Why the slump in corporate profits looks set to continue

Investors have had plenty to think about in recent weeks. Brexit. Italian bank bailouts. Payroll gains. Shifting odds of a Federal Reserve interest rate hike this year. Surges in "safe haven" assets like bonds and precious metals.

But fundamentals are about to make a return. The second-quarter earnings reporting season starts Monday when Alcoa (AA) reports, followed by big bank earnings from JPMorgan (JPM) on Thursday and Wells Fargo (WFC) and Citigroup (C) on Friday.

As things stand, the news won't be good. According to FactSet data, analysts expect S&P 500 earnings for the quarter to decline 5.6 percent from the year-ago period, which would mark the fifth consecutive quarter of falling profitability. Evidence also suggests the earnings recession is set to continue through the end of the year.

Expectations have been waning amid headwinds including a strong U.S. dollar, energy prices that remain well off of their 2014 highs, falling labor productivity, and higher unit labor costs. Back in March, analysts were looking for S&P 500 earnings to decline 2.8 percent. Nine sector groups have since seen their earnings estimates cut, with information technology hit the worst.

Guidance from the companies themselves has also been negative, as is typical, since lowered expectations are easier to beat: So far, 81 S&P 500 companies have issued negative earnings per share guidance, versus 32 that have issued positive guidance.

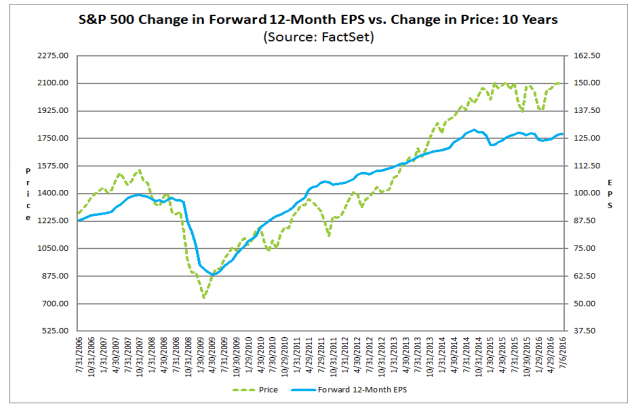

The combination of stock prices within inches of record highs and the ongoing slide in earnings continues to put upward pressure on market valuations. The S&P 500's 12-month forward price-to-earnings ratio is 16.6, above the five-year average of 14.6 and the 10-year average of 14.3. By this measure, stocks are downright expensive given faltering profitability.

How many positive surprises should investors expect as the financial results roll in?

FactSet looked back at where actual earnings came in compared with lowered estimates in recent quarters. They found that over the past four years, actual earnings reported by S&P 500 companies have beat estimates by an average of 4 percent. During this time, more than two-thirds of S&P 500 companies have beat their estimates.

As a result, from the end of the quarter to the end of the associated earnings reporting season, the overall S&P 500 earnings growth rate has increased by an average of 2.7 percentage points. Applying this number to the current second-quarter estimates suggests the actual end-of-reporting earnings decline for the period will be just below 3 percent.

Digging in, there are a few bright spots. Four sectors are expected to post positive earnings growth, led by telecoms and AT&T (T) thanks to its recent purchase of DirecTV. Not surprisingly, energy companies are the largest drag on overall growth, with a 77 percent year-over-year decline in earnings expected.

Over the horizon, hope springs eternal as both earnings and revenue growth is expected to return in the second half of the year. For earnings, growth rates of 0.7 percent and 7.2 percent are expected for Q3 and Q4. For revenues, growth rates of 2.2 percent and 5.1 percent are expected. Forecasters predict that materials, utilities and financial companies will lead this second-half bounce back.

Of course, analysts tend to be an optimistic bunch -- industry data show they tend to overestimate earnings growth in the second half of the year by nearly five percentage points. If this is applied to the 4.2 percent growth expected for the back half 2016, earnings are likely to drop 0.5 percent.

In other words, as things stand now the earnings drag may well continue.