Fed turns hawkish as stimulus ends

It's taken more than six years to get here, but it's finally happened: The Federal Reserve is ending its controversial policy of mainlining money into the U.S. economy in hopes of stimulating growth.

But Fed officials went even further in announcing the end of its bond-purchase program, sounding a surprisingly optimistic note about the health of the economy just weeks after stocks suffered the worst selloff in months (a pullback that, in turn, led St. Louis Federal Reserve Bank President James Bullard to say that the bond buying should continue). Policymakers also acknowledged, but did not emphasize, the strengthening job market and a recent cooling of inflation pressure.

All of this gives the impression that the Fed is aggressively pulling the plug on a program that has bolstered the stock market and the economy since 2008. Markets reacted accordingly, with the U.S. dollar rebounding strongly as stocks slipped modestly, pushing the Dow Jones industrial average back below the 17,000 level.

The major question now: Is the Fed's confidence in the economy justified?

The Federal Open Market Committee -- which sets interest rate policy -- highlighted that "there has been a substantial improvement in the outlook for the labor market since the inception of its current asset purchase program" and that "a range of labor market indicators suggests that underutilization of labor resources is gradually diminishing."

The Fed should hope, since it's bond buying has swelled the monetary base from $800 billion before the recession to more than $4 trillion now.

An important test of the economy comes Thursday when the government releases its initial estimate of for third-quarter gross domestic product. Aside from the weather-related slip in the first quarter, growth has been strong, posting 4.6 percent annualized growth between April and June -- the fastest rate of expansion since the end of 2011 -- and has averaged 2.6 percent over the last four quarters. Wall Street is looking for 3 percent annualized growth for the July-to-September period.

Friday will bring an update on the last piece of the economic puzzle yet to turn around -- wages.

With the Fed ending its policy of "quantitative easing," as the asset purchases were known, the focus now turns to the timing and pace of interest rate hikes. Most forecasters expect the Fed to start raising rates in mid-2015.

Given that stocks rallied off of the October 15 low on Bullard's comments -- and the hope that quantitative easing would be extended -- it's possible that stocks suffer a pullback on fears that the economy will lose momentum without the Fed's help, as it did after the first two rounds of bond buying in 2010 and 2011. Any softening in the economic data would accelerate such a response.

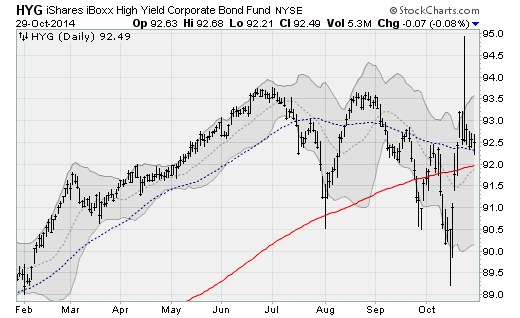

After smooth and easy conditions over the last two years, investors should prepare for some volatility and chop heading into 2015 as financial markets no longer enjoy the steady inflow of cheap dollars from the Fed. A key gauge to keep an eye on is high-yield corporate bonds. Any turbulence here will be a sign that liquidity is disappearing and that the selling pressure that hammered stocks a couple of weeks ago is about to return.