What investors should expect in 2016

As 2015 drew to a close, the bulls and the bears continued the trench warfare they've been engaged in since late 2014 -- keeping stocks dipping in and out of the red for the year. In the end, the Dow Jones industrials remained just below the 18,000 level that it first closed above on Christmas Eve 2014.

Overall, the year was a disappointment for many: Consider that Apple (AAPL), the most popular and widely held single stock based on its market capitalization, posted its worst year since 2008. Both investment-grade and high-yield corporate bonds are down for the year. Crude oil has lost more than $10 a barrel, a little more than 30 percent for the year. Even interest rates are higher after the Federal Reserve tightened policy earlier this month for the first time since 2006.

So what will 2016 bring? Here's a quick look.

Stocks

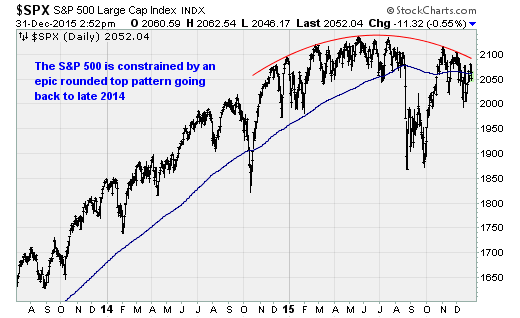

On a technical basis, stocks look vulnerable heading into the New Year. The S&P 500 has dropped back below its 200-day moving average and is constrained by an epic "rounded top pattern" that started in late 2014. This pattern is typically seen at the end of long-term bull markets, a slow grinding pattern of higher highs and higher lows giving way to a pattern of lower highs and lower lows over many months.

Unless the bulls can break up and out of the pattern, with a surge back over the 2,100 level on the S&P 500, the bears are running the show. Adding to the worries has been a steady narrowing of measures of market breadth, or the percentage of stocks in the market participating to the upside -- a sign of waning buying interest that suggests lower prices are coming.

Another way to look at the vulnerability of the overall stock market has been the reliance on a small group of big-tech stocks -- including Netflix (NFLX) and Facebook (FB) -- to keep the major averages held aloft while more, and less popular, issues roll over.

Economy

Just a couple of weeks after the Fed raised interest rates, the U.S. economy is starting to whimper. Manufacturing activity is slowing sharply, with industrial production dropping 0.6 percent in November for the weakest monthly result since 2012. Home sales are slowing. The list goes on.

As a result, the Atlanta Fed's real-time GDPNow tracking estimate of fourth-quarter GDP growth has collapsed to just 1.3 percent. Whether this slowdown will weigh on job growth remains to be seen. We'll know more when the government releases the December payroll report on Friday, Jan. 8.

Interest rates

After the Fed raised short-term interest rates by 0.25 percent, the focus is now on what pace the Fed will take on subsequent rate hikes in 2016. Currently, Fed policymakers are pricing in four more quarter-point hikes based on their individual forecasts in the Summary of Economic Projections, or "dot plot" of estimates. That pace is already much slower than what the Fed did during the last few policy tightening campaigns.

But the futures market expects only two quarter-point hikes. This disconnect will need to be closed, either by the Fed acquiescing to Wall Street's desires and softening its approach, or by the Fed standing firm and forcing the markets to realize the era of ultra-cheap money is in fact ending.

Oil prices

A growing oversupply problem and rising risk of "tank tops" as inventories swell will likely push crude oil prices even lower in early 2016. Even though U.S. shale oil producers have been idling drilling rigs, overall production remains just off its high as more productive, lower-cost wells are ramped up.

Moreover, OPEC is continuing its price war against U.S. shale. And traders are shuddering at the thought of Iranian crude hitting the market as economic sanctions against the country are lifted. Goldman Sachs recently warned clients that a drop to the $20-a-barrel level could be necessary to force the production cuts necessary to balance supply and demand.

Everything from energy stocks to high-yield bonds of shale producers will depend on whether this scenario actually plays out.

Earnings

Because of the drag from a stronger dollar (which hits U.S. corporations' foreign earnings) and weak oil prices (which hits energy sector profits), overall S&P 500 earnings growth is expected to drop in the fourth quarter for the third consecutive period, according to FactSet data. That hasn't happened since the financial crisis.

Specifically, earnings are expected to decline 4.7 percent in the quarter over the same period in 2014. This is a big markdown from the 0.6 percent drop expected at the end of September. Energy and material earnings are the big weight here.

Analysts are pretty dour on the outlook for the energy sector looking into 2016. Their aggregate earnings estimates are down 15 percent since September, and a year-over-year earnings decline of 8 percent is now expected for the calendar year. But this actually represents a stabilization of sorts, at least enough to push overall estimated S&P 500 earnings growth to 7.5 percent for 2016.

Here's hoping that this time next year, we're marveling at how well 2016 turned out despite all the reasons to worry.