Brexit: Will the latest U.S. stock rebound last?

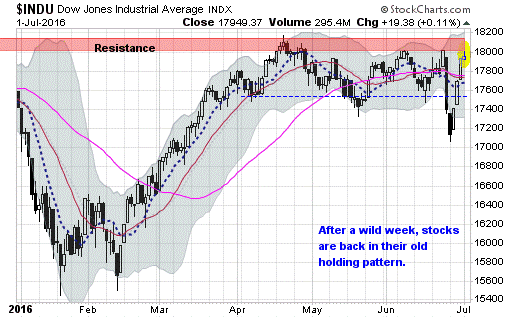

What a difference a week makes: Stocks have roared higher over the past five trading sessions to push the Dow Jones Industrial Average back above the 18,000 in mid-day trading last Friday. All the fear and uncertainty surrounding the surprise Brexit vote the previous week faded faster than what even the most ardent market bull could've hoped for. Call it the "Bre-lief" rebound -- as in, relief in the belief that this too shall pass.

The S&P 500 gained 3.3 percent over last week, its best performance since October 2014. The weakest, most shorted stocks were up 10.1 percent over the most recent four trading days, the biggest short squeeze since May 2009. Financial stocks have enjoyed their strongest spike in three months.

This market, pumped up on central bank stimulus, just refuses to stay down in yet another repeat of the V-shaped recoveries we've seen so often during this bull market. Remember the 2014 Ebola freakout? Probably not. And that's the point.

But will the gains continue?

To be fair, as the dust settles it looks like Brexit may not be as catastrophic an event as was initially feared. In the best traditions of European bureaucracy, the process will likely take years to play out -- debated, discussed and legislated until ennui takes over. Capital Economics also noted the rising possibility that Brexit actually won't happen, with Scotland and Northern Ireland supporting "Remain" and the British government in no hurry to invoke the Article 50 exit clause that triggers a country's exit process from the European Union.

Yet as time goes on -- and debt, leverage and overconfidence builds amid a normal business cycle maturation -- these rebounds are becoming increasingly hollow, vulnerable and hard to justify. Don't take my word for it: Aggressive rallies in government bonds and precious metals belie the confidence in equities.

Stocks have gravitated towards the Dow 18,000 level for the last few months, capping a three-year-old consolidation range that started when the Federal Reserve ended its QE3 bond-buying program. We've been sliding sideways ever since.

Moreover, the "More Stimulus!" headlines that helped rally stocks so hard last week were hardly groundbreaking. Bank of England Governor Carney said more stimulus would likely be needed over the summer while the European Central Bank is reportedly considering a change in how it allocates its bond purchase stimulus amid an ongoing investor "melt up" in government bonds that is limiting the pool of assets available for banks and governments to buy.

All this amid an ongoing corporate earnings recession, the looming start of the Q2 reporting season, the specter of Federal Reserve interest rate hikes, and an uneven global economy. Crude oil looks vulnerable to fresh weakness as short-term supply disruptions ease and drilling rig counts rise again. And an ongoing tightening in the U.S. labor market -- coupled with evidence of falling labor productivity -- threatens to trap the Fed in a "stagflation" scenario.

As noted by Gluskin Sheff economist David Rosenberg (the famous bear who turned bullish between 2012 and 2015), the situation has become fragile. He recently warned clients of a "sub-par global economy, burdened by excessive debt and supply gluts in practically every market, and an equity market challenged by what is still a very murky earnings outlook." He has recommended using the current relief rally to lighten up on cyclical positions and focus on classic defensive assets like bonds and income-yielding stocks.

Other concerns he highlights includes U.S. election uncertainties; rising tides of nationalism, isolationism and trade protectionism; relentless cuts to U.S. capital goods orders; and weak regional manufacturing-activity surveys. To this list I would add unimpressive technical support for the current rebound.

Overall, just 53 percent of the stocks in the S&P 500 are in uptrend vs. 74 percent in early June and nearly 80 percent back in April (when the Dow was trading 250 points lower). This narrowing base of support shows the bulls are relying on a shrinking group of stocks to keep the major averages aloft -- not exactly a sustainable situation.

No wonder Wells Fargo Investment Institute's Peter Donisanu is encouraging clients to not be complacent in light of the recovery rally, but "remain prepared for periods of heightened levels of financial market volatility." The Institute of International Finance is also warning that Brexit-related volatility is likely to continue over the summer as the British economy is being pushed into recession.

Buckle up, because this wild ride isn't over yet.