Higher interest rates shouldn't halt the housing market

If you’re saving up to buy a new home, you’ll need a lot more of it in 2017. On Wednesday, the Federal Reserve announced a 25-basis-point hike in its benchmark federal funds rate and indicated that it expects three further increases in the coming year.

The decision was long-delayed, coming a full year after the Fed’s first quarter-point raise in a decade last December. Among the reason’s for the Fed’s hesitance to pull the trigger were fears that higher interest rates would throw the economy -- and especially the fragile housing market -- into a tailspin. But now that the hike is made, it’s likely to have little or no impact on those in the business of buying and selling homes.

“We’ve been prepared for this for some time,” said President Steve Udelson of Owners.com, an online brokerage that helps people buy and sell homes themselves. “Gradual rate increases are unlikely to be a huge game changer.”

His users weren’t the only ones girding for the increase. Home refinancing originations rose 16 percent in the third quarter year-over-year -- a sign that many people felt a rate hike was coming and prepared for it ahead of time.

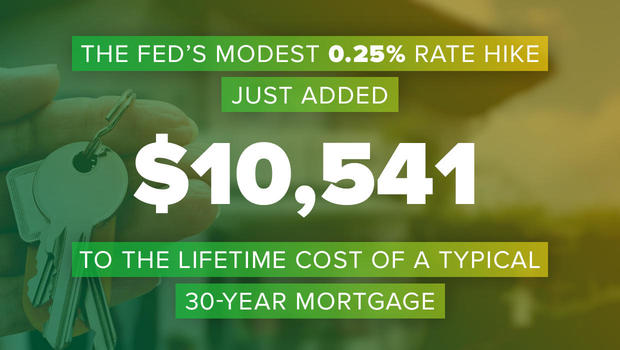

A rate increase will undeniably cost prospective homebuyers more when they seek a mortgage. Interest rates for a 30-year fixed-rate loan are currently hovering just above 3.5 percent on some websites. And while the Fed doesn’t directly control consumer interest rates, the quarter-point hike and the directional tone of “continued gradual increases” in the Fed’s policy statement will definitely move mortgage rates higher.

The upward movement so far -- some in anticipation of what the Fed would do -- has increased mortgage payments by 7 percent, or about $750 in additional interest, on a median-priced home each year, according to Chief Economist Jonathan Smoke of the online website realtor.com.

“We anticipate that rates may be 4.5 percent by the end of 2017,” said Lawrence Yun, chief economist for the National Association of Realtors (NAR) “and that home prices will also march upward by 4 percent.”

But Yun said even at that level, the market is “still favorable” to homebuyers. He expects 2017 will be a “decent year,” with home sales about equal to 2016.

It will certainly be more favorable to home sellers, who will see increased prices. That could prompt more homeowners to put their properties up for sale in what has become an increasingly undersupplied market.

It’s also more favorable to banks and other lenders. “They may open up the lending box and relax their standards, which were excessively tight,” predicted the NAR’s Yun. “And quite a number of new ones could enter the market.”

Even though rates and housing prices will certainly go up, household income is rising as well, allowing more people the opportunity to buy. Currently at 4.6 percent, unemployment is at its lowest rate in almost 10 years, and consumer confidence is up, “both positives for the real estate industry,” said Owners.com’s Udelson.

The huge jump in homeowner’s equity, which has more than doubled from a low of $6 trillion at the start of 2009 to $13 trillion in the third quarter of 2016, may seem like a hurdle for new homebuyers, but it’s also a positive for those who want to sell their current house and move up to a more expensive property.

Realtors concur that homes are worth more on resale, and they now feel more comfortable that values won’t plunge again like they did in the 2008 recession. This could free up more starter homes for first-time buyers.

The NAR’s profile of homebuyers and sellers shows a growing desire for people to own a home -- 67 percent in 2016 compared to 53 percent in 2014. And realtors said many of them are millennials, nearly 25 percent of whom still live with their parents but may be earning enough to buy a house or condo.

“In September, first-time homebuyers reached a 34 percent share,” said Udelson, “the highest rate in over four years.” They now form a third of the total pool of buyers.

One constraint on the housing market -- homes that were “underwater” -- is definitely easing. An underwater homeowner is faced with paying a mortgage that’s worth more than the home’s value. It’s not only discouraging but can also lead owners into foreclosure or to simply abandon the house.

Thanks to the rise in home equity, which increased $726 billion in the third quarter compared with a year ago, and to the wave of homeowners who’ve been able to refinance at the current low rates, the number of underwater homes has fallen nearly 25 percent this October compared to the same time in 2015, according to CoreLogic, a property information and analytics firm. And CoreLogic had even better news: The national foreclosure inventory fell nearly a third since last October.

Home prices, which began rising in 2012, have fully recovered from the depths of the housing bust. U.S. households’ ownership equity reached 57 percent of the value of their homes, the highest since 2006, according to Fed figures.

This news might encourage anyone thinking about buying because rents have skyrocketed in recent years, outpacing income in 57 percent of all markets, according to RealtyTrac. Buying is now more affordable than renting in most places.

But others say, not so fast.

First off, a rush into the housing market could create huge inflation in a market where listings are few and people aren’t always ready to sell when you want them to. Realtor.com’s Smoke said there was “record low inventory” in November and “an intensifying supply shortage” with only 363,000 new listings in the past month.

“Buyers are starving due to the inventory of homes for sale,” he said.

And the other big question mark is that President-elect Donald Trump said he favors deregulation.

“Regulatory changes could make credit standards less stringent and more available to first-time homebuyers,” predicted Udelson. “Alternative mortgage options could resurface, offering a lifeline to potential buyers who don’t qualify for conventional financing.” Of course, the downside of that is a potential rerun of the housing bust if too many unqualified borrowers wind up with mortgages again.

Another big but, said Yun, is that Trump’s pick for Treasury Secretary, Steve Mnuchin, wants to sell Fannie Mae and Freddie Mac. These two federal agencies back 95 percent of all mortgages and are two of the largest financial institutions in the world, responsible for a combined $5 trillion in mortgage assets.

Warned Yun: “That’s likely to make mortgage rates even more expensive.”