America's bull market stands alone

With great fanfare, U.S. equities have climbed out of their Feb. 11 low, reversing what was the worst-ever start to a year and ending a very scary test of last August's market lows. The Dow Jones industrials index climbed back above the 18,000 level for the first time since August and moved within a few hundred points (less than 2 percent) of last May's record high.

With all that, many have started wondering if the long sideways crawl in stocks that started in late 2014 could finally be ending -- despite fundamental headwinds like weak earnings (first-quarter results expected to be the worst since 2009 and the fourth consecutive quarterly decline in profitability) and tepid GDP growth (the Atlanta Fed's GDPNow first-quarter estimate stands at just 0.3 percent).

Whether a breakout is at hand I can't say one way or another. But here's something worth mentioning: America's stock market rally stands alone. Markets around the planet are much less ebullient, with the MSCI World Index (minus the U.S.) down nearly 15 percent from its high last summer. That suggests caution is warranted.

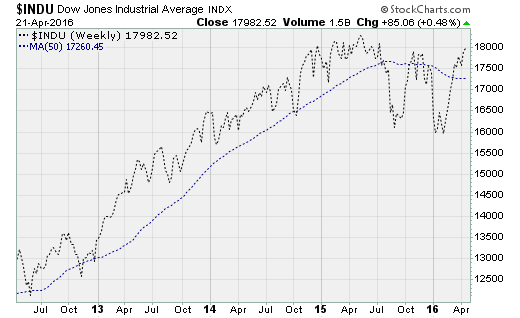

First, the Dow Jones industrials are constrained in a three-year trading range between 16,000 and 18,000 (chart above) as investors struggle to balance catalysts like Federal Reserve policy tightening, the ups-and-downs in crude oil, a stronger dollar, earnings and GDP growth.

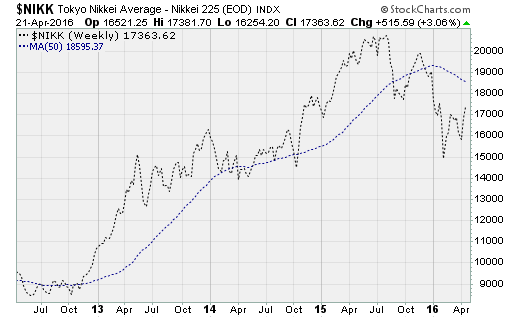

Second, take a look at Japan's Nikkei average, which remains 16.1 percent off of its summertime high and is still well below its 50-week moving average (chart above). GDP growth remains slow, at just a 0.7 percent annual rate. And despite negative interest rates and an aggressive asset-purchase program from the Bank of Japan, inflation is dancing on the edge of negative territory. The specter of deflation is dangerous because of Tokyo's 229 percent government debt-to-GDP ratio.

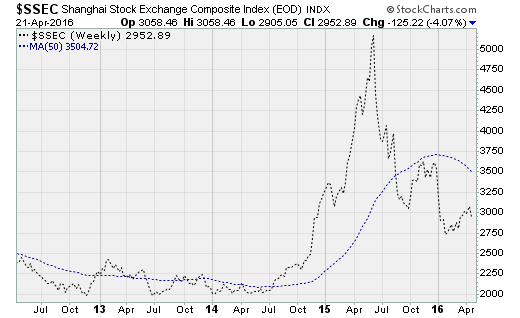

Third, China's Shanghai Composite is still recovering from a dramatic bubble boom-and-bust cycle from 2014 through 2015, which has seen share prices fall nearly 43 percent from their highs (chart above). A two-year-old pattern of lower highs and lower lows remains in play as the Chinese economy grapples with currency volatility, overreliance on credit, capital outflows and a bungled transition away from exports and fixed-asset investment toward services and consumption. And what's happening in China is a big concern for the U.S. Fed, so keep a close eye on that.

Fourth, Germany's DAX is down nearly 16 percent from its high last summer as the eurozone contends with a recent flare up of sovereign debt risk, tepid GDP growth (just 1.6 percent annualized), low inflation and still-high joblessness in peripheral countries, like Spain's 20.9 percent currently.

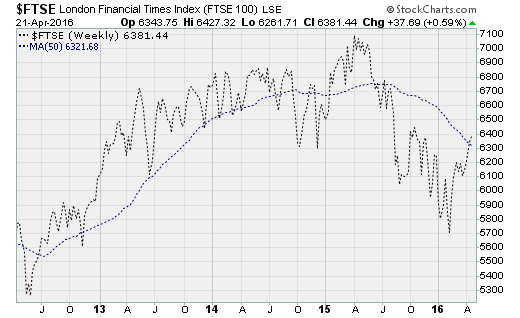

Finally, consider the U.K.'s FTSE index, which is down nearly 10 percent from its high last spring. While GDP growth here is better (at 2.1 percent), recent economic data like retail sales have disappointed (worse performance since January 2014). That suggests headwinds related to Britain's possible exit from the European Union.

Can the U.S. once again be an island unto itself? Investors are about to find out.