Wall Street's quiet spell is getting worrisome

The U.S. stock market is the largest in the world, representing the vibrant beating heart of global capitalism. But lately things are pretty dull. Anyone feel a pulse?

For many, market calm may be a confidence-boosting break from the harrowing volatility seen earlier in the year. But with a number of major catalysts on the horizon -- including the U.S. presidential election -- worry is growing that this is merely the calm before the storm.

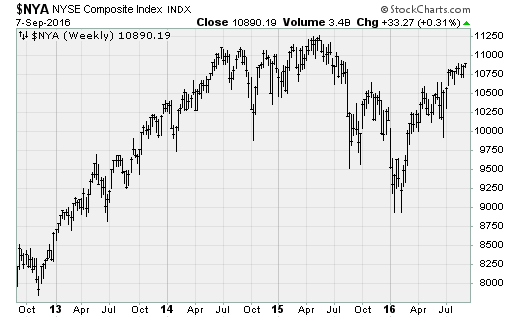

Broadly measured by the NYSE Composite Index, American stocks notched incremental new highs in the spring of 2015 and after an energy-driven scare earlier this year, are trading near levels first reached in the summer of 2014. That has them in the upper end of an oppressive three-year trading range (chart below).

Narrower measures, like the Dow Jones industrials index, hit new highs back in July after rebounding from the short-lived post-Brexit sell-off. But since then, the blue-chip metric has since gone into stasis, staying within a 1.3 percent range. Trading volumes have fallen off as well, with activity at levels not seen since the holiday break in December.

In fact, according to Dana Lyons of Lyons Fund Management, over the past 40 days the Dow has traded in its tightest range in at least 100 years. For context, the next narrowest range was between December 1922 and February 1923. Given the unreliability of historical stock data, it’s very possible this is the quietest period for stocks ever.

It’s enough to turn Gluskin Sheff strategist David Rosenberg near-term bearish on stocks amid what he calls “extremely bullish” positioning in the equity futures and options market, a very low reading on the CBOE Volatility Index (or the VIX, Wall Street’s fear gauge) and lofty equity market valuations. In Rosenberg’s mind, the current bullishness isn’t justified by some hard numbers and fundamentals.

Let’s not forget the ongoing corporate earnings recession (expected to reach, at least, into its sixth consecutive quarter) and a recent rollover in U.S. economic data. The August jobs report disappointed, factory orders are weak, manufacturing had an outright contraction (its first since February) and construction spending continues to decline.

The nonmanufacturing ISM index, which measures growth in the larger services sector of the economy, suffered its largest month-over-month slowdown since 2008 and fell to its weakest level since early 2010.

Rosenberg also highlights looming “event risks,” including the Fed’s September and December interest rate decisions (when hikes are possible), a constitutional referendum in Italy in October (shades of Brexit) and, of course, the outcome of what’s shaping up as the most contentious U.S. presidential election in generations.

Marko Kolanovic, head of JPMorgan’s quantitative research department, warns that the eerie calm is about to end with a “significant increase in realized volatility” likely later this month and into October. Seasonality, central bank decisions and leverage in fancy derivative hedging strategies will all “provide fuel for volatility” in the weeks to come.

Put simply, a share-price drop of only 1 percent or 2 percent would, in his estimation, badly rattle the market by upending current low-price options hedges used by Wall Street professionals. He adds that historically, September is the worst-performing month of the year, with an average decline of 1 percent.

Such a drop could be just enough of a spark to shock Wall Street back to life.