Here's the problem with the historic post-Brexit rebound

Wall Street's bulls are foaming at the mouth right now. After apocalyptic warnings about the Brexit vote a few weeks ago, U.S. large-cap stocks surged to new record closing highs on Tuesday -- capping one of the most powerful dump-and-pump rebounds in market history and potentially marking the end of a three-year funk.

Why? Well, that's complicated. But at the core, it's same theme that has lifted stocks more than 220 percent from the March 2009 low: the hope and promise of cheap-money stimulus. This time, it's out of Japan.

First, however, the story has a big, fat wrinkle that could either be an opportunity for investors who are late to arrive at the rally or confirmation to the skeptical that all is not well. Just 16 percent of the stocks in the S&P 500 are hitting new 52-week highs right now while more than 22 percent are trading in outright bear markets (down 20 percent or more from their highs).

There's more.

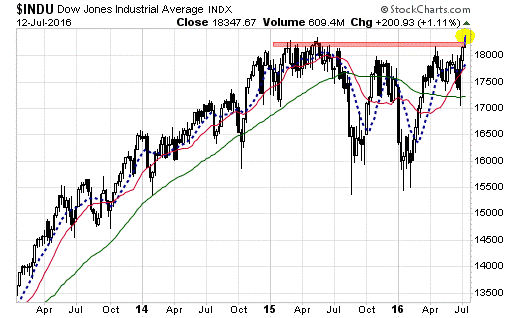

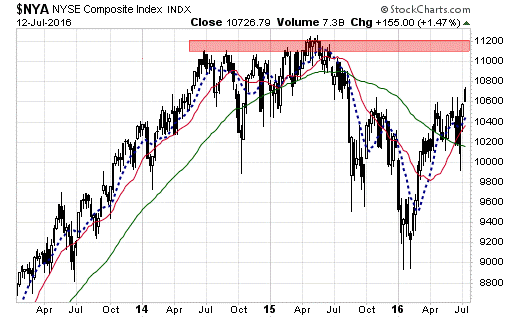

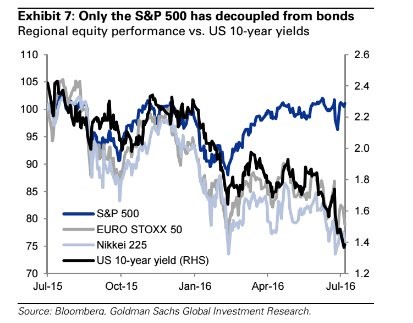

Even as the Dow Jones industrials finally cracked over the 18,000 level again, the majority of stocks, as measured by the NYSE Composite, remain well below their 2015 highs (charts above). The "fear trade" continues to outperform for the year-to-date, with gold, Treasury bonds and utility stocks leading the way. Earnings still look terrible: Second-quarter 2016 is expected to be the fifth consecutive period of declining profits. And consider that the U.S. stock market is the last man standing, so to speak, as other developed economy stock markets have already rolled over (chart below).

U.S. blue chips are in a bubble of their own, both in terms of risk-vs.-reward and a lack of fundamental support and in terms of acting insulated from problems bothering overseas bourses. And, to mix metaphors, the support for U.S. equities uptrend is dangerously narrow.

That gets us back to the catalyst: reports that Japan is preparing an even more aggressive round of monetary policy stimulus -- spurred on by no less than Ben Bernanke himself, as the former Federal Reserve chairis in Tokyo consulting with government and Bank of Japan officials.

The long and short of it is Japanese Prime Minister Shinzo Abe -- encouraged by an electoral victory and disappointed by an ongoing debt-deflation malaise amid eye-watering public debt-to-GDP levels -- is likely to unleash a version of Bernanke's "helicopter money." That would be a $100 billion fiscal stimulus funded not by debt but by the BoJ printing fresh money.

For the monetary junkies on Wall Street, excitement over this trumps everything else. The ongoing U.S. corporate earnings recession doesn't matter. Expensive stock valuations don't matter. Uneven economic data should be ignored. Look away from fresh weakness in crude oil.

The stock market is confounding just about everyone. According to Bank of America Merrill Lynch, just 18 percent of active investment managers are outperforming their benchmark, marking the worst year on record.

Just look at the bond market, which the pros know eclipses the stock market in size, level-headedness and importance.

About a quarter of global government bonds are trading with negative interest rates. A German railroad just sold the first-ever nongovernment, nonfinancial corporate bond with a negative yield. Bond-market derived inflation expectations have been collapsing. This is a big vote of no confidence in the virility of the central bank cabal. And it's exactly the opposite message stocks are sending.

A clue that Wall Street pros are eyeing the exit -- likely as soon as Brexit risks reappear in the headlines as a new British prime minister comes to power -- is the way the CBOE Volatility Index (VIX) or "fear gauge" diverged from the rally and rose on Wednesday. The Bank of England is due for a monetary policy decision on Thursday as well. Theresa May, the new U.K. prime minister, said earlier this week "Brexit means Brexit" and that she'll "make sure we leave the European Union."

Finally, for those who still care about fundamentals, big bank earnings are coming later in the week, with JPMorgan (JPM) reporting on Thursday and Citigroup (C) and Wells Fargo (WFC) on Friday. Overall, according to FactSet data, second-quarter S&P 500 earnings are expected to decline 5.6 percent from last year's period.

While the chances that the "meltup" continues can't be dismissed, investors should consider all these risks if they're allocating fresh capital to stocks at these levels. Buyer, beware.