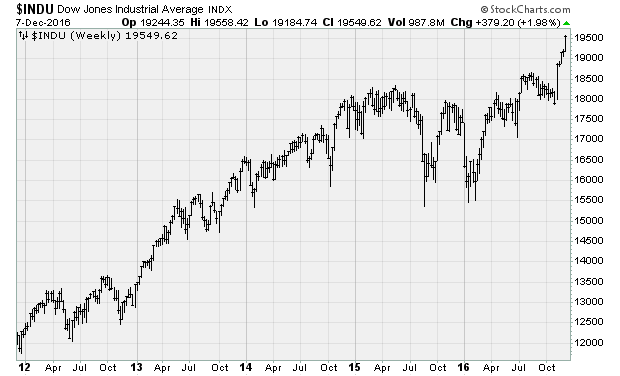

The Dow is surging toward 20,000 on a thin crest

The post-election rally reached a new level of intensity on Wednesday in what could only be characterized as a buying panic. The Dow Jones industrials index pushed to another record high and is now less than 500 points from the 20,000 threshold, up more than 8 percent from its pre-election low. Impressive stuff, considering the next Federal Reserve interest rate hike is likely just a week away.

No specific catalyst sparked the move, which featured some countertrend activity in areas like bonds, volatility and commodities. Excitement continues to build on Wall Street over President-elect Donald Trump’s deregulation and fiscal stimulus plans.

Yet as stocks rocket higher, the risks to investors joining the party late -- of which there are many given the narrowness of the advance -- continue to grow.

For one, stocks have simply come too far too fast (chart above). Currently, the Dow is 4.1 percent above its 50-day moving average -- an intermediate-term trend measure. That’s rare: Since 1985, on any given day the Dow is typically just 0.9 percent above its 50-day average. In terms of percentage rank, the Dow’s current perch is higher than 84 percent of all days.

Said another way, the stock market has been more extended to the upside just 16 percent of the time.

The narrowness of the advance is also worrisome. Currently, only 66 percent of the S&P 500 stocks are in uptrends, despite the rise to record highs. Compare this to levels above 75 percent in August and September and near-80 percent readings in March and April.

Alternative measures of market breadth tell the same story: Less than 68 percent of the stocks on the New York Stock Exchange are above their 50-day moving average vs. 80 percent-plus in July and 90 percent-plus in April.

It’s worth noting that seasonality suggests the Trump Rally could hit headwinds in just a couple of weeks. David Rosenberg of Gluskin Sheff pointed out that practically every new president since Harry Truman has enjoyed a “Honeymoon Rally” in the weeks following their election. The median advance the month after an election is nearly 1 percent vs. the 6.6 percent rally for Mr. Trump. Ronald Regan enjoyed a 6 percent rally his first month in office.

But less than four weeks in Reagan’s term, the market peaked and the next two years were marred by an economic downtrend and a 25 percent decline in stock prices as a combination of higher interest rates, Fed policy tightening and a stronger dollar took its toll.

All three dynamics are in play right now.

And finally, the recent weakness in bonds -- and the associated rise in interest rates -- could pose a serious problem for stocks very soon.

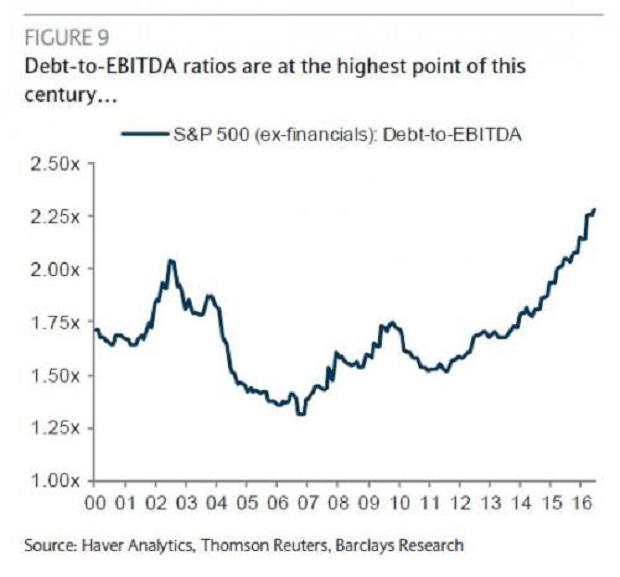

Higher interest rates will be a drag on equity valuations as discount rates rise and investors start wondering about the negative impact on earnings from rising interest costs for debt-burdened corporate balance sheets (chart above). The U.S. 10-year Treasury traded near a 2.5 percent yield last week -- a 17-month high. Analysts at Societe Generale put the “red zone,” so to speak, at 2.6 percent. Goldman Sachs puts it at 2.75 percent. Above these levels, stocks valuations could suffer.

Much of this will come into focus on Dec. 14, when the Federal Reserve will likely raise interest rates for the second time this cycle, just days before Wall Street’s Christmas holiday break.