How older workers and retirees can stop worrying about falling stocks

If you're an older worker or retiree, you may understandably be worried about the stock market's recent tumbles -- particularly with concerns that you won't have time to make up for your losses.

Here are two tips to help ease your fears:

- Keep a historical perspective on stock market returns

- Adopt strategies to protect against stock market crashes

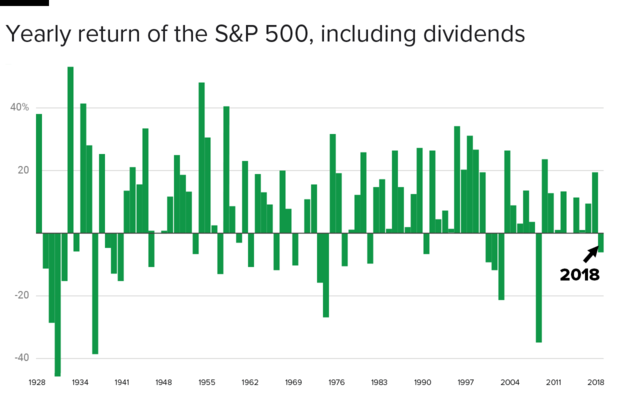

The historical perspective

A look at annual returns (including dividends) for the S&P 500 since 1928 shows that 2018 was the first annual loss after a nine-year winning streak, which tied the record for winning streaks. If you were invested in stocks during this period, you're still way ahead -- even considering 2018 losses -- than if you had been invested in bonds or other "safe" investments.

The chart also illustrates a significant "double-double" for the S&P 500:

- It has had well over twice as many up years as down years -- 68 up versus 25 down.

- The average gain during the up years was almost twice as much as the average loss in the down years. So when the market went up, investors typically made more money than they lost when the market went down.

If you're in your 50s, 60s, or even your 70s, you can expect to live for one, two or even three more decades. This should give you enough time to ride out most stock market declines.

Strategies to protect yourself from market crashes

History shows you'll most likely experience a few more stock market crashes during your retirement years. The trouble is, nobody -- not even the "experts" -- can reliably predict when they'll happen. We also know that pulling out of equities during a crash is one of the worst moves you can make. Doing so locks in your losses and misses out on good returns when stock prices recovers.

That's why you'll want to build your retirement income portfolio in a way that gives you confidence that you can ride out future crashes, whenever they might occur.

To do that, you'll want sources of retirement income that can cover your basic living expenses and not drop when the market crashes. Such sources include Social Security, a pension if you're lucky enough to have one and annuities you can purchase from an insurance company.

Start by optimizing your Social Security income, which is the "almost perfect" retirement income generator. For many middle-income workers, optimized Social Security benefits might be the only guaranteed, lifetime retirement income they need to cover basic living expenses.

If you've earned a significant benefit under a traditional pension plan, make smart choices to optimize that valuable benefit. And be sure to resist the urge to take a lump sum instead of the guaranteed monthly pension, if you're offered that choice. A lump sum isn't usually the best choice.

Retirees who want more guaranteed retirement income to cover their basic living expenses can consider "bond ladders," low-cost payout annuities or monthly payments from reverse mortgages.

Once you've developed enough sources of guaranteed income to cover your basic living expenses, you should feel confident to invest your remaining savings significantly in stocks to give you the potential for growth. These savings can be invested in low-cost target-date funds, balanced funds or stock index funds. Use this money to generate a retirement paycheck that covers your discretionary living expenses, such as hobbies, travel and gifts, or for spoiling your grandchildren.

Adopting these two tips should encourage you to remain invested when the market drops and wait for it to bounce back. If you have your basic living expenses covered, you should have the patience to ride out any crashes.