Why year-end investors should bail on oil stocks

Stocks dropped again on the penultimate trading day of 2015 in light pre-holiday action as inventory concerns pummeled crude oil.

And now, with 2015 quickly drawing to a close, and many investors focused on harvesting losses for tax purposes, it's time to consider what parts of your portfolio should be sold. It looks to be anything related to the energy sector.

As I've been saying for weeks, seasonal strength (the "Santa" effect) and light volumes have kept a lid on stock and bond market volatility recently.

As things stand now, the S&P 500 is up 0.2 percent for the year to date, while the Dow is down 1.2 percent and remains constrained by a resistance pattern of lower highs going back to May. The blue-chip benchmark hasn't crossed the psychologically important 18,000 level since July. And measures of market breadth -- or how many stocks are participating to the upside -- have been deteriorating for months.

But by the time we head into the second week of January, junk bond risks, stalled corporate earnings, slowing U.S. economic growth, weak oil prices and the specter of another four Federal Reserve interest rates hikes (based on the policymakers' forecasts) should spook investors into a fresh bout of selling.

Energy stocks and high-yield bonds issued by U.S. shale producers will likely be at the epicenter of this selling.

The American Petroleum Institute's inventory data, released Tuesday afternoon, showed a stockpile build of 2.9 million barrels, far ahead of expectations. While Wall Street bucked that bad news for crude on Tuesday, Wednesday's Energy Information Administration numbers showing a 2.6-million-barrel build vs. a drop of 5.9 million barrels last week had the opposite effect: On Wednesday, crude oil lost 2.9 percent to close at $36.76 a barrel.

Adding to selling pressure were comments from Saudi Arabia's energy minister that his country's oil output strategy is "reliable" and it's not about to change. The market is also bracing for a surge of Iranian crude when economic sanctions are lifted in 2016.

Other wrinkles include rising U.S. oil production, the limited impact of rising global energy demand (efficiency efforts have lessened the "oil intensity" of GDP growth) and the fact that global crude storage is quickly approaching capacity. Seasonally, stockpiles tend to drop at the end of the year and rise in the first few weeks of the New Year due to tax implications. So, any further rise in supply in early 2016 could well push crude oil to fresh lows not seen since the early 2000s.

A tank-topping in various areas of the energy market is looking increasingly likely heading into 2016. In a recent note to clients, Goldman Sachs said avoiding such an inventory top-out would require a slowdown of output, due to producer financial stress as they get cut off from funding. But that slowdown just isn't happening.

Goldman's warning: Oil may need to fall to near $20 a barrel to force production cuts.

Much damage has already been done.

The Barclays High Yield Bond ETF (JNK) recently traded down to levels first reached in 2012 and is off more than 11 percent from its 2014 high -- a stomach punch wiping away years of dividend payouts for conservative fixed-income investors.

Energy stocks as represented by the Energy Select SPDR (XLE) are down 38 percent from their 2014 highs. And because of the drag from the decline of energy-sector profits, S&P 500 earnings growth are on track for their third consecutive quarterly decline -- something not seen since the financial crisis.

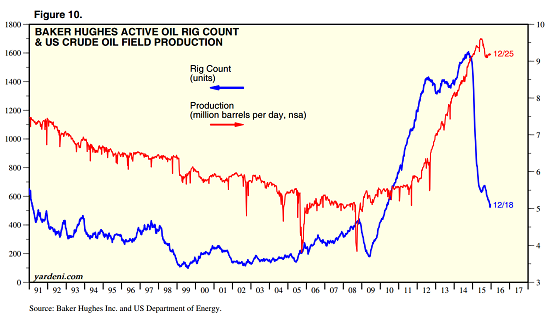

While U.S. drilling rig counts have fallen sharply, production is barely below its recent high as shale producers have focused on low-cost wells (chart above). As credit costs rise, thanks to the Federal Reserve's rate hikes, the incentive will be for U.S. producers to pump even more -- despite the lower per barrel price -- to try to cover increasingly expensive financing costs.

Until a wave of bankruptcies and defaults in the energy sector forces U.S. production lower, resulting in losses for investors in these areas, this dynamic will continue. And that means there's no reason to hang on when you can still do some year-end selling.