Don't be shocked if stocks rebound, for a bit

U.S. equities alternated between gains and losses on Tuesday as traders returned after the long holiday weekend to celebrate the life of Martin Luther King. The modicum of enthusiasm -- despite crude oil closing below the $29-a-barrel level for the first time since 2003 -- was driven by China's weakest GDP growth in 25 years, which fueled hopes of fresh monetary and fiscal policy stimulus.

No doubt, many concerns remain: Among them are the ongoing OPEC-U.S. shale-oil price war, declining corporate profitability, soft U.S. economic data, and currency, credit and equity market volatility in China. Still, stocks here at home look set for at least a temporary relief rally.

Here's why.

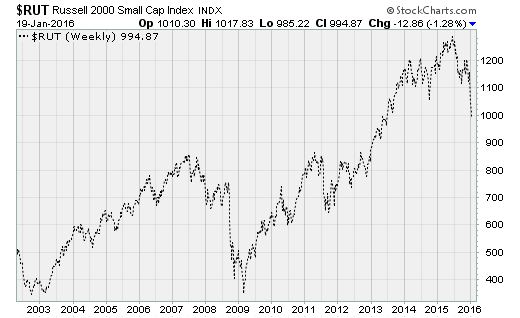

By multiple technical measures, stocks have become extremely oversold. The Russell 2000 Small Cap Index closed below the 1,000 level for the first time since 2013 (chart below). The percentage of S&P 500 stocks in uptrends has returned to its August low. The ratio of activity in equity puts vs. calls (that is, options traders betting stocks will decline vs. those betting they'll rise) has surged to heights not seen since the 2008 financial crisis. And the selling pressure has grown less intense as fewer and fewer stocks participate to the downside when looking at metrics such as the number of net advancing issues on the NYSE.

Jason Goepfert at SentimenTrader wrote in a note to clients this weekend that the gap between rising "Smart Money" confidence vs. falling "Dumb Money" confidence had hit levels not seen since the August low.

Smart money is based on sentiment measures such as commercial hedge positions in the equity index futures market and the relationship between stocks and bonds, among others, that tend to correctly foresee market turning points. Dumb money confidence is based on the opposite sentiment measures, such as the equity-only put vs. call ratio, that tend to be poor predictors of market turning points.

Since 1999, according to Goepfert, there have been 135 other days when the gap between smart and dumb money confidence has been as high as it is now. Over the 30 days that followed, the S&P 500 was positive 113 times (an 83 percent win rate) with a median gain of 4.4 percent.

The maximum decline over the next 30 days was 1.9 percent vs. a maximum gain of 6.9 percent.

Once we're past a short-term reprieve, however, the selling pressure is likely to return.

The latest Bank of America Merrill Lynch Global Fund Manager Survey shows that while pessimism is rising, it's not yet at full-on panic levels. Allocation to cash has risen to 38 percent overweight, the highest level in 43 months and third-highest since 2009. Fewer investors are looking for the dollar's rise to continue. And more are looking for earnings per share growth to drop than at any time since October 2012.

But just 12 percent of respondents believe a recession will occur in the next 12 months, and the vast majority remain overweight stocks. This suggests a deep-seated optimism that could very well set up most market participants for disappointment as 2016 rolls on -- especially if the Federal Reserve sticks to its guns on its December forecast of four additional 0.25 percent rate hikes this year.