Wall Street ducks and covers as it sweats the Fed

Following the market chaos of late August, things have calmed down in recent weeks as everyone prepares for the Federal Reserve's policy decision on Thursday. That announcement could feature the first interest rate hike since 2006 and put an end to nearly seven years of near-zero percent interest rates.

In fact, you could say the market has gone into a sort of stasis.

But don't be fooled: This is just the calm before the storm because volatility is set to rise again following the Fed's policy decision and press conference later this week.

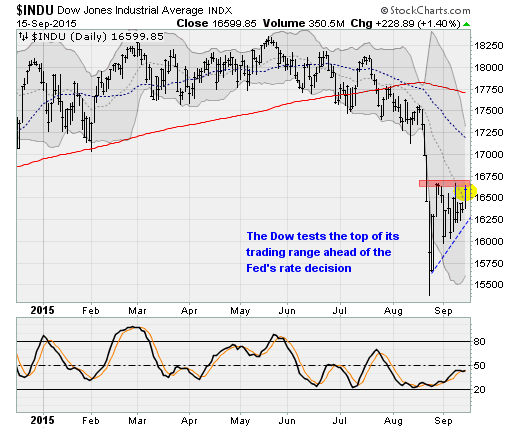

Just look at the chart of the Dow Jones industrials below, which has traded into a fast-tightening range that chartists call a "pennant" formation. Activity has slowed as traders resist placing big bets ahead of the Fed's decision.

According to Nanex data, S&P 500 futures set a new record low for average trade size on Monday, and fewer than 800 million shares moved on the NYSE floor vs. a 20-day average of 984 million. Even as the Dow popped 229 points (1.4 percent) and the S&P 500 rose 25 points (1.3 percent), only 760 million shares were traded on Tuesday.

August had 13 consecutive sessions without a single investment-grade bond being issued, the longest drought since the financial crisis. And it has been nearly a month since an IPO has been launched. That hasn't happened since August 2014.

With the Fed set to start its two-day policy meeting Wednesday, the chatter on Wall Street is increasing as trading activity remains light. No one knows what to expect, but there's no shortage of opinions on the matter.

Current pricing puts the odds of a September rate hike at less than 30 percent. Yet by a slim margin a group of economists polled by Reuters believes a rate hike will happen this week for the first time since 2006. Fed officials themselves maintain a much more aggressive outlook on the pace and timing of rate normalization, opening a massive expectations gap between traders, economists and policymakers.

Bank of Japan Governor Haruhiko Kuroda was upbeat Tuesday morning, saying a Fed rate hike now would be a positive signal. A team of researchers at Deutsche Bank led by David Folkerts-Landau issued a special report outlining their reasons why the Fed should raise rates now. It included:

- A labor market that's at, or very close to, full employment.

- Relatively stable global economic growth prospects.

- U.S. inflation held down by temporary factors as unit-labor-cost inflation increases to levels consistent with the Fed's long-term goals.

- The lags inherent in monetary policy, the risks of waiting too long and the risks of creating asset bubbles and instability by keeping rates near zero percent.

- And evidence, shown in the chart below, that the Fed should no longer be so far from neutral on its policy given that it's so close to its inflation and employment goals.

Bank of America Merrill Lynch economist Michael Hanson believes a September rate hike is the most likely outcome of a close-call decision on Thursday because of the undeniable cumulative improvement in the U.S. economy and job market. GDP growth is set to be upwardly revised to a 4 percent or higher rate for the second quarter. And the unemployment rate has already fallen near the Fed's own estimate of full employment -- 5.1 percent, a level it didn't expect to reach until the end of 2016.

But Goldman Sachs chief economist Jan Hatzius said the Fed is still far away from its 2 percent inflation target, reiterating his expectation of a December rate liftoff window and noting the risk of an adverse market reaction to a rate hike. It's even possible that the Fed will delay any policy changes until 2016, in his view.

With two days to go, all we can do is wait as the tension builds and stocks remain range bound.