Troubled First Republic Bank seized and sold to JPMorgan Chase

Regulators seized control of First Republic Bank on Monday and accepted a bid from JPMorgan Chase for virtually all of the lender's assets. It is the third financial institution taken under government control in the last two months following a series of lightning-fast bank runs that has shaken the confidence of financial industry customers and investors.

California's Department of Financial Protection and Innovation (DFPI) said it had taken over San Francisco-based First Republic and appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. FDIC officials then accepted a bid from JPMorgan "to assume all deposits, including all uninsured deposits, and substantially all assets of First Republic Bank," the DFPI said.

"First Republic customers can bank as usual and feel confident that their deposits are backed by the strength and security of JPMorgan Chase," Jeremy Barnum, JPMorgan's chief financial officer, said during a news conference Monday.

First Republic has 84 branches across eight states: California, Connecticut, Florida, Massachusetts, New York, Oregon, Washington and Wyoming.

JPMorgan CEO Jamie Dimon said the locations will be converted into JPMorgan wealth management centers over the next 18 months. JPMorgan will make a "modest" one-time $2.6 billion gain by acquiring First Republic but will also spend another $2 billion restructuring the regional bank, he added.

"This acquisition modestly benefits our company overall, it is accretive to shareholders, it helps further advance our wealth strategy and it is complementary to our existing franchise," he said, noting that 800 JPMorgan employees worked around the clock to complete the transaction.

Dimon also said buying First Republic's assets will help stabilize the U.S. banking system, which has been rocked in recent weeks by the sudden collapse in March of Silicon Valley Bank (SVB) and Signature Bank.

JPMorgan will gain $92 billion more in customer deposits and also absorb $173 billion in outstanding First Republic loans. Without the deal, the FDIC would have needed to assume all of First Republic's debt.

