Why market losses could continue

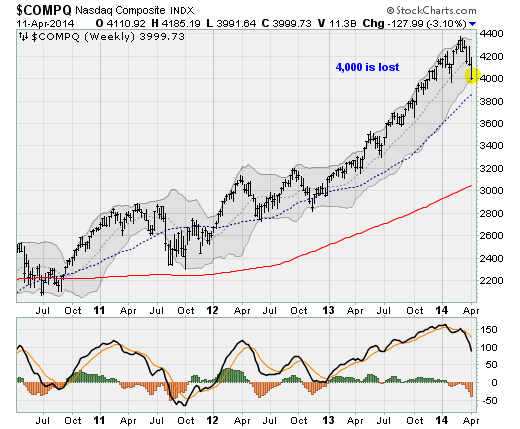

Stocks came under serious pressure again on Friday as the Nasdaq Composite fell to test its early February lows below the 4,000 level. There wasn't a single catalyst for the slide that reversed early-morning gains, although a rare earnings miss by JPMorgan (JPM) sure didn't help.

It was the first disappointing result for the money-center bank in over two years and only the fifth miss in 10 years. First-quarter earnings dropped 28 percent over last year as the release of loan-loss reserves (a favorite big bank earnings trick) couldn't overcome a drop in revenue from bond trading and mortgage originations.

These include the promise of more cheap-money stimulus from the major central banks. Both the Bank of Japan and the European Central Bank have disappointed by withholding new stimulus announcements. And the Federal Reserve, after dragging its feet on the issue throughout 2013, is committed to winding down its "QE3" bond-buying program as the discussion shifts to the timing of when short-term interest rates will rise from the near zero percent level where they've been since 2008.

Stimulus hopes have also been dashed in China as Beijing resists calls for another 2008-style large-scale effort on fears it would only encourage structural problems like overreliance on credit, fixed-asset investment resulting in massive overcapacity in areas like steelmaking, and dependence on exports.

The economic data both at home and overseas have been disappointing, suggesting that winter weather -- the favored excuse in recent months -- cannot fully explain the slowdown in global growth. Here at home, the data are disappointing to an extent not seen since mid-2012. And in China, import and export volumes are dropping off in a way not seen since 2008.

Investor sentiment has been overextended for awhile amid record-low portfolio cash holdings. This has been encouraged by the lack of any significant fear-causing event since the Fed's QE3 program started in late 2012.

Market-top mentality is on display, as clear as day. Just look at the way folks are piling into dubious tech IPO and eurozone sovereign bonds. Greece's issue of a five-year bond was oversubscribed, despite the fact that the structural problems that led the county to renege on its obligations to private creditors and restructure is bond holdings in 2012 remain in place.

Currency trends, which I've written about frequently, have also started to shift as the U.S. dollar threatens to fall out of its four-year-old trading range.

All of this is happening heading into a potentially contentious midterm election season, with the Senate poised to change hands. A Republican takeover of both houses of Congress could open the door to confidence-shaking investigations as well as new confrontations over the budget and the national debt.

And the faith in market fairness has been shaken by the ongoing high-frequency trading scandal.

The selling remains concentrated in infotech and biotech stocks, as the Biotech iShares (IBB) fund dropped below its 200-day moving average for the first time since late 2012. But the selling has also spread to areas that have recently been resisting the downside pressure, including emerging market stocks.

That's a bad sign that folks are selling indiscriminately -- clearing the way for a panic-fueled cathartic wipeout.

Technical indicators are flashing red.

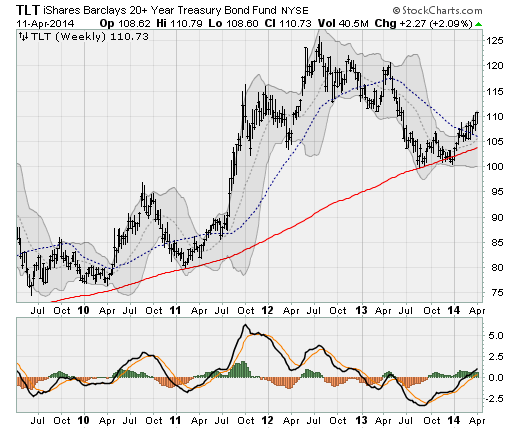

The Nasdaq Composite has fallen further below its 20-week moving average, the support line that held the uptrend since late 2012, as investors pile into safe havens like U.S. Treasury bonds. The iShares 20+ Year Treasury Bond (TLT) looks like it's about to initiate its first medium-term uptrend -- as defined by an upward cross of its 20-week moving average over its 50-week moving average -- since the middle of 2011.

That suggests the volatility and market weakness we've seen so far in 2014 could continue through the end of the year -- if not longer.

The leveraged Direxion 3x Treasury Bond Bull (TMF) fund that I recommended to clients and added to my Edge Letter Sample Portfolio back in February is now up 7.7 percent.

Disclosure: Anthony has recommended TMF to his clients.

Anthony Mirhaydari is founder of the Edge and Edge Pro investment advisory newsletters, as well as Mirhaydari Capital Management, a registered investment advisory firm.