How GOP tax plans are playing on Wall Street

Investors continue to respond rather tepidly to the outcome of the Senate's passing its version of the GOP's tax reform proposal. Why? It's partly because they're "rotating" out of low-tax sectors like technology (the group with recent upward price momentum) and into high-tax areas like telecoms, consumer staples and retailers (all of which have been laggards lately).

And some of it is because of an embarrassing realization that the Senate Republicans sort of messed up -- a consequence no doubt of hurriedly passing a near-500-page bill in the middle of the night -- and left in the current 20 percent corporate "alternative minimum tax" rate while cutting the regular statutory rate from 35 percent to 20 percent. Keeping the corporate AMT could mean businesses would no longer be able to claim the popular -- especially for tech companies -- research and development credit.

Therefore, many would actually pay a higher tax rate than the GOP intended, diminishing the benefit of the reforms in the first place. The House version of the bill dumps the AMT, so the hiccup will likely be removed in the joint conference committee before a final bill passes both chambers.

The sector-rotation dynamic is likely to continue through year-end as Congress works to get a final copy of its tax legislation to President Donald Trump's desk in 2017. UBS analyst Keith Parker, writing back on Nov. 30 after the House passed its tax bill but before the Senate approved its version, estimated just a 20 percent to 40 percent probability the tax cuts had been priced into markets. Figure that number is around 50 percent now, leaving room for investors to shift their bets even more.

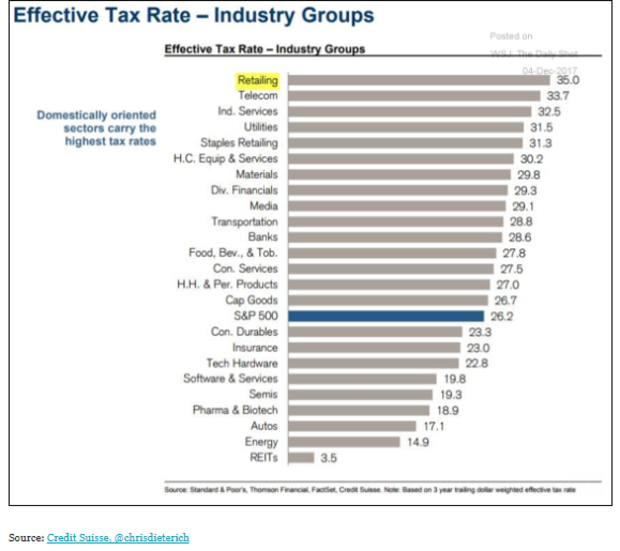

Currently, even though the statutory US corporate tax rate stands at 35 percent, companies overall are paying just 27 percent on average, according to Credit Suisse (chart above).

So companies that are above that average are poised to benefit the most when considering cash tax impact as a percentage of market capitalization. They include beaten-down names like Macy's (M), Kohl's (KSS) and Kroger (KR), according to UBS.

Overall, Parker sees 9.5 percent earnings per share upside for companies in the S&P 500 stock index from the legislation. Individual high-tax sectors would likely benefit more, with retail particularly ready for a possible rebound from post-Amazon (AMZN) levels.

Those stocks would benefit from the fact that institutional investors like mutual funds and hedge funds are underweight in these areas -- and in some cases outright net short (betting those stock prices will fall). That would result in forced buying and short covering.

Separately, Wall Street is feeling some nervousness about rising odds of a government shutdown later this month, with the government needing at least a short-term funding bill passed by Dec. 8. So all of this is far from a done deal.