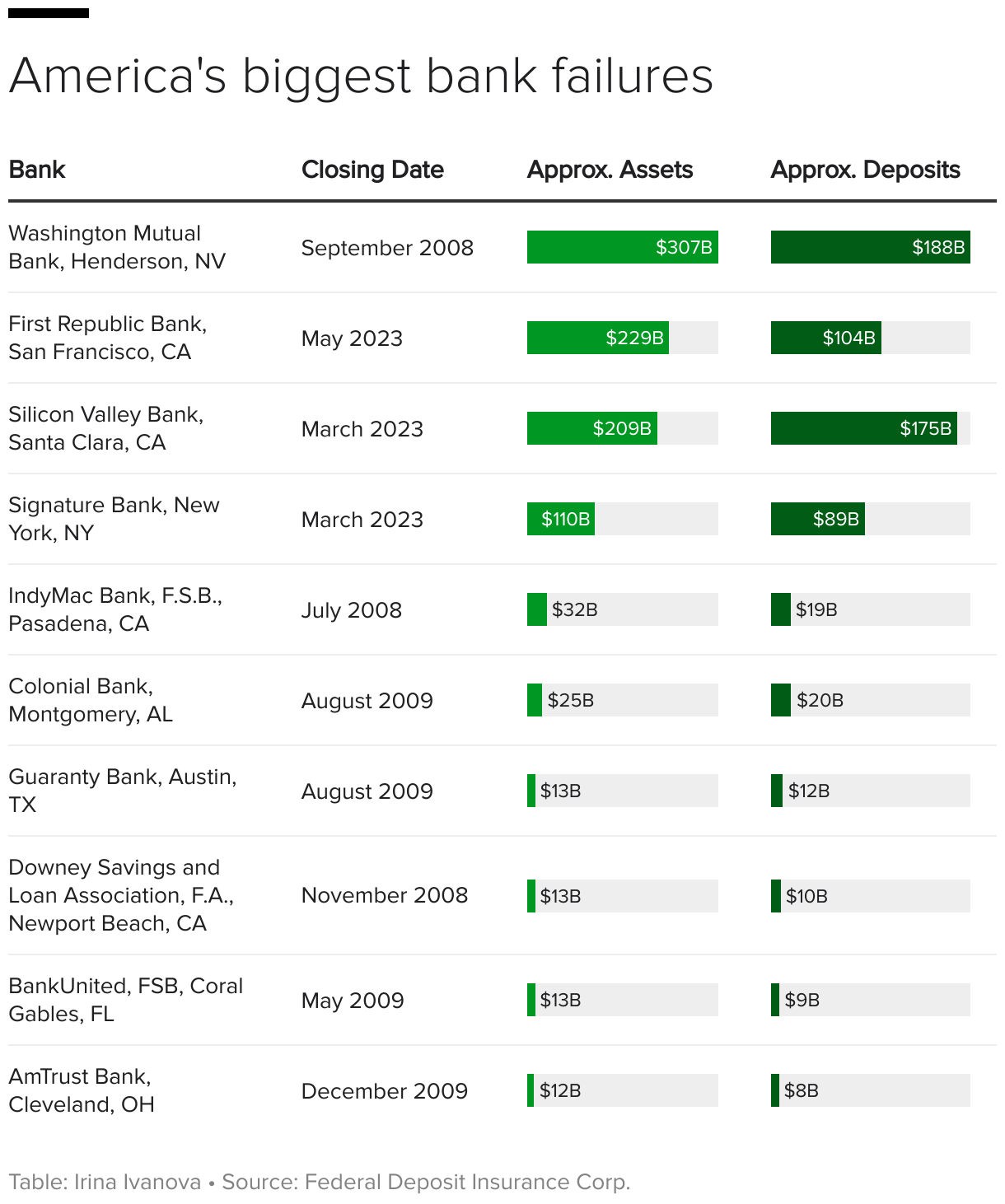

Second-biggest bank failure in U.S. history

First Republic has $229 billion in assets, making it the second-biggest bank to collapse in U.S. history after the 2008 failure of Washington Mutual, which at the time had roughly $307 billion and also was sold to JPMorgan. Silicon Valley Bank had roughly $209 billion when it was seized by California regulators.

The government's move to assume control of First Republic came one week after it disclosed that customers had withdrawn more than $100 billion following SVB's collapse. As with its San Francisco neighbor Silicon Valley Bank, First Republic had many affluent account holders with deposits exceeding the $250,000 limit guaranteed by the FDIC. That made it more vulnerable to a bank run as customers rushed to transfer their money elsewhere.

Hoping to stem the panic, 11 of the nation's largest financial institutions in mid-March gave First Republic $30 billion in deposits, but the effort failed to assuage concerns about the bank's viability. Under Monday's deal with JPMorgan, the funds will be returned to the firms, TD Cowen analyst Jaret Seiberg said.

Another hit to the FDIC's Deposit Insurance Fund

U.S. Treasury officials said Monday they're encouraged that the First Republic seizure happened "with the least cost to the Deposit Insurance Fund."

The FDIC estimated the cost to the Deposit Insurance Fund at about $13 billion; by comparison, SVB's failure resulted in a $20 billion hit. Before that collapse, the largest loss for the DIF was $10.7 billion in 2008 to resolve the loss for subprime lender IndyMac.

At the end of the fourth quarter of 2022, the DIF had $128 billion in reserve. The fund is mostly financed through fees paid by the nation's banks.

Federal officials from the FDIC, Treasury Department and Federal Reserve held private talks with other banks on Friday hoping to find a bailout plan for First Republic, Reuters reported, but no private rescue materialized. Takeover talks continued all weekend in the hope a deal could be struck before U.S. stock markets opened Monday.

Washington's reaction

Although the acquisition of First Republic's assets by another lender may shore up confidence in the banking system, analysts noted that JPMorgan is growing even larger as a result of the deal and is likely to attract the scrutiny of lawmakers.

"The failure of First Republic Bank shows how deregulation has made the too big to fail problem even worse," Senator Elizabeth Warren tweeted on Monday. "A poorly supervised bank was snapped up by an even bigger bank — ultimately taxpayers will be on the hook. Congress needs to make major reforms to fix a broken banking system."

Regulators wanted a private company to take over First Republic to avoid the FDIC taking on too much debt, and that requirement "may have precluded other regional bank bidders from making the math work as well as it does for JPM," Ken Usdin, equity analyst for Jeffries, said in a note Monday.

Dimon dismissed concerns about JPMorgan's size, saying the U.S. needs big financial institutions as much as it needs small and regional lenders.

"We need large, successful banks in the largest and most prosperous economy in the world," he said. "You need large, successful banks. And anyone who thinks that it would be good for the United States of America not to have that, should call me directly."