Stop hitting your head against a BRIC wall

(MoneyWatch) The acronym BRIC -- which stands for Brazil, Russia, India, and China -- was invented by Jim O'Neill of Goldman Sachs in 2001 to describe a shift in economic power away from the developed countries to the developing world. The prediction was that these countries were growing so rapidly that their combined economies would surpass those of the current leaders by 2050. (In 2010, the term was expanded to BRICS to include South Africa.)

Never letting a good marketing opportunity pass them by, Wall Street quickly developed investment products based on the BRIC theme, and lots of marketing dollars were spent supporting the concept. And, as usual, investors piled in.

Unfortunately, there's no evidence whatsoever that faster economic growth translates into higher investment returns. In fact, the evidence is that there is a slight negative correlation between the two -- countries with above average economic growth rates tend to produce below average investment returns. For example, Jay Ritter's study, "Is Economic Growth Good for Investors?" published in the Summer 2012 edition of the Journal of Applied Corporate Finance found:

- For 19 countries with continuously operating stock markets during the 112-year period 1900-2011, the correlation between stock returns and the growth rate of per capita gross domestic product (GDP) was -0.39, when measured in local currency. When measured in dollars, the correlation changes slightly to -0.32. Investors in 1900 would actually have been better off investing in companies of countries that experienced lower growth of their economies.

- If we focus on more recent data, the 42-year period 1970-2011, whether measured in local currency or dollars, the correlation between economic growth and stock returns is effectively zero.

- For 15 emerging markets (including the BRIC countries), during the 24-year period 1988-2011, the correlation was -0.41 in local currency and -0.47 in dollar terms. The data for China is particularly compelling. While economic growth averaged about 9 percent, stock returns were -5.5 percent per year.

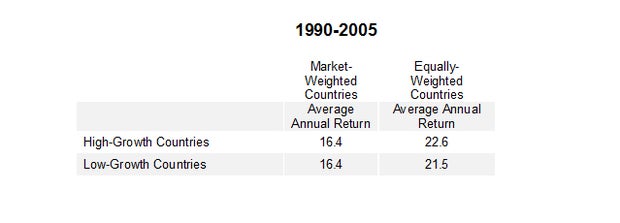

DFA's take on BRICs

Another study, by Jim Davis of Dimensional Fund Advisors, focused on the emerging markets and covered the period 1990-2005. At the beginning of each year, Davis divided the emerging market countries in the IFC Investable Universe database into two groups based on GDP growth for the upcoming year. The high-growth group consisted of the 50 percent of the countries with the highest real GDP growth for the year. The low-growth countries were the other half. He then measured returns using two sets of country weights -- aggregate free-float-adjusted market-cap weights and equal weights. Companies were market-cap weighted within countries. The results are shown in the table below.

It seems that there is not much, if any, advantage to knowing in advance which countries will have the highest rates of GDP growth.

The conclusion we can draw is that the emerging markets are very much like the rest of the world's capital markets -- they do an excellent job of reflecting economic growth into stock prices. In other words, by the time you decide to act on the information about faster growth rates, it's already reflected in prices. Thus, the only advantage would come from being able to forecast surprises in growth rates. For example, if a country was forecast to have 6 percent GDP growth, and it actually experienced a rate of growth of 7 percent, you might been able to exploit such information (depending on how much it cost to make the forecasts and how much it cost to execute the strategy). Unfortunately, there does not seem to be any evidence of the ability to forecast GDP rates any better than do the markets.

Good investments aren't built with BRICS

There's another important insight you should draw from these studies: It isn't necessary to make concentrated, undiversified bets on individual countries and take idiosyncratic risks that can easily be diversified away by owning a broader emerging markets fund. This is especially true of emerging markets, which are often characterized by high levels of volatility, economic and political risk, restrictions on foreign investments, and periodic flights of capital.

In case you were wondering how the BRICs have actually fared, Morningstar provides us with data for the five-year period ending Sept. 27, 2013. The iShares MSCI BRIC (BKF) underperformed Vanguard's Emerging Markets Fund (VEIEX) by 2.2 percent per year (2.3 percent versus 5.5 percent). It also underperformed Vanguard's Total International Fund (VGTSX), which returned 4.8 percent per year by 2.5 percent. And it underperformed Vanguard's Total U.S. Market Fund (VTSMX) which returned 9.9 percent by 7.6 percent per year. Other BRIC ETFs also underperformed. The Guggenheim BRIC (EEB) returned just 2.2 percent for the period, and the SPDR S&P BRIC 40 (BIK) returned 4.6 percent.

The bottom line is that even if you are able to forecast which countries will have faster rates of economic growth, that won't necessarily translate into superior investment returns. In other words, while the ability to grow an economy at a faster rate of economic growth is good information for the individuals living in those countries (as they will likely benefit from rising standards of living), it's not relevant for you as an investor. Information doesn't have any value unless you're either the only one who knows it, or you can somehow interpret it better than your competitors. And since neither of those two criteria is likely to be met, you're best off ignoring the information.