What happens if the bitcoin bubble pops?

The enormous run-up in bitcoin's price this year has spurred talk that it's a bubble bound to burst. That sounds ominous. But take heart: If bitcoin's bubble pops, the pain likely will be restricted to those who bet on the cryptocurrency -- and not harm the wider market and economy very much.

Compared to past investment manias that came to grief, such as the 1990s dot-com craze and the housing boom of the past decade, a bitcoin rout likely would be of small magnitude.

Certainly, bitcoin's gains have been breathtaking enough to invite worry. Bitcoin, created as a faster and government-free means of exchange, has had such a sudden ascent that it's scary to many on Wall Street. Jamie Dimon, chairman of JPMorgan Chase (JPM), has labeled it a "fraud," and Bespoke Investment Group warned that the "herd mentality" that has pushed its price precipitously skyward would end in tears.

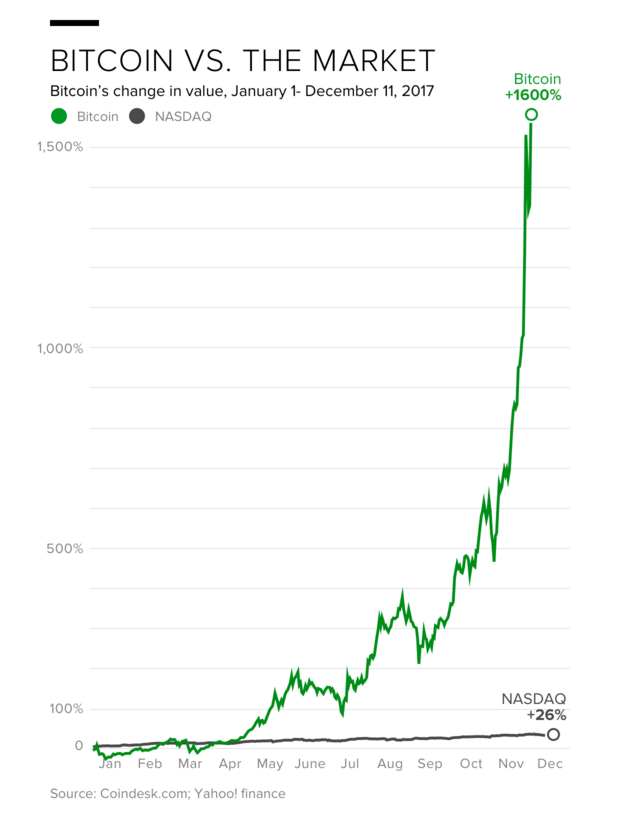

This year, bitcoin's price has enjoyed a 1,600 percent increase, shooting past $17,000 on Monday. It far eclipses the Nasdaq Composite's 26 percent advance. The cyber-currency "is now officially an investor mania," wrote Joshua Brown, an adviser with Ritholtz Wealth Management in a blog post. "Like all manias, when it turns, people are going to be wiped out."

Bitcoin is notoriously volatile, with double-digit drops common. In June, for instance, it fell 19 percent in one day. And many of the people piling into bitcoin appear to be speculators, not long-term investors who believe in its future. While the digital dough has found increasing acceptance among some retailers, with the likes of travel service Expedia accepting it, bitcoin and its smaller rivals like Ethereum have a long way to go.

That's because a taint lingers about the stuff. Bitcoin, because of its anonymity, rivaling cash, is a favorite among drug dealers and other criminals. Securities and Exchange Commission Chairman Jay Clayton cautioned on Monday that investors must be wary of cryptocurrency and especially of a spate of new "coin based offerings," where digital money firms raise money by distributing their internet-based coins.

Adding fuel to the worries is the launch of bitcoin futures contracts. Cboe Global Markets debuted its product on Sunday, which allows established Wall Street players, leery about the digital currency up to now, to get involved with it. CME Group, the biggest derivatives trading platform, will unveil its own bitcoin futures on Dec. 18. High-end investment firm Goldman Sachs (GS) has indicated it will clear bitcoin futures trades, where it acts as an intermediary between buyer and seller.

