Why investors are complacent as market catalysts loom

You've probably noticed that you haven't noticed the stock market lately.

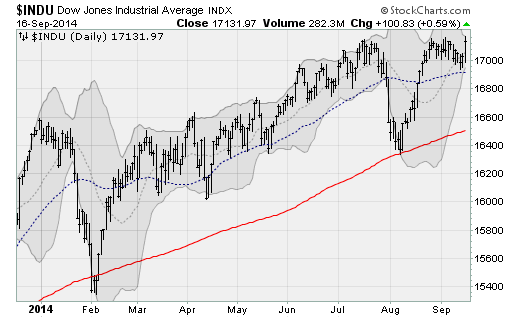

Over the past month, the S&P 500 has traded near the 2,000 level. The Dow Jones Industrial Average has remained near 17,000. And volatility, the day-to-day oscillations of active trading, has diminished to very low levels. In fact, according to one study, current market jumpiness not just in stocks but in other assets like currencies and bonds has fallen near historic lows.

But that's set to change as a number of major catalysts threaten to rattle an overly quiet market. While this doesn't mean stocks are going to go down, it means that investors are going to have to start paying attention again at a time when confidence in the market, according to the AAII survey of investors, is at levels not seen since 2004.

On Wednesday, things start off with the Federal Reserve.

Markets had been drifting lower over the last few days in anticipation of a more hawkish outcome from the Federal Reserve's latest two-day policy meeting, due to wrap up today.

Given the robust performance of the economy over the summer, investors are preparing for the Fed to confirm this by ending the QE3 bond buying program in October and moving forward the timing of its first short-term interest rates hike since 2006 into the middle of 2015. So the dialogue was all about the end of the steady flow of cheap money stimulus.

That changed on Tuesday, sending the Dow Jones Industrial Average to record intra-day highs (although the S&P 500 couldn't close above the 2,000 level once again).

It started when the Wall Street Journal's Jon Hilsenrath -- the Fed's preferred media leak outlet -- said the removal of the "considerable time" language from the Fed's statement wasn't a sure thing. These two words concern the timing of the first short-term rate hike after QE3 ends in October. It's seen as representing about 6-9 months.

The end result was a near vertical ramp in stocks and risk assets in general, including commodities, currency carry trades, bonds and precious metals.

As a result, expectations are high that the Fed will deliver on what Hilsenrath teased. That'll be tough given the plethora of Fed datapoints that are about to be released including the post-meeting statement, the summary of economic projections (known as the "dot plot"), and Fed chair Janet Yellen's press conference.

So it's not surprising that some apprehension crept back into the market heading into the closing bell. Stocks finished off their best levels. Treasury bonds finished deep in the red after flirting with gains mid-day. Junk bonds pulled back for a small 0.1 percent gain on the day. Precious metals gave back the majority of their gains. And the U.S. dollar, which dipped on the Fed news, rebounded.

Clearly, tensions are high and the stakes are even higher as the market, after skidding sideways over the last few weeks, looks ready for a decisive break up or down out of its recent trading range. Look for more fireworks on Wednesday.

After the Fed, other catalysts include the upcoming Scottish independence vote (which could rattle Eurozone debt market), the ongoing battle against ISIS (threatening crude oil supplies), the unresolved situation in Ukraine (which has rattled stocks before), and the upcoming mid-term elections in November (which if the Republicans capture the Senate could usher in more fiscal fights, government shutdowns, and possible debt defaults as the GOP locks horns with the White House).

Investors have a lot to watch out for as the peaceful market conditions they've gotten used to look set to end.