Wall Street sprints to the final hurdle of 2016

U.S. equities climbed to new record highs on Friday in what’s becoming a speculative fever following the surprise electoral victory of President-elect Donald Trump.

Also fueling the rally are seasonal tailwinds in play at this time of the year as well as portfolio shifts as investors pull money out of bonds (which have been hammered) and pour it into stocks. There simply seems to be no stopping the uptrend.

If anything is going to break this streak now, it’s the looming Federal Reserve monetary policy decision on Dec. 14.

Last week, the Dow Jones industrials index gained 3.1 percent, the Nasdaq Composite rose 3.6 percent as big-tech stocks like Apple (AAPL) joined the fray and the Russell 2000 small-cap index climbed 5.6 percent to bring its total gain to 16 percent since the election.

Smaller stocks have been in the vanguard, thanks to their increased exposure to U.S. customers, who are expected to benefit most from Trump’s economic policies. And financial stocks have been getting a lift from higher long-term interest rates, which boost profit margins for banks.

Both investors and consumers are in a “honeymoon” period right now with Trump. In just over a month, after the inauguration, the realities of governing will hit -- and the ebullience will fade as contentious issues like the need to raise the federal debt ceiling in March and the drag on the deficit from higher interest rates become clear.

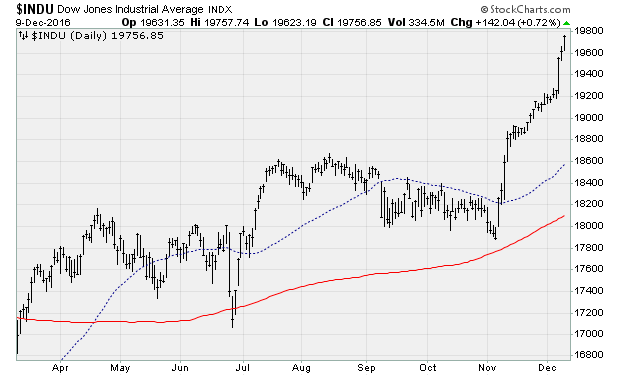

That isn’t to say the uptrend won’t march on into 2017 (chart below). Just that the euphoria should give way to reasoned analysis. Trump’s efforts to clamp down on immigration and open-border trade deals will likely pinch corporate profitability. Plus, his fiscal plans, all else equal, would double the national debt and won’t start coming into effect, according to Goldman Sachs, until 2018.

For now, however, none of that matters.

Overbought technical conditions, red-hot sentiment and stretched equity market valuations? Those don’t matter either, but they’re warning signs for those looking to extend their long positioning.

The Bespoke Investment Group noted that the S&P 500 is well over two standard deviations above its 50-day moving average. The latest Investors Intelligence survey showed investors with bullish sentiment increased to 58.8 percent, the third reading in the “danger zone” and nearing the 60-percent-plus peak seen when the market was topping in mid-2014. And Goldman Sachs pointed out that the median S&P 500 company trades at the 98th percentile of historical valuations.

Investors couldn’t care less. According to Bank of America Merrill Lynch, another $600 million flowed into stocks last week, while $1.2 billion was pulled out of bonds. Financial stocks enjoyed their 11th consecutive weekly inflow. Energy stocks enjoyed their largest inflow in a year.

The only remaining catalyst that could trip up stocks before year-end is the upcoming Fed policy announcement on Wednesday, widely expected to feature another 0.25 percent interest rate hike as well as fresh guidance showing an aggressive pace of hikes in 2017.

Heading into the New Year, Merrill Lynch analysts worry that risks will increase markedly for investors. Trouble could start as soon as February as short-term bonds sell off, joining in the weakness seen in long-term bonds. That would result in a “bear flattening” of the yield curve that ushers in an era of higher growth/higher interest rates that drives higher market volatility.

And it raises the risk of a “bust,” a la 1987, 1994, 1998 and 2008 as the Fed is forced to quickly tighten policy to prevent runaway inflation.