The Ideal Spending Plan

This article is provided and sponsored by:

ClearPoint Credit Counseling Solutions

____________________________________

How much did you spend last year on entertainment? Food? Gasoline? Most of us have no idea. Figuring out how much you spend and where you spend it will allow you to make adjustments to your household budget and to meet your financial goals.

To determine your average annual costs for categorical spending, you'll need to track your daily expenses for several months. Make sure to account for less obvious payments that are automatically deducted from your paycheck, added to your mortgage, or applied to your credit card such as health insurance, property taxes/insurance and gym memberships, respectively.

Once you've come up with your numbers, you will determine some household budget percentages. Calculate the percentage of your annual gross income that you spend in each area. Then take a look at the results.

Are you surprised by your budget allocations and household budget percentages? Seeing the cold hard facts is often enough to motivate and encourage changes in our spending behavior. In the case of a family with two children between paying for cable, going to the movies, taking vacations, buying MP3s and lottery tickets–it is likely that they have spent $7,100 a year on entertainment and haven't saved for their children's college educations. It is enough to make you consider shifting your priorities and making a more balanced spending plan.

Your budget has to fit your lifestyle. A liberal spender making $200,000 a year, for instance, might allocate more than 10 percent of his or her income to transportation because the family regularly leases new luxury cars. More cautious spenders with the same income might allocate much less to that category because their families buy older, moderately-priced cars, and drive them until they wear out. As a result, the conservative spender has more funds left to allocate to savings. So, even with the same income, their spending plan and budget percentages will differ.

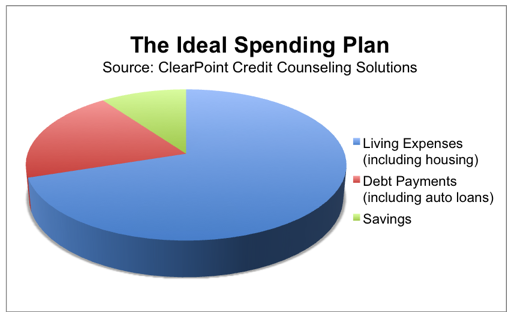

Division of a household budget depends upon a particular family's income, lifestyle, and financial goals. In general, financial experts recommend that we live on no more than 70 percent of our net income (including housing). At least 10% should be dedicated to savings and no more than 20 percent spent on consumer debt such as credit cards and car loans.

Now that you have a spending plan for reference, you can see how you match up. Hopefully, your plan is similar to the chart above. It's extremely important that your debt level is below 20%. If it isn't, or if you have other financial questions you would like answered by a certified credit counselor, contact ClearPoint Credit Counseling Solutions.