Why the Fed should allow wages to rise

On Wednesday, the Federal Reserve's Open Market Committee announced its decision to leave its target interest rate unchanged. I believe that was a wise decision. However, it said labor market conditions will be a key part of its decisions about future rate increases:

A range of recent indicators, including strong job gains, points to additional strengthening of the labor market. ...

The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will continue to strengthen. ...

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. ...

In assessing the need for future rate increases, it's important to take a closer look at one component of labor market conditions: how wage increases have been distributed. In 2015, wages increased by 2.2 percent, enough to outpace inflation over that period by a small margin, and wages have continued to rise at close to this rate, but how has that growth been distributed?

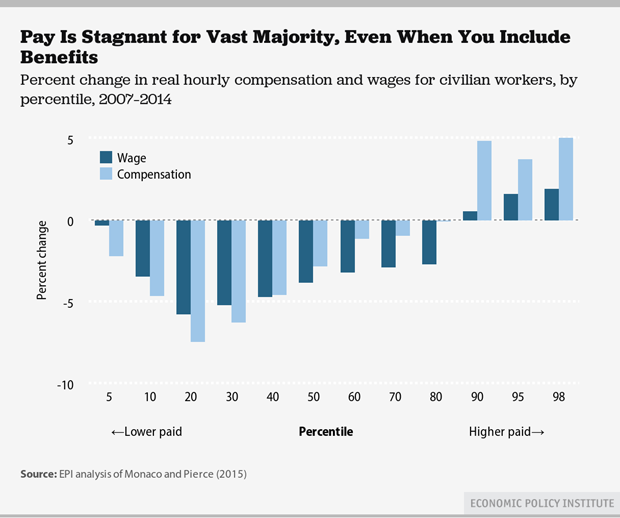

According to a recent analysis by the Economic Policy Institute, the growth in wages adjusted for inflation, or alternatively, wages and benefits adjusted for inflation, has been concentrated among those at the top of the income distribution since the onset of the Great Recession (chart below).

As the report notes, for the median wage-earner, wages and compensation declined by 4 percent and 1.9 percent, respectively. The bottom 40 percent of workers suffered an even greater decline in compensation than in wages, indicating that including benefits as well as pay results in a more adverse trend.

What will it take to get wages growing for those at the lower end of the income distribution? One important change would be to give workers more bargaining power in wage negotiations, something those at the top of the wage distribution are more likely to have.

Another important factor in boosting wages is the state of the labor market. When the economy is near full employment, wages rise much faster.

Achieving full employment -- and despite a jobless rate of 4.9 percent, we aren't there yet because so many workers left the labor force during the recession, and many will return as conditions improve -- depends critically on the conduct of monetary and fiscal policy. Unfortunately, even though aggressive government spending on infrastructure would push employment higher and help the economy reach its full potential, political stalemate makes it very hard to imagine Congress enacting any fiscal policy program of the scale needed. The best we can hope for is that Congress doesn't make things worse by trying to reduce the budget deficit.

That leaves monetary policy as the only policy tool left for promoting and maintaining full employment. While I would have liked the Fed to be much more aggressive to this point (and for it to have left its target interest rate unchanged in December), to date the Fed has done a pretty good job of promoting its employment goals. The real test is ahead.

Monetary policy acts with a lag, so the Fed must forecast where the economy will be months ahead when it sets monetary policy. Presently, it must decide when to continue the increase in interest rates that began at its December meeting. If it acts too soon, it will cause employment to be lower than it could be and stifle wage growth. If it acts too late, the risk is inflation.

Traditionally, the Fed watches growth in wages as an indicator of inflation pressure, and it begins to increase interest rates when it see signs of upward wage pressure. However, it's not necessarily the case that an increase in wages will translate into an increase in prices, particularly at a time when the division of income within firms has favored profits over wages. Prices could go up, but competitive pressures could make it difficult for companies to increase prices and cause the wage increases to come out of profits.

My view is that the cost of inflation is much smaller than the costs associated with flat wages and employment being lower than it could be. For that reason, and because it's far from certain that wage growth will translate into inflation, the Fed should not enact further interest rate increases until it can see clear signs that inflation is a problem.

The working class paid huge costs during the Great Recession in terms of unemployment, home foreclosures and lost savings as people tried to weather the storm. Even before the recession, middle-class incomes were stagnant and inequality was on the rise. Policymakers must do all they can to reverse these trends.

But with elected officials more concerned with political maneuvering than coming to the aid of people in need, the Fed is the only hope left beyond waiting and hoping these problems will somehow fix themselves.

There's widespread belief that the Fed cares more about the interests of the rich and powerful than it does the working class. This presidential election cycle provides ample evidence of this sentiment, and future rate decisions present a golden opportunity for the Fed to show that the vast majority of people, those who toil each day to produce the goods and services we all enjoy, come first.

Yesterday's rate decision was a good start, but the Fed's future decisions will tell the full story.