Banks boost earnings as refinancings surge

(MoneyWatch) JPMorgan Chase's (JPM) earnings are surging, while Wells Fargo (WFC) investors seem underwhelmed by the bank's latest quarterly results.

JPMorgan reported net income of $5.71 billion, up from $4.62 billion for the same period a year ago. There was scant mention of the now infamous "London Whale" trade, which will generate an additional $300 million in losses, on top of the $5.8 billion notched through June. Earlier this week, the New York Times reported that federal authorities, including the FBI, are using taped phone calls as they attempt to build a criminal cases related to the London Whale.

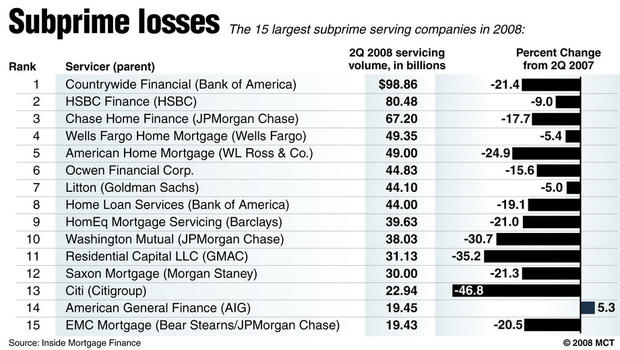

About a third of the increase in earnings was derived from a spike in home loans, prompting CEO Jamie Dimon to state that the housing market "has turned a corner." Dimon added that the bank was still seeing a high level of souring mortgage loans, and said he expects high default-related expenses "for a while longer." And he noted the homeowners still struggling under mortgages they can't afford, saying the bank was working to modify such loans. It's always amusing to hear bankers frame this particular issue in a light that makes it sound like the dirt-bag borrowers are to blame for these losses. In fact, as noted in the chart below, there were also lenders involved in these transactions.

As Barry Ritholtz points out, data from the Federal Reserve Board shows that more than 84 percent of the subprime mortgages in 2006 were issued by private lending institutions and private firms made nearly 83 percent of the subprime loans to low- and moderate-income borrowers that year. In other words, it wasn't Fannie and Freddie that enabled the lion's share of rotten lending, rather private institutions like JPMorgan Chase and Wells Fargo were the big players in the market. Why? Because yields were high, and as long as housing prices kept climbing, it was easy money.

Meanwhile, Wells Fargo said net income was $4.9 billion, up from $4.1 billion for the same period a year earlier, boosted by robust home lending, higher fees and a rise in trading revenue. Revenue was $21.2 billion, up from $19.6 billion a year earlier, but less than analysts had expected. Despite the revenue miss, Wells has delivered 11 straight quarters of net income gains.

The Mortgage Bankers Association expects that mortgage originations probably climbed 33 percent in the third quarter from a year earlier, which helped Wells. The bank accounted for 1 in 3 home loans at midyear, with more than a quarter of all its fees coming from originations and servicing. But for Wells, there is a downside to being the big guy on the block in terms of mortgages. This week, the government filed a civil mortgage fraud lawsuit against Wells Fargo, saying the bank engaged in the "regular practice of reckless origination and underwriting" of government-backed loans.

In sum, the banks have come back from the financial crisis first on the backs of taxpayer support and now, on the backs of homeowners. There is something perverse about this story, especially when we peruse a recent report issued by New York State Comptroller Thomas DiNapoli, which documents the climbing salaries of financial executives.

Sure, the once-bloated financial services industry is shrinking -- the industry has cut 1,200 jobs this year in New York alone. And yes, the cash-bonus pool is shrinking, down 13.5 percent for those securities industry employees who work in New York City. But those left standing in the business are doing pretty well.

The average salary and bonus for a Wall Street professional last year was $362,950, according to Mr. DiNapoli's office, more than five times the average salary in New York of $67,900. (Median U.S. household income is $50,054.) Perhaps even more startling is to consider the past four decades for Wall Street. DiNapoli's office found that in 1982, average pay was about $45,000, about twice the average pay of a private-sector job in New York at the time.

Investors might worry about earnings at the nation's giant financial institutions, but most Americans would love to have such "problems."