business-friendly talk (although stocks have hit a flat spell of late).

The trouble for Mr. Trump is that the long-term trend for the dollar is to rise against other currencies. As the world’s largest economic and military power, the U.S. is in the enviable position of almost everyone wanting to traffic in its currency -- that overwhelming demand has kept it aloft for much of the time since World War II. For that reason, Jonathan Loynes, chief economist at research firm Capital Economics, wrote in a note that Mr. Trump “will struggle to keep the dollar down.”

After news of his comments to the Journal got out, the dollar fell about 0.5 percent on Wednesday. Tellingly, however, it bounced back in Thursday trading, as if nothing had happened.

At his scrum with reporters on Thursday, White House press secretary Sean Spicer did not directly respond to a question regarding Mr. Trump openly calling for a weaker dollar and low interest rates, which serve to keep the currency down. That raised questions on whether the president’s musings on the subject were indeed White House policy.

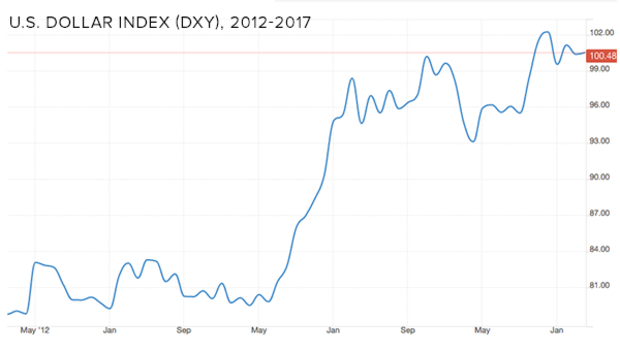

Over the past five years, the greenback has climbed 26 percent, compared to a basket of other denominations, as measured by the U.S. Dollar Index. The index shot up 4 percent from Election Day to year-end 2016, amid excitement that the Trump administration would spur U.S. economic growth through tax cuts and infrastructure spending.

Despite the foreign trade disadvantages of a strong dollar, it has long been the orthodox position of the federal government to push for one. As Ty J. Young, an Atlanta investment manager, put it: “”Most countries view a strengthening currency as a hallmark of a growing and prosperous economy.”

Nevertheless, the dollar has suffered setbacks through the years. Thus far in 2017, as fears arose that Mr. Trump’s plans will be delayed, half of those post-election gains melted away -- the index has dipped by 2.2 percent. Previously, the dollar tumbled during the Great Recession and its aftermath, because the U.S. was at the epicenter of the financial crisis.

Any action to significantly push down the dollar would take an extraordinary international effort, which would be difficult in light of Europe’s and Japan’s fragile economic recoveries. They need weaker currencies to prop up their exports. Another factor is China, which is trying to strengthen its yuan to, among other things, prevent Chinese assets from fleeing abroad in search of better returns.

Would Beijing be willing to make common cause with Washington on monetary exchange after it endured months of invective from Mr. Trump that it is manipulating its currency down to gain an advantage for its own exports?

The last time a concerted multinational campaign to pull back the soaring dollar occurred was in 1985, when it was another Asian nation, Japan, whose wares were getting a boost from a yen-dollar exchange rate in Tokyo’s favor. Amid threats in Congress to impose harsh trade restrictions, as American exports like grain and cars suffered, most of the world’s major economics at the time (that roster did not yet include China) joined forces to devalue the dollar. But they were in a solid economic position then.

The world is a lot different today. Here are three reasons the dollar should continue to ride high for the foreseeable future:

The dollar’s preeminence in the global order. In the late 1940s, as much of Europe and Asia lay in ruins, America became the world’s leading nation, and its currency became the indisputable core of the global economy. Some 80 percent of global trade transactions now are conducted in dollars. And the buck is used to value much of the world’s commodities, notably oil.

Nowadays, the U.S. has a lot more economic competition, with China’s economy growing at a 6 percent yearly clip, versus 2 percent for the U.S. Nonetheless, the dollar remains the preferred reserve currency, and proposals to replace it with other denominations -- perhaps including China’s yuan -- have gone nowhere. For one thing, unlike China, the United States has a relatively open society where contracts, the rule of law and intellectual property are generally held sacrosanct.

Interest rates are going up in the U.S. The higher interest a nation’s bonds generate, the more attractive its currency is. After the financial crisis, Washington led the rest of the planet in lowering rates to near zero. But the Federal Reserve has taken the lead in raising short-term rates, with three hikes in the past 16 months and two more expected this year. The goal is to “normalize” them to somewhere in the mid-single digits, much as they were pre-2008.

The Fed’s action on short-term rates has an influence on long-term ones eventually. And if Mr. Trump gets his way and receives congressional approval to spend $1 trillion to restore the nation’s aging infrastructure -- roads, tunnels, dams, etc. -- a lot more federal debt will be issued. That increased supply should lower American bond prices, and therefore jack up yields (they move in opposite directions).

True, one obstacle to meeting that goal is that the U.S. is the ultimate refuge. Whenever turmoil hits, whether a war or a financial problem like Europe’s debt crisis, investors flock to American bonds, with the 10-year Treasury note the most popular. That serves to keep long rates down because their prices are bid up.

Meanwhile, there is one tool Mr. Trump could use to make the Fed back off its rate-raising campaign: filling vacancies at the central bank with people who want lower rates. He has spoken of not re-appointing Janet Yellen as Fed chair when her term runs out next year. She is leading the rate-hiking charge (although in his remarks to the Journal, the president did seem to back off his previous pledge not to keep her on).

Rates are lower elsewhere. The American economic recovery is further along than those of other major economies (other than China’s). That has made for better yields in the U.S. as foreign investors search for the sweeter returns. “U.S. yields are significantly higher than those of the USD’s main peers,” said Scotiabank in a research note, referring to the U.S. dollar.

Europe is still dealing with the economic woes of its southern periphery, mainly Italy and Greece, and also is fretting about elections in France and Germany, where far-right parties may win -- and pull out of the European Union. Britain faces a bumpy ride extricating itself from the European Union. And Japan’s woebegone economy is still plodding along. All their central banks are keeping rates down.

That all leads to foreigners scrambling for U.S. bonds and other fixed-income investments, which they must buy in dollars. So higher demand for the buck increases its worth.

In other words, if Mr. Trump is serious about a lower dollar, he has his work cut out for him.