The economic slowdown deserves a second look

The data continue to disappoint.

The Citigroup Economic Surprise Index, which rises and falls based on how reality is living up to analyst expectations, has collapsed to levels not seen since 2011. The Atlanta Fed's GDPNow real-time tracking estimate of first-quarter GDP growth has dropped to just 0.2 percent from nearly 2.5 percent back in February.

The optimists, including a Federal Reserve eager to start raising interest rates, are quick to dismiss this softness as caused by transient factors such as severe winter weather, especially on the East Coast. Seasonal factors are in play as well, with UBS recently highlighting that first-quarter GDP growth has been consistently weak since at least 1988 -- suggesting government statisticians need to rejigger the data.

But there is also a nagging sense, especially in light of soft data globally, that something is amiss.

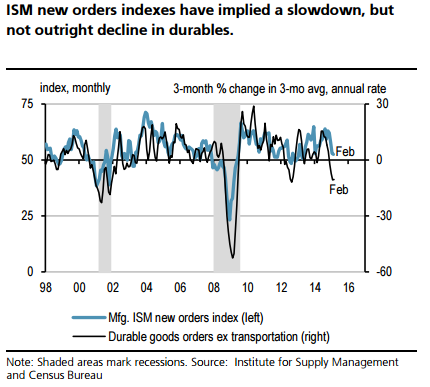

The working thesis is that the stronger dollar and lower oil prices have formed a toxic brew pulling down business investment, a dynamic that's weighing on various measures of activity from producer price inflation to factory orders. Maury Harris at UBS noted that core durable goods orders have been dropping since September, making this hard to simply dismiss as being weather-related.

The chart above shows that the drop in new orders should have an ongoing effect on factory activity in the U.S. in the months to come. The fall-off has been severe and at levels associated with the start of the last two recessions.

At this point, it seems that the dollar's rise is the primary instigator: A Duke Fuqua School of Business/CFO Magazine survey asked executives what was bothering them. A quarter of firms with at least 25 percent of their sales from abroad indicated currency-related drops in capital expenditures.

The good news is that the dollar's rise has been tempered somewhat in the wake of the Federal Reserve March policy statement, in which it halved its expectations for the number of interest rate hikes this year to just two. That should, hopefully, limit the impact on business investment through the rest of the year.

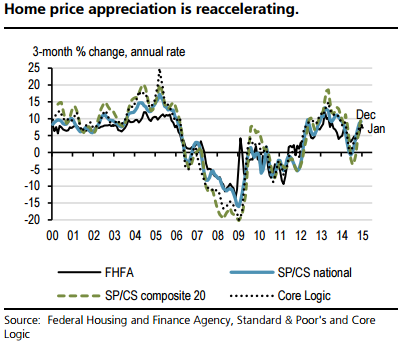

Housing is also showing signs of strength, with home price gains reaccelerating and a rise in rents pressuring Millennials into becoming homeowners. The rate of new household formation is far outpacing new home construction. Amid tight existing-home inventories, price gains should accelerate heading into the peak summertime home buying season.

And finally, Friday's disappointing consumer sentiment report -- even though it's the second drop in as many months -- shouldn't be the start of a spending retreat by households. Deutsche Bank economists are looking for shoppers to bounce back as a rapidly tightening labor market, the specter of long-awaited wage gains and improved balance sheets fuels confidence.

They're looking for a slight pullback in the savings rate to further pad expenditures heading into the summer. Moreover, lending standards continue to loosen, and mortgage growth is turning positive in early indications that credit is beginning to expand again after a long hibernation.

At this point, while countries like China and Japan are contending with deep, structural problems, the U.S. -- after years of monetary policy triage -- appears to be on the cusp of an economic tailwind focused on the middle class and working families. That would be a refreshing change of pace from what we've seen in this recovery so far: Gains accruing to the corporate sector via ballooning profitability and record earnings, and to the wealthy via gains in financial assets.