Fed rate hikes might give Wall Street an unpleasant surprise

For years, to bolster the bull market, the Federal Reserve has erred on the side of dovishness. Former Fed Chairman Ben Bernanke delayed the start of tapering its bond buying stimulus program in 2013. Chairman Janet Yellen surprised many when she didn't raise interest rates in September 2015 -- for the first time in nearly a decade despite high expectations -- waiting until December instead.

But more recently, as the unemployment rate has fallen to just 4.3 percent, inflation has stabilized near the Fed's 2 percent target, and financial market and real estate asset valuations have soared, Yellen and her cohorts have changed their approach. After hiking rates just twice in the two years through 2016, they've accelerated their pace to two rate hikes over the past six months.

And now, they raised rates again on Wednesday afternoon, by a quarter percentage point, and likely will once more sometime later this year (based on their estimates), as well as start the process of rolling back their bloated $4.5 trillion balance sheet, reversing years of bond-buying stimulus. This is far more aggressive than Wall Street is expecting.

Is Yellen about to deliver some Volcker-style tough love to investors? As Federal Reserve chairman for eight years through 1987, Paul Volcker pushed up interest rates sharply to conquer then-rampant inflation, a policy that propelled the nation into a recession and punished the stock market.

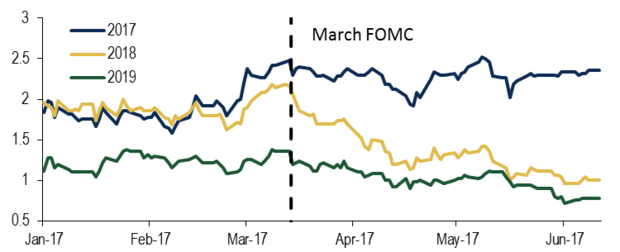

As shown in the chart above, driven by recent disappointments in the economic data (missing analyst estimates by the largest magnitude since early 2016), the market has lowered its rate hike expectations. Wall Street currently only sees around three more rate hikes, including Wednesday's, through the end of 2019 pushing rates to a high of 1.75 percent.

Fed officials, on the other hand, have penciled in rates at 3.0 percent.

This is no small matter, as pessimism in the rates market has pushed down long-term Treasury yields to around 2.2 percent from a high of 2.6 percent in March. Should the Fed keep pushing up short-term policy rates, they risk creating a "yield curve inversion" -- where short-term rates are higher than long-term ones, which is a key indication of a pending recession. Gluskin Sheff economist David Rosenberg believes an inversion, at the current pace of things, could happen sometime early-to-mid-2018.

Bank of America Merrill Lynch economist Michelle Meyer believes it will be hard for the Fed to deliver the "dovish hike" that the central bank would prefer to do: tightening rates to keep a lid on inflation and asset price gains, but not spooking the market. The latest flavor in central banking circles is to lower inflation expectations -- as the European Central Bank did last week -- to account for the recent weakness in energy prices and give a wink to Wall Street that the rate hike pace could very well slow.

This could be combined with a decline in the Fed's own interest rate projections, known as "lowering the dots" in reference to the scattershot chart of individual Fed policymaker estimates. Indeed, in the past when Fed and market rate path expectations deviated, the Fed always lowered their estimates to match Wall Street's. We wouldn't want to spook the stock market, would we?

The same trick might not work this time.

As Merrill's Meyer notes, the gap in rate hike expectations are extremely wide: The market is pricing in less than 0.5 hikes over the next five policy meetings, versus an average of 1.5 hikes during this cycle. This is the second lowest amount of tightening expected over the next five meetings since 1994. In Meyer's words: "The market notably reduced its hike expectations following the March [policy meeting] making it difficult for the Fed to sound more accommodative than current pricing."

Adding to the difficulty was a rather hot producer price inflation report on Tuesday: The "core" inflation rate, stripping out volatile food and energy, increased from 2.1 percent from 1.9 percent, above the Fed's 2.0 percent target. Assuming a strong retail sales and consumer price inflation report Wednesday morning, before the Fed's policy announcement, Yellen will be hard-pressed to justify with a straight face the dramatic lowering of rate hike estimates Wall Street wants to see.

Thus, the risk of a hawkish negative surprise is high. And Wall Street could suffer a dose of tough money love from the Fed; something it hasn't experienced in some 10 years.