What would the Ryan plan really do?

(MoneyWatch) Mitt Romney's selection of Rep. Paul Ryan as his vice presidential running mate thrusts the Wisconsin Republican's budget plan back into the spotlight five months after its initial release. Not that Romney seems eager to embrace the controversial proposal, which critics say would harm lower-income Americans while benefiting the wealthy.

Romney, the Republican presidential nominee, appeared to want to distance himself from the Ryan plan on "60 Minutes"Sunday in telling CBS News chief Washington correspondent Bob Schieffer, "Well, I have my budget plan, as you know, that I've put out. And that's the budget plan that we're going to run on."

By contrast, when the Ryan budget was unveiled in March Romney said, "I'm very supportive of the Ryan budget plan," adding the following week that "it would be marvelous if the Senate were to pick up Paul Ryan's budget and adopt it and pass it along to the President."

Considering that Romney selected as his veep a lawmaker who is most famous for authoring the House-approved budget, some observers expected him to more openly adopt most, if not all, of the plan. Still, Ryan's presence in the campaign means it's time to take another look at the his plan, dubbed "The Path to Prosperity: A Blueprint for American Renewal" (known less colorfully on Capitol Hill as the House Budget Committee -- Fiscal Year 2013 Budget Resolution).

Why the fuss over Paul Ryan's Medicare plan?

Romney & Ryan: The first interview

Watch: Can Paul Ryan win independent voters

Budget/debt/deficit

If you are one of those people who think that balanced federal deficits are the best thing since sliced bread, there's some bad news in Ryan's plan: It would not balance the budget for another 28 years, according to analysis by the nonpartisan Congressional Budget Office. When the CBO examined the Ryan budget, it projected that the deficit in 2022 would be about the same as the CBO baseline, or 1.2 percent of U.S. GDP.

Indeed, much to the chagrin of deficit hawks, balancing the budget does not appear to be one of the top priorities of the Ryan plan. When the House put a balanced budget amendment up for a vote for the first time in 16 years last November, Ryan voted against it. (The final vote was 261-165, less than the two-thirds majority needed to pass a constitutional amendment.)

In the past, Ryan also has not been afraid of spending. He voted for the George W. Bush tax cuts, the war in Iraq, the Medicare Prescription Drug Benefit, the 2005 highway bill (which included the famous "Bridge to Nowhere" in Alaska) and the $700 billion financial industry bailout, or TARP.

Taxes

Ryan appears to believe in the supply-side economics espoused in the 1980s by President Ronald Reagan and Ryan's former boss, late New York congressman Jack Kemp. Supply-siders believe that high taxes inhibit economic growth and low taxes spur growth. (For a deeper dive into these theories, go here.)

The Ryan plan would extend the 2001 and 2003 tax cuts enacted under President Bush, which are set to expire at the end of this year. It would enact another $4.5 trillion in cuts over the next decade, excluding the $5.4 trillion in revenue lost from permanently extending the Bush-era tax cuts.

The plan would scrap the current six marginal tax rates and replace them with just two rates: 10 percent and 25 percent. The Ryan plan would repeal the Alternative Minimum Tax, cut the corporate tax rate from 35 percent to 25 percent, and eliminate the tax provisions of the 2010 health reform law.

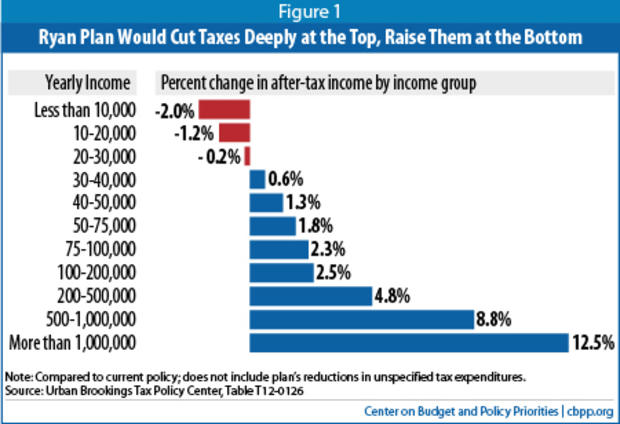

How does all of this affect you? According to estimates from the Tax Policy Center, federal income taxes would drop significantly for high earners -- those earning over $1 million could see an average tax cut of $265,000, primarily due to the elimination of most of the taxes on investment income. "By contrast, half of those making between $20,000 and $30,000 would get no tax cut at all," the Washington think-tank concluded. Middle-income earners -- those earning between $50,000 and $75,000 -- would likely see average annual tax savings of $1,000, a which amounts to a 2 percent boost in after-tax income.

These tax cuts would add $4.6 trillion to the federal deficit over the next decade, according to the TPC. To foot the bill, the Ryan plan would eliminate existing tax deductions, credits and exclusions to "broaden the base" of the tax code, though the proposal does not specify what would be cut.

That lack of detail has led to a lot of guessing. For instance, would the plan eliminate or limit the popular mortgage interest deduction, ditch the exclusion of employer-provided health insurance from income, limit the charitable contribution deduction? For now, this all remains conjecture.

Social Security, defense and domestic spending

Here's what the Ryan plan would not cut: defense spending and Social Security, which together account for about 40 percent of the federal budget. The plan would increase the military budget by $300 billion over the decade. To balance that rise, Ryan would slash non-defense spending, keeping the across-the board cuts that are due to occur in 2013, and deepen those cuts by an additional $700 billion over the next decade.

Under the Ryan plan, pretty much everything else would be on the chopping block, including (but not limited to) unemployment, food stamps, Pell grants for college students, veteran benefits, transportation, research and national parks.

Medicare

In the run-up the November election, Democrats have started training their fire on the Ryan budget for seeking to "eliminate Medicare as we know it." Yet while the Ryan plan would overhaul the Medicare system, for seniors already in the plan and for those who are 55-to-65 years old, everything would remain as is.

For everyone under age 55, Ryan's Medicare system would look starkly different from the current system, where the government pays health care providers. Under the plan, seniors would receive a fixed amount of money, also called a "premium support payment," which is essentially a subsidy or a voucher. Americans would have the option of using that money to buy private health insurance or enroll in Medicare. If a health plan cost more than the government contributed, seniors would have to pay the difference. Additionally, the Ryan would gradually lift the Medicare eligibility age from 65 to 67 by 2034.

The reasoning behind the Ryan plan is that seniors will wisely shop for the cheapest plans, and as a result competition among insurers would push down health care costs for everyone. According to the CBO, under the Ryan plan the average Medicare participant is likely to pay an additional $1,200 and $2,400 a year, unless health care costs rise much more slowly.

CBO also said that both the Ryan plan and current law could lead to "reduced access to health care; diminished quality of care; increased efficiency of health care delivery; less investment in new, high-cost technologies; or some combination of those outcomes. In addition, beneficiaries might face higher costs, which could in turn reinforce some of the other effects."

Medicaid

Medicaid is a joint program between the federal government and U.S. states that provides healthcare for the poor and disabled and also includes a sister plan that pays for healthcare for children. Under the Ryan plan, Medicaid would be cut by about a third, and the program would be run primarily by states. The federal government would fund its share of the program as a block grant to states, which would be adjusted annually according to inflation and population growth. In turn, states would use the funds to provide services. Critics say that the states, which are already under fiscal pressure, would likely cut Medicaid.