Retirement savers should ignore market forecasts

If you're keeping up with the stock market at all, you've most likely read various 2018 forecasts. Some analysts boldly predict new highs, while others worry about the age of the current rally -- and any number of other possible problems -- and predict a decline. Who'll be correct?

Market forecasters have had a lousy track record over the years, according to various analyses and studies. Fortunately, if you're investing for retirement, you can adopt strategies that let you ignore such "expert" forecasts.

Investing insights from history

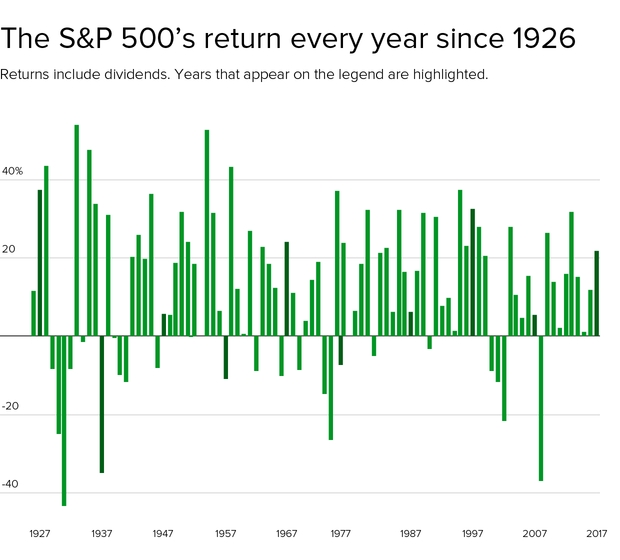

During 2017, the total return on the S&P 500, including dividends, was 21.8 percent. This was the ninth straight calendar year that the market posted positive returns. The current streak ties the longest one previously, which was from the beginning of 1991 to the end of 1999.

The chart below shows those total returns since 1926, which helps you see the stock market's various winning streaks. You can also glean some important insights on retirement investing from this chart.

The chart illustrates a significant "double-double" for the stock market. First, Wall Street has had well over twice as many up years as down years -- 68 of the former compared to 24 of the latter. Second, the average return for up years was almost twice as much as the average return in the down years. This means when the market went up, investors typically made more money than they lost when the market went down.

If you're still working, are investing for retirement and don't plan to retire within the next five years, you have a very long investing horizon. After all, you'll be investing your retirement savings up to and throughout your retirement years. That chart should give you the confidence to ride out the downturns and wait until the market rises again.

But what if you're closer than five years to retiring or are already retired?

Investing insights for older workers

In that case, you'd do well to start shifting your thinking from accumulating savings to building a diversified portfolio of retirement paychecks. You'll want some sources of retirement income that won't drop when the market crashes so you can cover your basic living expenses.

Most likely, you'll have a few more stock market crashes during your retirement years. The trouble is, nobody -- certainly not the "experts" -- can reliably predict when they'll happen. As a result, you'll want to build your retirement income portfolio to withstand future downturns, whenever they might occur.

Start by optimizing your Social Security income, which is the "almost perfect" retirement income generator. For many middle-income workers, optimized Social Security benefits might be the only guaranteed, lifetime retirement income they need.

Optimizing Social Security benefits usually involves delaying benefits as long as possible but no later than age 70. If you retire before you start Social Security benefits, you might want to build a "retirement transition bucket" that will substitute for the Social Security income that you're delaying. You'll want to invest this bucket in funds that don't drop when the stock market crashes, such as short-term bond funds, money market funds or "stable value" funds in 401(k) plans.

Workers who want more guaranteed retirement income can consider bond ladders, guaranteed annuities or tenure monthly payments from reverse mortgages.

The next step is to supplement your guaranteed income sources with retirement income generators invested significantly in stocks to give you the potential for growth. These savings can be invested in low-cost target-date funds, balanced funds or stock index funds. Use this money to generate a retirement paycheck that covers your discretionary living expenses, such as hobbies, travel, gifts and spoiling your grandchildren.

The S&P total returns chart should encourage you to remain invested when the market drops and wait for it to bounce back. If you have your basic living expenses covered, you'll likely have the patience to ride out any crashes.

Plenty of evidence also showing that a low-cost index fund will beat most actively managed funds, so you don't need to fret about finding the best mutual fund. The return on the S&P 500 or other broad market index should be good enough for your retirement stock investments -- you don't need to take additional risks to try beating the market.

With a strategy that balances safer sources of income with some money in the stock market, you won't need to worry about which forecaster is correct. If you spend the time necessary to design a thoughtful retirement investing strategy, you can leave your money worries behind and enjoy your life.