Sure looks like a bubble forming on Wall Street

Investors are valuing stocks these days at levels -- measured by the S&P 500's price-earnings ratio -- that were higher only during the 1929 and 2000 market bubbles. But is today's market also in a bubble?

It's hard to say when you're in the middle of one, given that the primary motivators of this bull market -- cheap credit and strong corporate earnings -- have slowed but aren't in full reverse just yet.

Yet growing evidence indicates bubble-like conditions are increasing amid red-hot sentiment, investor complacency and historic low volatility. In Wall Street vernacular, one could say these are signs of "froth."

Increasingly, brokerages are sounding the alarm. Bank of America Merrill Lynch chief investment strategist Michael Hartnett outlined a few reasons for concern in a recent note to clients:

- Relative to the size of the economy, the S&P 500's market capitalization is quickly approaching an all-time high.

- So far, global issuance of high-yield debt (also known as junk bonds) is tracking nearly $500 billion annualized, a record high.

- Argentina, a country that has spent one-third of the last 200 years in debt default -- and has defaulted three times in the past 23 years -- just announced a 100-year bond offering.

- The market cap of Facebook (FB) now exceeds the size of India's stock market, a country of 1.28 billion souls vs. a company with 18,000 employees.

- Inflows to tech-focused funds are rising in 2017 at their fastest annualized rate in 15 years (since the dot-com bubble burst).

- Investors are aggressively moving into the eurozone, a classic late-cycle signal (given Europe's ongoing structural problems).

- And market volatility is plumbing historic depths. U.S. Treasury market volatility is nearly at all-time bottom, and S&P 500 volatility is at 20-year lows.

Fundamentally, this market has three supports: Earnings growth, economic growth and global credit flows/central bank easing. Of these three, two are already rolling over. Any other justification comes down to emotion, multiple expansion -- and prayer.

According to the Citigroup Economic Surprise Index, U.S. economic data is missing estimates to a degree not seen since 2011 as the post-election "Trump-flation" hopes are dashed amid dimmed prospects for actual health care and tax reform. From a high of nearly 4.5 percent, the Atlanta Federal Reserve Bank's GDPNow real-time estimate of second-quarter growth has fallen to just 2.9 percent. The stock market is resolutely ignoring the rollover in economic data.

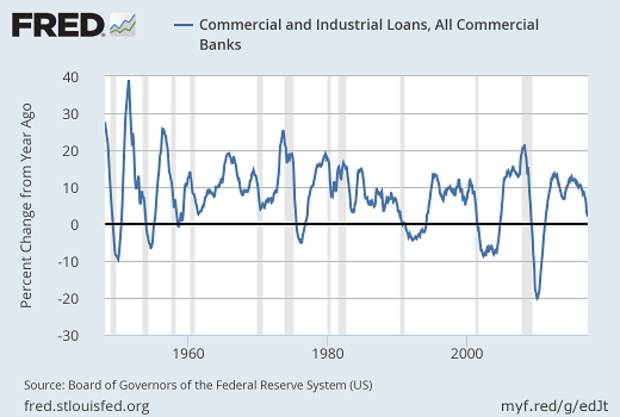

Credit flows are slowing as well as the Federal Reserve aggressively hikes interest rates and new loan activity (chart above) stalls in recession-like fashion. The Fed has unleashed three quarter-point rate hikes since Election Day, has penciled in another before the end of the year and is expected to start reducing its $4.4 trillion balance sheet in September.

New York Fed President Bill Dudley raised eyebrows over the weekend when he noted that despite the Fed starting its policy tightening cycle in December 2015, financial conditions have actually gotten easier as stock prices have rallied, bond spreads narrowed and long-term yields declined. In his view, this should encourage the Fed to tighten policy even more aggressively.

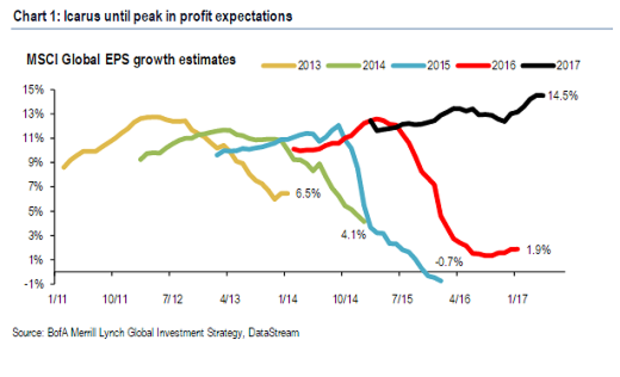

The final leg of fundamental support the bulls can point to with a clear conscience -- preventing any admittance that stock prices may have come too far too fast -- is that 2017 earnings growth estimates have avoided the midyear collapse seen in each of the last four years. Currently, global earnings-per-share growth estimates stand at 14.5 percent (chart above).

As long as this metric remains buoyant, Bank of America believes stocks will continue to grind higher in what its analysts have dubbed the "Icarus trade" -- before eventually falling back to earth.

Second-quarter earnings reporting season will start over the next few weeks, presenting a major threat to full-year earnings estimates. Why? Because of the weight on energy companies and major banks from the recent energy price weakness and, especially for banks, the drop in long-term Treasury yields, which is a drag on net interest margins.

According to FactSet, reality is setting in: Analysts' S&P 500 earnings growth estimates have already declined to 6.6 percent from 8.7 percent on March 31, led by downward revisions in energy.

The next startling sound you hear could be a bubble bursting.