In raw dollar terms, bitcoin's presence seems to be formidable, with a market capitalization of $292 billion. That puts it ahead of all but 10 of the Standard & Poor's 500 members, just behind Bank of America (BAC) at $301 billion (No. 10 on the list) and Apple (AAPL) at $885 billion, the nation's most valuable company.

Still, amid all the jeremiads about the dangers of bitcoin, a sense of proportion is lacking. A bitcoin collapse probably wouldn't have much affect on other parts of the capital markets or the economy because, despite the impressive numbers of its bull run, its reach is meager.

If bitcoin's price dropped to zero, the loss would equal a fall of just 0.6 percent in U.S. equity prices, according to Capital Economics. Plus, "there is no correlation" between bitcoin prices and other assets, so it "should not affect wider financial conditions," according a recent report by the research firm.

In other words, such a swan dive could rival the damage of the sports card mania of the 1980s and 1990s -- a blow to some when it fell apart, but not to the general public.

And unlike other bubbles, as Gavekal Research has noted, the bitcoin rally is not largely powered by leverage. Borrowed money magnifies the scope of financial damage. The housing bust showed just that when a wave of defaulted mortgages swamped the debt-laden securities that Wall Street had packaged them into and battered the banks that held them.

Certainly, the impact of previous bursting bubbles has been far more widespread than the end of the bitcoin enthusiasm could produce.

In the Dutch tulip fad of the early 1600s, people pledged their houses and other valuables to buy the bulbs, which flower lovers craved. When the overvalued market imploded, Holland plunged into a recession. A similar frenzy enveloped Britain in the 1700s, as investors bid up shares of trading companies doing business in the Americas and the Pacific. When these companies didn't deliver the promised bounty and the so-called South Sea Bubble burst, the British government had to bail out the banks threatened by the collapse.

In the 1920s, a similar investing passion raged as everyone from the well-heeled to shoeshine boys borrowed money to buy stocks in a roaring market, where some of the offerings were not quite legitimate. When manufacturing and farm overproduction sent companies' prices and profits plunging, the stock market crashed, impoverishing millions of people, and ushering in the Great Depression.

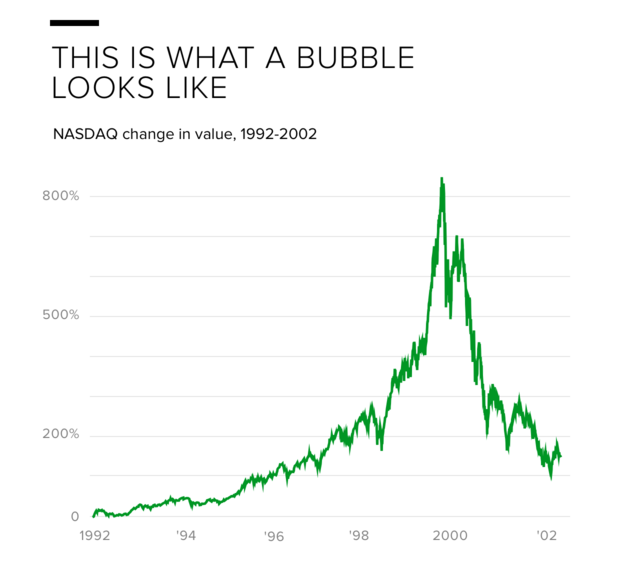

The dot-com vogue of the 1990s saw the creation of myriad firms promising riches, even though many had no hope of turning a profit. Fed by passionate stock investors, these ambitious internet outfits pushed the tech-heavy Nasdaq Composite to new highs. But finally, too much red ink tried investors' patience. The Nasdaq tumbled three-quarters from its high point, in a market retreat that lasted from March 2000 to October 2002.The debacle touched off a recession, although the downturn was brief and mild because the tech tyros had used little leverage.

Borrowed money was at the heart of the housing disaster, however: Thanks to low interest rates and loosened lending standards, many people who never could qualify for a mortgage before suddenly borrowed large sums to buy houses. When they couldn't make their payments, the effect almost destroyed the international banking system and created the Great Recession.

Thankfully, such a dire situation doesn't appear to be the case for bitcoin and its ilk. At least, not yet.