How to find "hidden" 401(k) fees

(MoneyWatch) Last week my CBS colleague Jill Schlesinger explained in a video how to save money by looking at the 401(k) fees assessed against the funds in your plan. I have a constructive and friendly disagreement, however, with her use of the word "hidden." 401(k) fees are no longer hidden -- plan sponsors are now required to provide statements to plan participants that disclose these fees.

"Ignored" might be a better word than "hidden," but then the title of Jill's article and video clip wouldn't be very newsworthy. The trouble is, most people don't take the time to examine the fees in their 401(k) plan, or they don't know how or where to look. For example, at a retirement planning seminar I gave last week, only about seven out of 60 attending participants said they'd even bothered to look at their 401(k) fee disclosure statement.

Let's take a look at a few fee disclosure statements so you at least know what to look for so you can compare your funds to other funds. The relevant number is the expense ratio -- annual fees as a percentage of assets. The numbers typically range from percentages of less than 1 percent to 2 percent or higher. As you'll see, these fee disclosures can go by a variety of names.

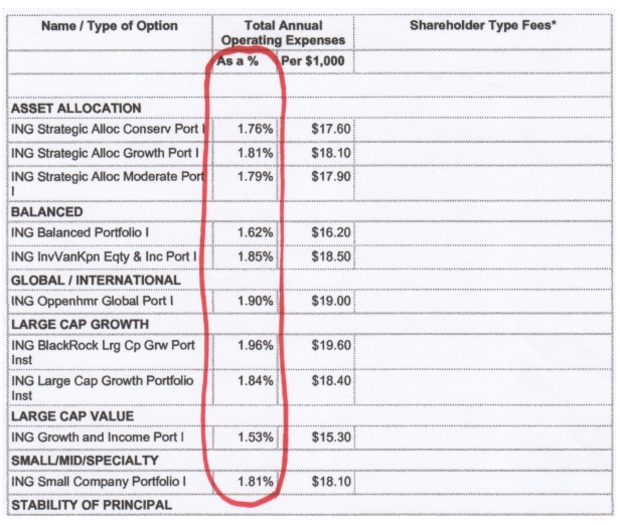

A particularly bad 401(k) fee statementHere's a fee disclosure from a 401(k) plan with high fees -- the annual charges are well above 1.5 percent of the value of assets. I've circled the column that discloses the fees -- this heading reads "Total Operating Expenses As a %."

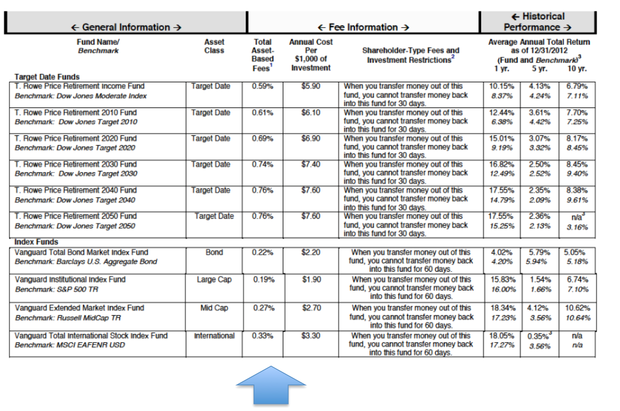

A better 401(k) fee statement

Here's a fee disclosure statement with better fees -- all annual charges are well below 1 percent. The blue arrow shows the column with the fees. In this case, the heading is titled "Total Asset-Based Fees."

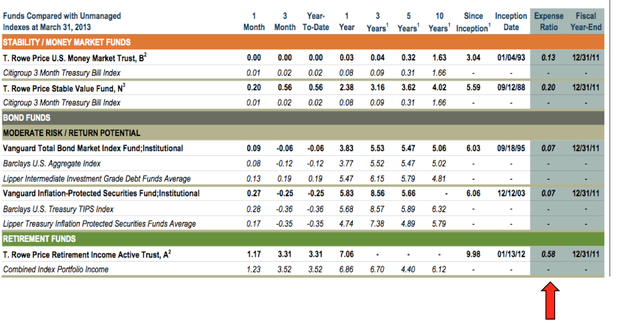

A very good 401(k) fee statement

Here's another fee disclosure statement with very low fee levels; note that two funds have charges of just 0.07 percent per year, and two more funds have expenses of 0.20 percent or lower. Most likely, you couldn't get this level of fees on a retail basis on your own, which illustrates the advantages of saving through a 401(k) plan where the employer has gone to the trouble of shopping for the best possible fees. The red arrow shows the column with the fees. In this case, it's simply labeled "Expense Ratio."

How much money is at stake when it comes to 401(k) fees? Suppose you have an account balance of $100,000. With an annual expense ratio of 1.5 percent, you'll spend $1,500 each year on fees. With an annual expense ratio of 0.5 percent, you'll spend only $500 -- $1,000 less. If your 401(k) plan has fees well above 1 percent, I'd suggest you constructively discuss this topic with your boss and show him or her this column. Chances are, your boss is in the same 401(k) plan and will save money as well by finding a plan that charges lower fees.

- Don't let high 401(k) fees bleed you dry

- CNBC plunges as indexing soars

- The lies active managers tell

- How to avoid hidden 401(k) fees

You stand to lose even more money if your high-fee fund is actively managed instead of passively managed; index funds typically outperform their actively managed brethren over the long run, as repeatedly pointed out by my CBS MoneyWatch colleagues Allan Roth and Larry Swedroe.

One last comment: Don't use video clips you've seen or articles you've read that mention high 401(k) fees as an excuse not to contribute to your 401(k) plan. Even with high fees, it pays to contribute if your savings are matched by your employer because the match will more than pay for the high fees. And you might find that your employer has negotiated funds that are better than you could find on your own -- that's a deal you shouldn't pass up!