10 years seems to be the sweet spot for TIPS

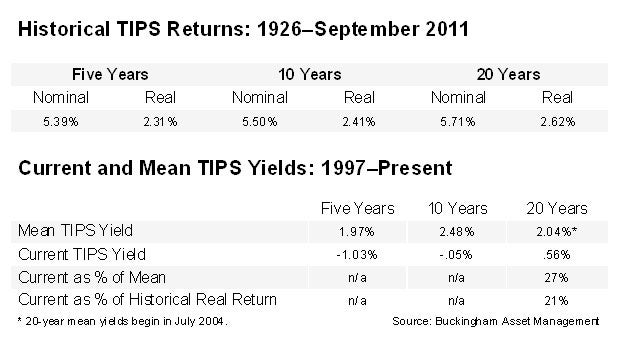

On a monthly basis, I update the tables below to help you make decisions on purchasing Treasury inflation-protected securities. The data is as of November 10. The first table provides the historical data on the real return of nominal bonds from 1926 through September. The second table shows the current and mean TIPS yields.

The 10-year and 20-year nominal Treasuries are currently yielding about 2.0 percent and 2.7 percent, respectively. Last month, they were 2.2 percent and 2.8 percent, respectively. Break-even inflation rates have fallen since last month. The 10-year and 20-year break-even rates are now about 2.1 percent and 2.2 percent, respectively.

The fourth-quarter inflation estimate from the Philadelphia Federal Reserve increased from 2.4 percent to 2.5 percent over the next 10 years. The negative risk premium for unexpected inflation on 10-year nominals decreased from -0.5 percent to -0.4 percent over the last month. With the risk premium for unexpected inflation remaining negative, TIPS are still the clear choice over nominal Treasuries in relative terms.

Now let's review the five-year maturity: The current yield on the five-year nominal Treasury is about 0.9 percent. With the Philadelphia Fed's fourth quarter five-year inflation forecast at 2.4 percent, the expected real return is now -1.5 percent. The market break-even rate between Treasuries and TIPS trades around 190 basis points, which relating to the Philadelphia Fed. Estimate, equates to a -0.5 percent risk premium. This would mean the five-year TIPS have more attractive yields relative to nominal, and makes them still the preferred choice.

In last month's blog post, we mentioned one potential alternative to purchasing a five-year TIPS. TIPS and Treasury yields are now even farther below historical averages. For those investors who have greater capacity to accept the risk of unexpected inflation in the five-year term, one alternative to consider is five-year CDs. Five-year CDs are now yielding 2.2 percent and have a break-even inflation rate of 3.2 percent or roughly 130 basis points over comparable nominal treasuries. The risk premium for unexpected inflation in buying five-year TIPS relative to a similar maturity CD has risen from 0.2 percent last month to 0.8 percent today. Investors who choose five-year CDs need to understand they're not as protected as TIPS buyers for higher unexpected inflation. They're also giving up the term premium of the TIPS curve by electing to stay shorter, as opposed to purchasing TIPS with maturities of greater than five years.

With the flight to quality due in part by the turmoil in the European markets, TIPS yields have continued to fall. Over the last month, TIPS relative to Treasuries were the stronger performers. Five-year TIPS yields fell by 47 basis points, while the five-year Treasury only fell by 25 basis points. Additionally, the Ten year TIPS rallied 24 basis points, while Treasuries only rallied 12 basis points.

On a yield basis, shorter-term TIPS saw the greatest decrease over the last month. This caused the TIPS curve to continue to steepen, which in turn caused a steep price for keeping TIPS with near-term maturities. For example, you pick up an additional 97 basis points in yield (or about 19 basis points a year) by moving from five-year TIPS to 10-year TIPS. Extending another five years to 15 years gives you about another nine basis points per year. Going beyond that earns you about six basis points a year. Given this, some investors could look at the steepness of the current TIPS curve and reason that it offers a decent yield pickup to target maturities in the 10 to 15 year range, if they're willing to accept the term risk. However, with real yields still below their historic averages for TIPS, those investors disinclined to subject their portfolios to additional price risk might find it more prudent to not extend maturities much further than about 10 years or so.

While TIPS yields don't look attractive relative to historical averages, you can't buy yesterday's yields, only today's. And since our crystal balls are always cloudy, we can't know if the current yield on longer-term TIPS will look like good or bad 10 years or more in the future.

As always, one last point to remember is that one of the advantages of TIPS over nominal bonds is that you can take maturity risk with TIPS and earn the term premium without taking inflation risk. Thus, while longer-term TIPS have more interim price risk -- which for some investors could be too much volatility to stomach -- there's no risk of loss if you hold to maturity.

Summarizing, it still seems prudent to limit maturities to about 10 years or so, since absolute yields are well below levels that would make longer-term TIPS a compelling buy regardless of the shape of the yield curve. If real rates rise well above the historical averages, you should consider locking in the higher yields for as long as possible, regardless of the shape of the yield curve. Higher TIPS yields would provide the added benefit of allowing you to lower your equity allocation, thereby reducing the risk of the overall portfolio without lowering expected returns.