Wall Street thinks Yahoo is worth less than nothing

The Alibaba (BABA) IPO made financial history as the largest public offering ever. In the shadow of that news is Yahoo (YHOO), the old-time Internet "portal," which held a bundle of Alibaba stock and made billions.

And yet, Wall Street has slapped it down. From a 52-week high of about $44 reached nearly two weeks ago, shares had fallen to around $38.50 in mid-morning trading on Tuesday.

Not so long ago, investors thought that Yahoo was essentially worthless, trading at the value of its Alibaba and Yahoo Japan shares. Now? Yahoo is worth less than its holdings. As Fortune notes, Yahoo's market capitalization is about $39 billion, while its Alibaba stake is worth $37 billion and its Yahoo Japan stake is worth $8 billion.

Perhaps the most telling viewpoint is one that Barry Randall, chief investment officer of Crabtree Asset Management, told CBS MoneyWatch on the eve of the Alibaba IPO. He thought the best way for non-insiders to approach Alibaba would be to buy the Yahoo stock after the price stabilizes after the Alibaba IPO.

"The company is essentially worthless [in the eyes of Wall Street] and would be immensely attractive to a private equity firm to leverage the firm because it's still cash positive," Randall said. A potential winning investment strategy would be to purchase Yahoo shares after the effects of Alibaba's IPO have been factored into the price and hold them until someone buys out Yahoo and breaks it up.

The company has descended into negative value, even though it still makes a profit and is one of the most popular Internet destinations in the world. Clearly, the reality of running Yahoo hasn't changed. CEO Marissa Mayer, brought in with great fanfare just a couple of years ago, faces an enormous challenge.

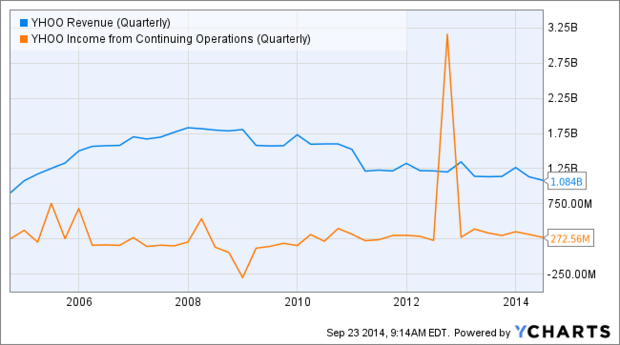

For all the acquisitions and expensive hires that Mayer has undertaken and the push to establish Yahoo as a news and media brand, the company still drifts when it comes to financial performance. Annual revenue has been declining since 2008 and operating income has been roughly flat, except for a spike owing to a share buyback deal with Alibaba in 2012, as the chart generated with Ycharts.com shows below.

Plus, for all the talk of transformation over the last two years, the Yahoo brand hasn't really changed. It remains a collection of services and properties without a resounding identity and clear strength.

Say Google (GOOG) and you think search. Apple (AAPL) is consumer electronics. Facebook (FB)? Social networking. Even often dismissed Microsoft (MSFT) has been financially successful with operating systems and corporate computing.

But most consumers still think of Yahoo as financial information, news, email, photo sharing, or whatever particular services they use. The company doesn't own a market, and that puts it at a competitive disadvantage. Even with its massive traffic -- comScore regularly ranks Yahoo as a top recipient of Internet traffic -- the company isn't a must for a single core constituency.

To shatter Wall Street's cynical view of Yahoo would take more than "fixing" the financial results. A CEO would have to totally remake it and create a reason to make people care. Doing so would require Yahoo to create a breakthrough service or product or buy an up-and-coming young Internet company and then rebrand the entire business under the winner's name.

Barring that, it's still a question whether anyone can steer Yahoo away from an eventual breakup.