How best to generate lifetime retirement income?

One of the most important retirement planning decisions you'll need to make is how you'll use your 401(k), IRA or other retirement savings to generate a lifetime retirement paycheck. This task is particularly critical if you haven't earned a significant lifetime pension from your employer, a situation many people are in these days.

Here are two different approaches for viable retirement income generators (RIGs):

- Systematic withdrawals: You invest a portion of your savings and use a withdrawal method to generate a paycheck intended to last the rest of your life. But it may not last if you live a long time or suffer poor investment returns.

- Immediate annuities: You give a portion of your savings to an insurance company, and it guarantees to send you a monthly check for the rest of your life, no matter how long you live and no matter what happens in the economy.

You'll find many opinions about these two approaches, some based on facts and some based on misperceptions. You'll also find that the people with the strongest opinions are often the ones who have a financial stake in your decision (meaning they want to invest your money for you or sell you an annuity).

With both approaches, you can find high-cost, poor-performing solutions or low-cost, efficient solutions. Your task is to first decide which approach, or combination of them, best meets your needs, then seek the most efficient version of each type of RIG.

Here's one important difference between systematic withdrawals and annuities that's relevant to this analysis. With most immediate annuities, the income stops at your death, and no further benefits will be paid (unless you elect a joint and survivor benefit -- then the income will stop when both you and your spouse or partner die). With systematic withdrawals, any money left in your account when you die is available as a legacy unless, of course, you exhaust all your savings before you die. In that case, you experience "money death" before physical death.

One way to compare systematic withdrawals with immediate annuities is to consider the circumstances where one approach would beat the other, meaning the circumstances under which you'd receive more retirement income or have money left over for a legacy. With annuities, you "win" if you live a long time or would have experienced poor investment returns if you had invested your money instead. With systematic withdrawals, you "win" if you experience good investment returns or die well before your life expectancy.

Let's look at an analysis that digs deeper into this comparison. First, let's consider a 65-year-old single woman who has $100,000 in retirement savings that she'll use to generate a regular paycheck. (Later we'll look at other situations.)

If our retiree uses an annuity bidding service such as Income Solutions -- one cost-effective way to buy an immediate annuity -- she could have bought a monthly annuity that would generate about $562 per month for the rest of her life.

But what are the circumstances where she could have realized a higher retirement income with systematic withdrawals? One way to answer this question is to determine the rate of return she'd need to earn so she could withdraw $562 per month over various lengths of time she might live.

For example, if she lives 10 years then passes away, she could have withdrawn $562 per month, earned no interest at all and money would still be left when she dies. This means she could have withdrawn more than $562 per month, or she could have withdrawn that amount and leave a legacy upon her death. If she lives only 10 years, clearly she'd be better off using systematic withdrawals than purchasing an annuity to generate a retirement paycheck.

But what if she lives longer than 10 years?

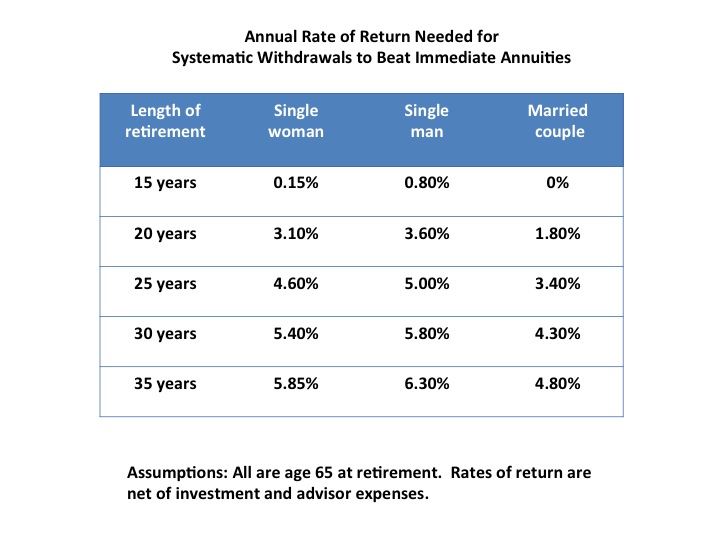

- If she lives 15 years, then passes away, she would need to earn at least 0.15 percent per year for 15 years to have any money left over when she passes away. Certainly, that's possible even at today's low interest rates. So, if she lives for only 15 years, she'll most likely still be better off using systematic withdrawals to generate a retirement paycheck.

- If she lives 20 years, then passes away, she'll need to earn at least 3.1 percent per year for 20 years to have any money left over when she passes away. There's a good chance she could invest in bonds and earn that rate, although she'd need to be a knowledgeable investor to do so. If she invests in the stock market, she could earn 3.1 percent per year or more, but she would need to accept the risk that she could lose money. Even still, if she lives for only 20 years, she'll also most likely be better off using systematic withdrawals to generate a retirement paycheck.

- Using this same logic, if our retiree lives 25 years, then passes away, she'll need to earn 4.6 percent per year for 25 years for systematic withdrawals to beat the income of an annuity. While that's possible if she invests in stocks, there's no guarantee she could do that, and she could lose money if the stock market tanks. Now, the comparative advantage of systematic withdrawals over annuities isn't as clear.

- If she lives 30 years, then passes away, the break-even rate of return is 5.4 percent per year. Again, it's possible to achieve this return, but our retiree would need to assume significant stock market risk to have a chance to earn that rate of return consistently for 30 years.

We can also apply this logic to a single man age 65 and to a married couple both age 65 who are considering buying a 100 percent joint and survivor annuity. In this last case, the retirement income continues as long as one person is alive. The following table summarizes the results of this analysis for the single woman, single man and married couple.

This table shows that if the single man lived for 25 years, he'd need to earn at least 5 percent per year for 25 years for systematic withdrawals to beat an immediate annuity. The married couple electing the 100 percent joint and survivor annuity would need to earn 3.4 percent per year for 25 years for systematic withdrawals to beat the annuity.

Note that these returns are net of investment expenses and fees paid to financial advisors. If your advisor charges 1 percent of assets, you'll need to add those charges to the target rates of return as well. In this case, the single man who lives 25 years would need to earn 6 percent per year because he's paying 1 percent per year to his advisor. And if he's investing in mutual funds, the 6 percent return target is net of mutual fund investment expenses.

This analysis offers one way to compare systematic withdrawals with an annuity and helps you focus on the key differences between these two methods of generating retirement income. The annuity protects you if you live a long time or if you're worried about poor investment results. Systematic withdrawals provide access to your savings and the ability to use untapped funds to leave a legacy, and you "win" if you experience favorable investment returns.

The advantages and disadvantages of each approach tend to complement each other, which is one argument for diversifying your sources of retirement income and dividing your savings between both approaches. You'll be best served if you learn about the pros and cons of each approach and consider which approach, or combination of approaches, best suits your goals and circumstances.