10 things you should never buy with a credit card

By Cherise Nelson/GOBankingRates

Credit cards can make your life a lot easier, but they can also create major financial headaches for you when they're used to purchase the wrong things. If you think it's OK to use your credit card for any and all purchases because of the swell perks and rewards you'll get, think again.

Here is a detailed list of things you should never pay for with a credit card, along with why it would be a terrible idea to do so.

Mortgage payments

If you're low on cash one month, it might be tempting to make your mortgage payment with a high-limit credit card, but there are problems with this thinking. For one, many mortgage companies won't let you pay your mortgage with a credit card. Although there are third-party companies that will enable you to use your credit card to pay your mortgage, they often also charge fees for this convenience, which will just add to the amount you're paying in bills each month.

Should you be able to circumvent your mortgage servicer and find a way to pay your mortgage with a credit card, it's still a bad idea if you don't plan on paying off your card balance in full each month: You're already being charged interest on your mortgage, so why add more interest to the amount you're putting on your credit card balance?

Furthermore, charging a large amount like your monthly mortgage payment will lower the amount of credit available to you, which could lower your credit score.

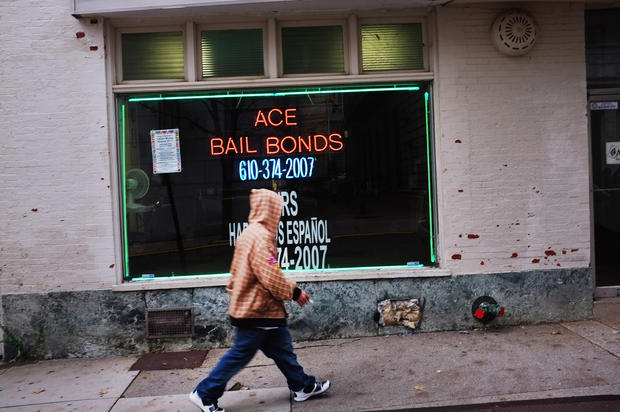

Bail bonds

Although creditors (other than your credit card issuer) will not be able to tell you charged a bail bond, there is still a good reason not to put this transaction on your card. Since a bail bond is regarded as a cash advance by credit card issuers, paying for a bail bond with a card will usually mean you'll incur a fee (generally around 3 percent, but it could be higher) as well as a higher interest rate (like 25 percent).

Alternate payment methods

Alternate payment methods include everything from money orders to person-to-person cash transfers, and are also generally considered a cash advance. While it might be convenient at the time to use your credit card for such purchases, you'll wind up paying a lot more for it than you would expect, including a one-time fee of around 3 percent and a higher interest rate.

Medical bills

When you don't have enough cash on hand to pay for medical bills, one of the worst things that you can do to your current and future finances is put to them on your credit card. Medical care is expensive, and paying for it with a credit card that will charge you high interest on top of this is a bad idea.

If you have large medical bills that you can't pay immediately, don't whip out your credit card -- contact the hospital's financial offices and set up a payment plan. Chances are, you will be paying much less in interest to the hospital than your credit card issuer will charge you.

College tuition

Just like medical expenses, the cost of college tuition has far outstripped the cost of living. If you're a broke college student, it can be very convenient to use your credit card to pay that tuition bill.

The best reason not to do this is that you won't be able to pay off your credit card before you have to start paying interest on it. Plus, many schools will tack on a convenience fee of 2 to 3 percent for the "privilege" of paying your tuition with a credit card. Bottom line: It's not worth it. If you're having trouble making your tuition payments on time, talk to your adviser or the bursar's office at your school; they'll tell you the types of low-interest student loans, grants, scholarships or work-study programs available to you to help defray the costs of your education.

Your taxes

While it's possible (and perfectly legal) to pay your debt to Uncle Sam with a credit card, there is an excellent reason why you shouldn't: Your tax preparer will likely charge you a convenience fee of 2 to 3 percent for using a card. If you're only on the hook for a tax payment of several hundred dollars, that fee won't amount to much. On the other hand, if you owe Uncle Sam thousands of dollars, that 2 to 3 percent fee can really add up. If you think you really can't pay your entire tax debt when it's due, speak with your tax preparer or contact the IRS ahead of time and work out some kind of payment plan. You can find out how to do this by visiting the official IRS website.

Automobiles

Think this is a crazy idea? People have done it. However, many auto dealers will not take credit cards because the fees to process a credit card transaction are so high. However, if you find one willing to take your card, it will likely make you pay transaction fees of 1 to 2 percent. By doing so, you're adding that amount to the price of the car -- and it could cost you hundreds of dollars.

In addition to paying more than you should, with many cars costing far more than $10,000, you are likely going to max out your line of credit, sending your credit score plunging downward. Why not borrow from a bank or credit union if you don't have all the cash you need? You could get rates near 3 or 4 percent, compared to about 15 percent interest on the average credit card. In addition to getting a favorable interest rate, you'll be adding an auto loan to your credit report, which will help your credit score.

Down payments of any kind

If you don't have the money for the down payment on a loan, don't get the loan: You obviously can't afford it. You're adding a large cost to the sales price of your item -- the high interest rates of a credit card. If you must borrow, wait and save up your money for the down payment; when you finally qualify for financing, fill out an application.

Your business startup expenses

A business without a credit rating is going to have a tough time getting a credit card without the personal guarantee of its owner, company officer or board member. Because of this, many people who are starting a new business put expenses on personal credit cards.

This is a terrible idea, as it generally takes at least several years for a business to become profitable. In the meantime, you're paying extraordinarily high interest on debt that you cannot afford to pay back immediately. If your business fails, you are on the hook for all of the charges.

If you do need to borrow money, you're better off with a small business loan, which is typically around 4.5 percent.

Virtual currency

Many people will tell you that buying virtual currency like Bitcoin is risky, no matter how you acquire it, but buying with a credit card adds even more risk. The world of Bitcoin is unregulated and many operators are shady; the reason you should be wary of virtual currency sellers who accept credit cards is that it's very risky for them to do so -- buyers can call the credit card company to revoke the charges while keeping the virtual currency. Be cautious whenever giving your credit card information to a third-party seller.