Wall Street looks to economy and politics for cues

Both Main Street investors and Wall Street traders have plenty to contend with after the Memorial Day break. The week's economic calendar is full, with updates on everything from the unemployment rate to manufacturing activity and personal income and spending.

And the political scene in Washington, D.C., should be crowded -- after something of a reprieve last week as President Trump traveled overseas -- with former FBI director James Comey set to appear before Congress to discuss his firing and alleged connections between the Trump campaign and Russia.

As a reminder, stocks suffered their worst one-day loss since September 2016 two weeks ago amid headlines that Mr. Trump pressured Comey to drop the investigation into former national security advisor Michael Flynn's connections with Russia. So watch for some price volatility to reappear.

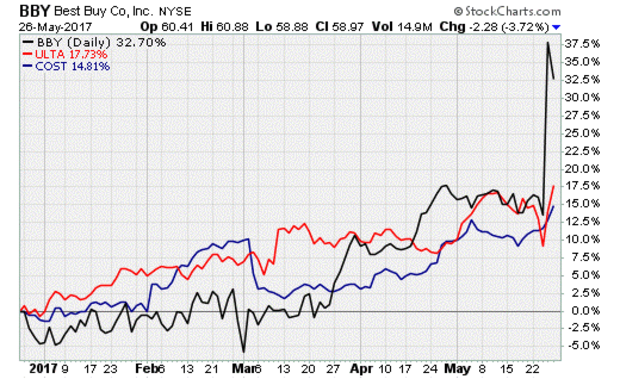

As much as investors would like to just ignore what's happening in Washington to focus on more exciting things -- like rare retail successes by the likes of Ulta Beauty (ULTA), Costco (COST), and Best Buy (BBY), for example, which are being rewarded by big stock price gains as shown below -- one cannot forget that the single largest catalyst of the past seven months has been Wall Street's discounting of possible pro-growth legislation from President Trump.

This is made more important by the fact that the actual "hard" economic data has been soft and that U.S. economic data overall is disappointing to the downside on a scale not seen since late 2015, according to the Citigroup Economic Surprise Index.

A lot of pro-growth legislation has been priced into the stock market since Election Day. Yet without progress on pro-growth things like tax cuts, healthcare reform and infrastructure spending, these gains could be quickly reversed as economic and earnings growth expectations -- which are high and rising -- are forced lower.

Another factor to consider as the economic data rolls out this week is the fact the latest Fed meeting minutes last week all but confirmed a June rate hike and set the stage for the start of a balance sheet taper (undoing years of so-called quantitative easing) sometime later this year, possibly in September.

The fear, being expressed by the bond market via an odd downward drift in long-term yields (shown above), is that the confidence is misplaced. Yields normally decline (and bond prices rise) in anticipation of lower economic growth and lower inflation -- pretty much the polar opposite of the sentiment being expressed by stock prices.

There's plenty of evidence something troubling is happening just below the surface of the economy, from a slowdown in auto sales, stagnant retail spending, weak inflation, and a rollover in income tax withholdings. Economists at Bank of America Merrill Lynch, in fact, believe the "data do not justify a hike at the June meeting" although the "Fed is committed to forging ahead."

Among their concerns are cracks in consumer credit, with new mortgage originations dropping to $491 billion in this year's first quarter from $617 billion in the fourth quarter of 2016. Demand for revolving credit is dropping. Demand for commercial and industrial loans is also stalling.

We'll know more as the week plays out, revealing whether the confidence in stocks or the pessimism in bonds is the correct outlook.